.png)

Although the origins of 420 still remain a mystery, one thing is for sure: it is the unequivocal leader in cannabis shopping days. 420 is akin to black Friday for mainstream retail giants. Every year cannabis retailers see huge spikes in sales, and Headset gets to dig into the data and find interesting patterns. Unlike a regular shopping day this is a day of big discounts, larger baskets (hopefully), and shifting consumer behavior.

Through our retailer partners we have a front-row seat into one of the most exciting markets around. On 4/20/2025 we gathered receipts that accounted for over $50M in sales across the US and Canada, over 3 million units sold. Below we take a dive into markets and categories to give you the highlights (and some lowlights) on every stoner's favorite day.

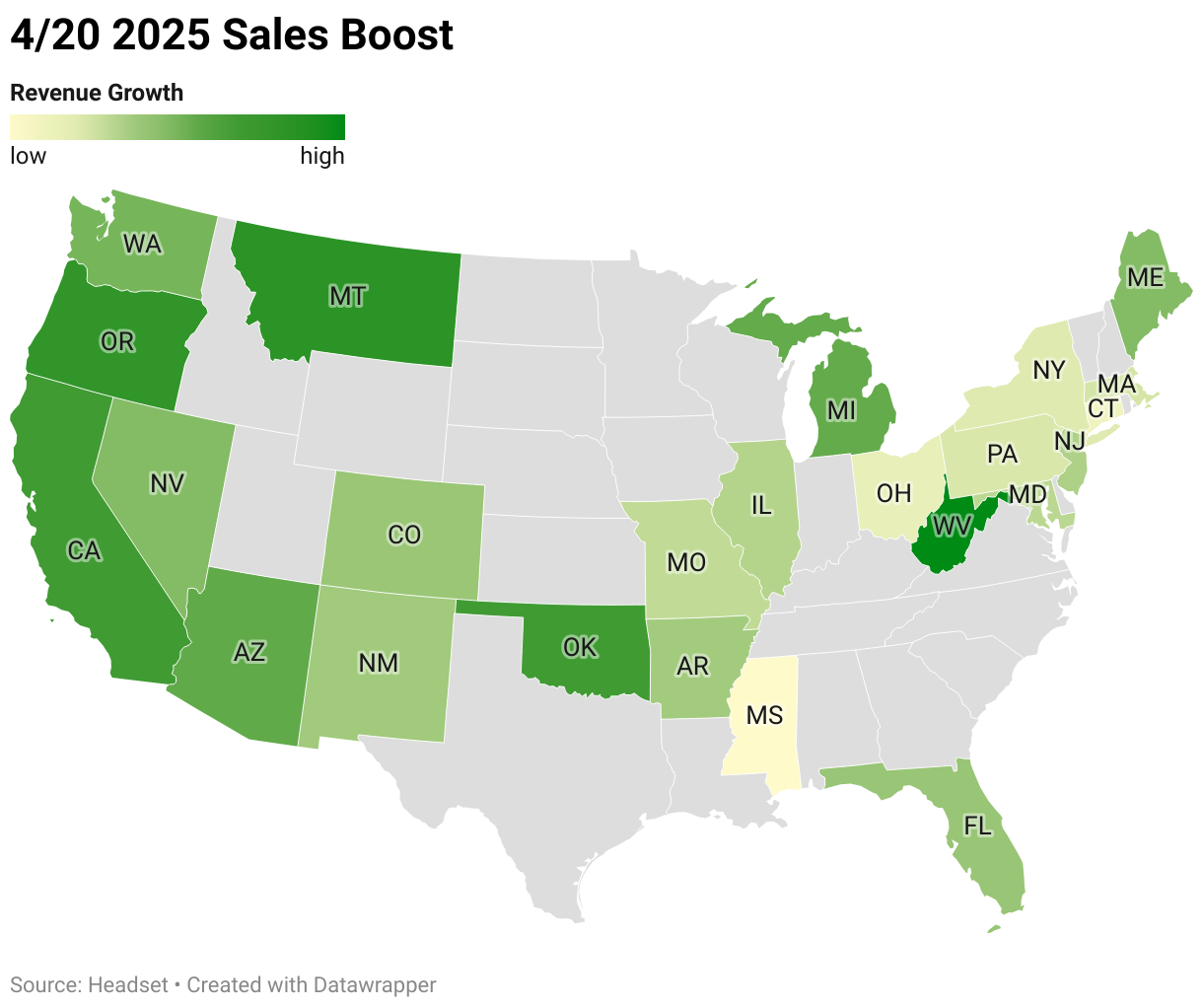

Our data sample from thousands of retailers gives us quick access to see trends and patterns. In the charts below we compare sales at individual retailers with their averages from the prior four weeks. This gives a good picture of the magnitude of the 420 effect in an "average" dispensary.

Oregon saw one of the strongest 4/20 performances nationwide, recording the second-highest increase in total sales. A key driver was a sharp rise in average discounts—jumping from a typical 14% to 34% on 4/20—one of the largest discount increases in the country. With already low baseline prices, these steep promotions resonated with customers, encouraging them to buy more products and drive basket sizes to levels that benefited both consumers and retailers.

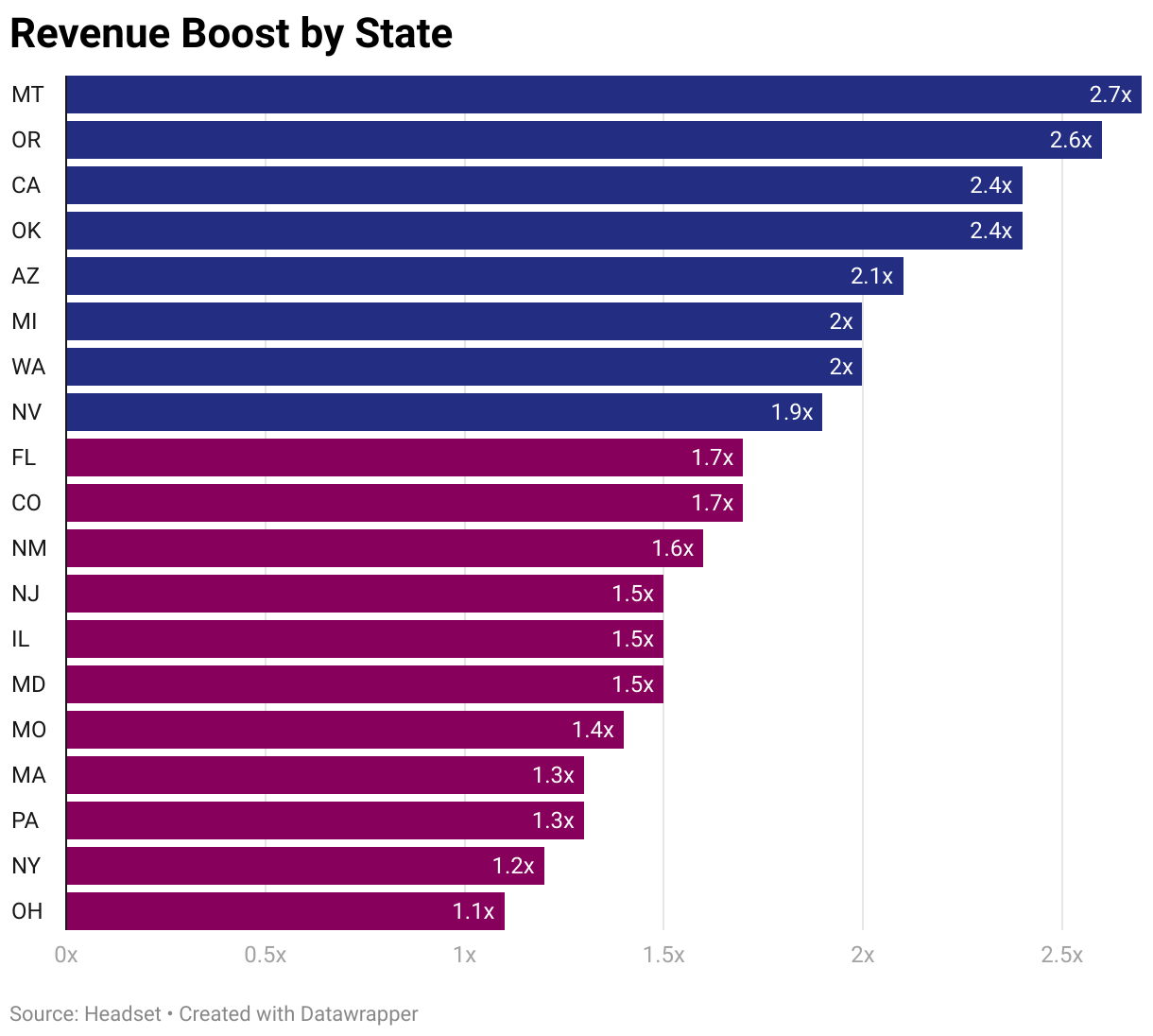

Montana saw the biggest relative 4/20 with 2.7x their typical sales total. Other states like Oregon, California, Oklahoma, and Arizona joined them in the over 2x club this year.

Ohio’s first official 4/20 as a fully recreational market proved somewhat underwhelming. Retailers reported an 8% increase in total sales, a 31% rise in transactions, and an 11% bump in units sold. However, despite offering competitive discounts, these promotions failed to drive significant foot traffic or meaningfully boost basket sizes. High prices in the newly recreational market limited retailers' ability to encourage larger purchases. Notably, many Ohio shoppers chose to stock up in the days leading up to 4/20 rather than on the holiday itself—a trend likely influenced by 4/20 coinciding with Easter Sunday this year.

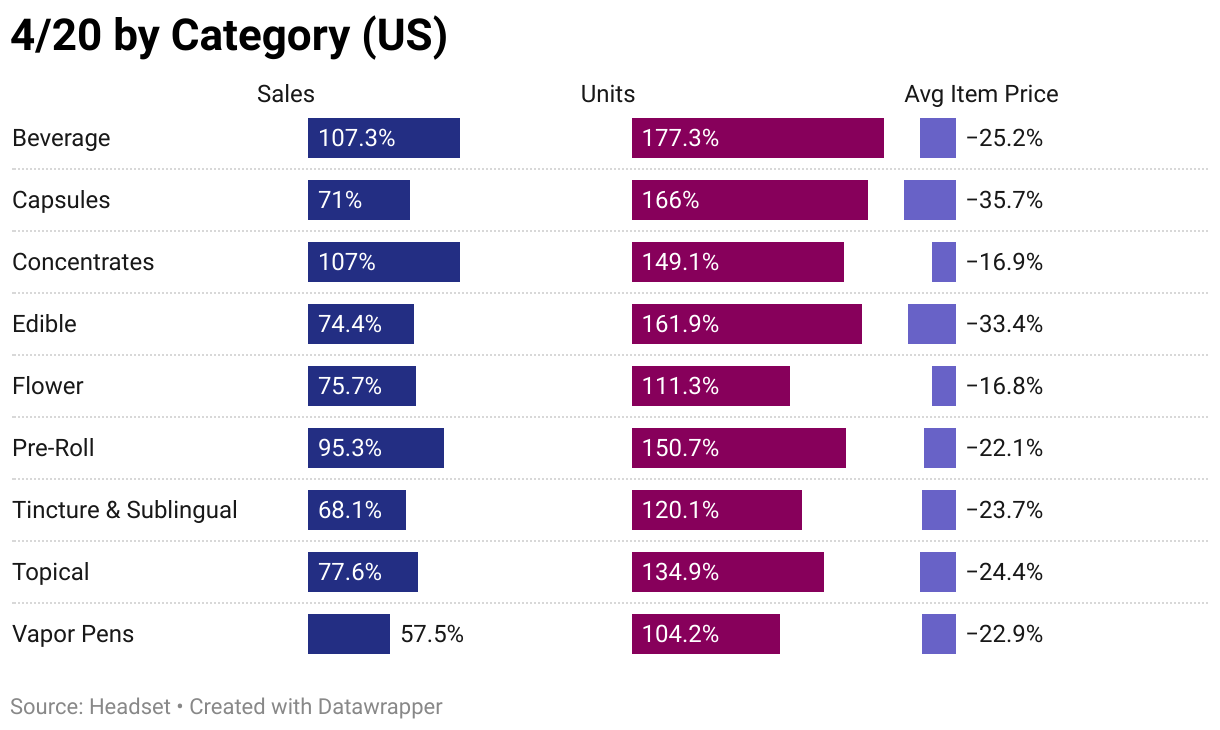

For the second consecutive year, Beverages topped the charts with the largest spike on 4/20 in both total sales and units sold. The category's popularity during social holidays was clearly evident, and 4/20 proved no different.

Concentrates remained a consistently popular category this 4/20, with total sales doubling compared to a typical Sunday. Despite being one of the least discounted categories, consumers still seized the opportunity to purchase this typically high-priced product, making Concentrates one of the top-performing categories of the holiday.

Edibles experienced one of the largest drops in average item price. While unit sales surged by an impressive 162%, the corresponding 74% increase in total sales was modest compared to other categories. This raises the question: was the category over-discounted, or were the elevated discounts applied strategically to drive traffic?

Despite being the second most popular cannabis category overall, Vapor Pens saw the smallest sales lift on 4/20. This may reflect consumer preferences for more social products—such as Beverages and Pre-Rolls—during holiday celebrations, while Vapor Pens are often seen as everyday, convenience-driven purchases.

Still the undisputed king of the dispensary shelf when it comes to total sales. Although its popularity is giving way to more convenient form factors like vapes and pre-rolls (especially among Gen-Z), flower still commands a massive amount of revenue.

New Jersey, one of the most expensive cannabis markets in the country, saw a 30% drop in average item price on 4/20. In contrast, Colorado—home to some of the lowest prices nationwide—experienced a more modest 9% decrease.

The average item price for beverages in New Jersey plunged 62% on 4/20 compared to typical prices—the largest price drop of any category in any state during the holiday. In New Jersey, where prices are already among the highest in the country, beverages stand out as being exceptionally expensive. The holiday provided an opportunity to offer deals on this in-demand product line. To follow trends in New Jersey signup for Headset Insights.

The concentrate category is driven by the most THC-seasoned consumers. These enthusiasts want as little to come between themselves and cannabinoids as is humanly possible. They need no excuse to celebrate the plant, and will still show up for 4/20. Dispensaries appear to be keen on this fact and offered some discounts, but kept it tight. With average item prices only decreasing by 17%, they still managed to drive a 107% increase in revenue. Our Retailer platform assists in monitoring sales and discounting, if you aren't using it you may be missing out.

Topicals in Nevada experienced a dramatic 37% price drop on 4/20. As the highest-priced category in Nevada, this further illustrates how customers leverage the holiday to purchase premium products at a discount.

It’s clear that discounting and promotions are major drivers of traffic on 4/20. Oregon, which posted a 165% increase in sales on the holiday, also recorded one of the largest relative jumps in average discount. This bold departure from typical retailer offerings clearly captured customers’ attention and helped fuel the surge in sales.

Promotions successfully drove traffic into stores on 4/20, but heavy discounting inevitably put pressure on basket sizes. To counteract lower prices, retailers should focus on increasing items per basket to help sustain or grow overall basket value. This year, markets like California executed this strategy effectively—boosting average items per basket by 75%, which in turn led to a 28% increase in average basket size. New Jersey, by contrast, where high prices remain a challenge, did see a modest increase in items per basket; however, it wasn’t enough to lift average basket size above typical levels.

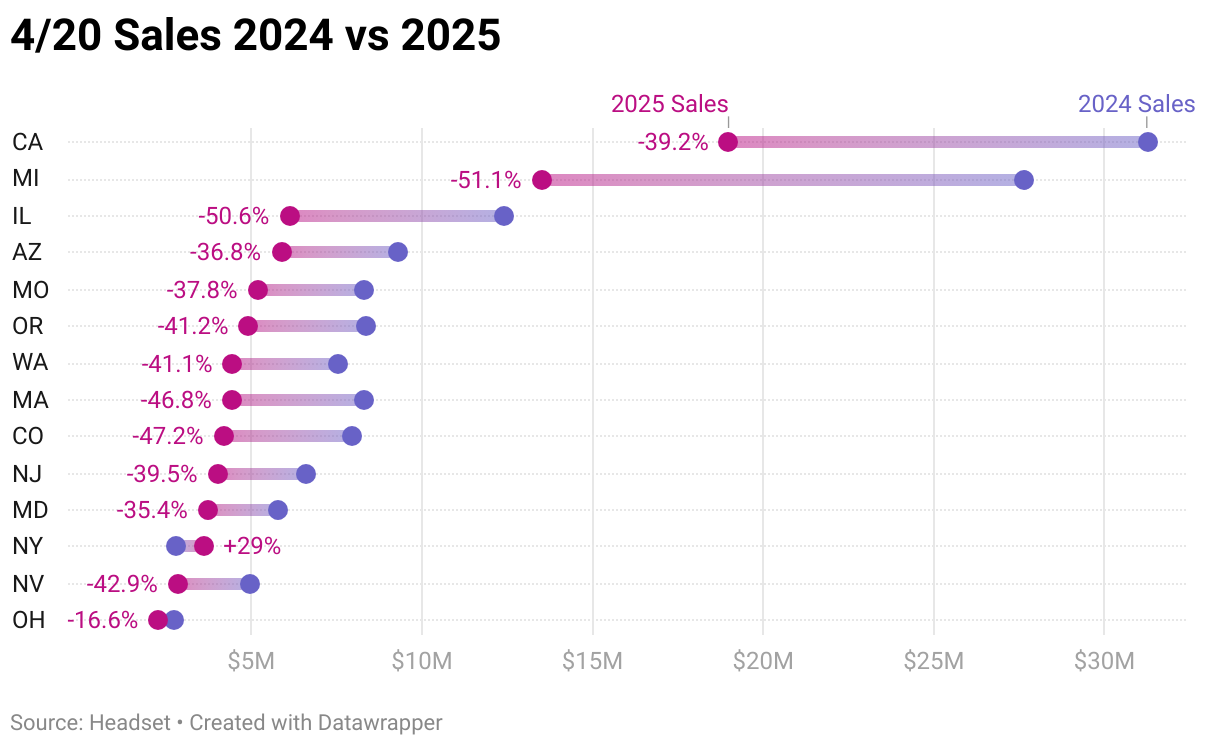

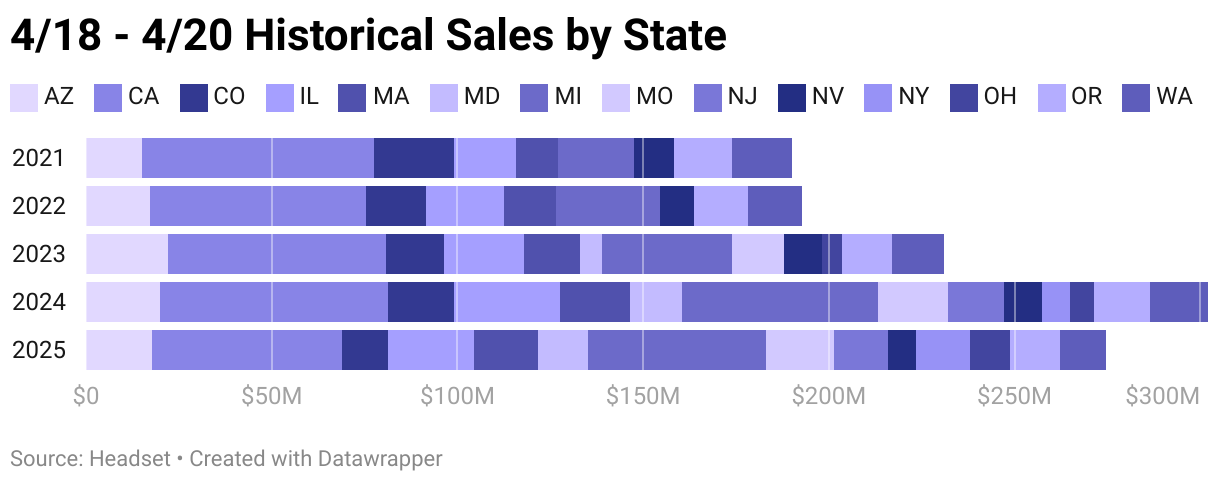

Even with the addition of new recreational markets like Ohio, 4/20 in 2025 saw a significant decline in performance, with total sales down 42% compared to last year’s Saturday holiday. This downturn is certainly - at least in part- related to the holiday falling on Easter Sunday this year.

Nearly every market experienced a decline in total sales compared to last year’s 4/20. The largest reductions were concentrated in mature cannabis markets across the western U.S., where the industry has been contracting over the past year. In contrast, newer markets in the Midwest and Northeast saw smaller declines—and in a unique case, New York posted year-over-year growth.

With 4/20 falling on a Saturday last year, both the holiday and the preceding Friday saw elevated sales, driven by typical weekend shopping patterns. Similarly, this year’s Sunday holiday created a weekend effect, boosting sales across both Saturday and Sunday. Since Friday is typically the strongest sales day of the week, the combination of weekend timing, holiday promotions, and discounts effectively turned 4/20 into a three-day sales event—with Friday ultimately experiencing the highest sales volume of the weekend.

When combining sales totals for April 18th through April 20th, the year-over-year gap narrows to just a 9% decline. In both 2024 and 2025, 4/20 falling on a weekend created a more extended, multi-day shopping experience—unlike previous years when the holiday landed midweek.

A closer look reveals notable regional differences in consumer shopping patterns during the 4/20 weekend. Western states generally saw the largest sales spikes on the 4/20 holiday itself, with a higher proportion of purchases occurring on Sunday. In contrast, consumers in Midwest and Northeastern markets tended to shop more on Friday. In Mississippi—where over 75% of the population identifies as Christian—more than 70% of dispensaries were closed on Easter Sunday, leading most shoppers to make their purchases on Friday and Saturday. Meanwhile, in Montana, where Sunday accounted for the largest share of weekend sales, the market experienced the strongest performance of any state on the actual 4/20 holiday.

4/20 in 2025 was a uniquely nuanced event. Falling on a Sunday—and coinciding with Easter—the holiday evolved into more of a three-day sales opportunity. While 4/20 and Easter Sunday won’t align again until 2088, this year’s event offers valuable lessons for the future. Increasingly, consumers are using the holiday to capitalize on deals, particularly in social categories like Beverages and Pre-Rolls, as well as high-priced items such as Topicals and Concentrates. Notably, Concentrates saw one of the largest sales boosts despite only modest discounting, demonstrating that retailers don’t need to give products away to maximize 4/20’s traffic and sales potential. Looking ahead, it’s critical that retailers and brands are equipped with the right insights and tools to operate efficiently. At Headset, we’re here to help—with a full suite of solutions designed to drive success at every opportunity.

.png)

.png)

.webp)

Tired of waiting 3 months for market data? Experience the real-time difference with Headset.