Estimating Ohio's Cannabis Market Size: Potential for a $2B+ Industry

Introduction

Recreational cannabis is now legal and being sold in the state of Ohio. Through the first month of sales Ohio retailers sold over $50M in cannabis products and everyone wants to know how high this new state is going to climb. The reality is that each state is very much its own market with its own history, regulations, infrastructure, economics and opportunities that all contribute towards shaping the state’s future in the cannabis industry. At Headset we are taking a look a markets across the country and using the data we have to understand where Ohio, potentially one of the nation’s largest markets, and the latest recreational cannabis market could be headed in the upcoming days, months, and years.

Early Sales in Ohio

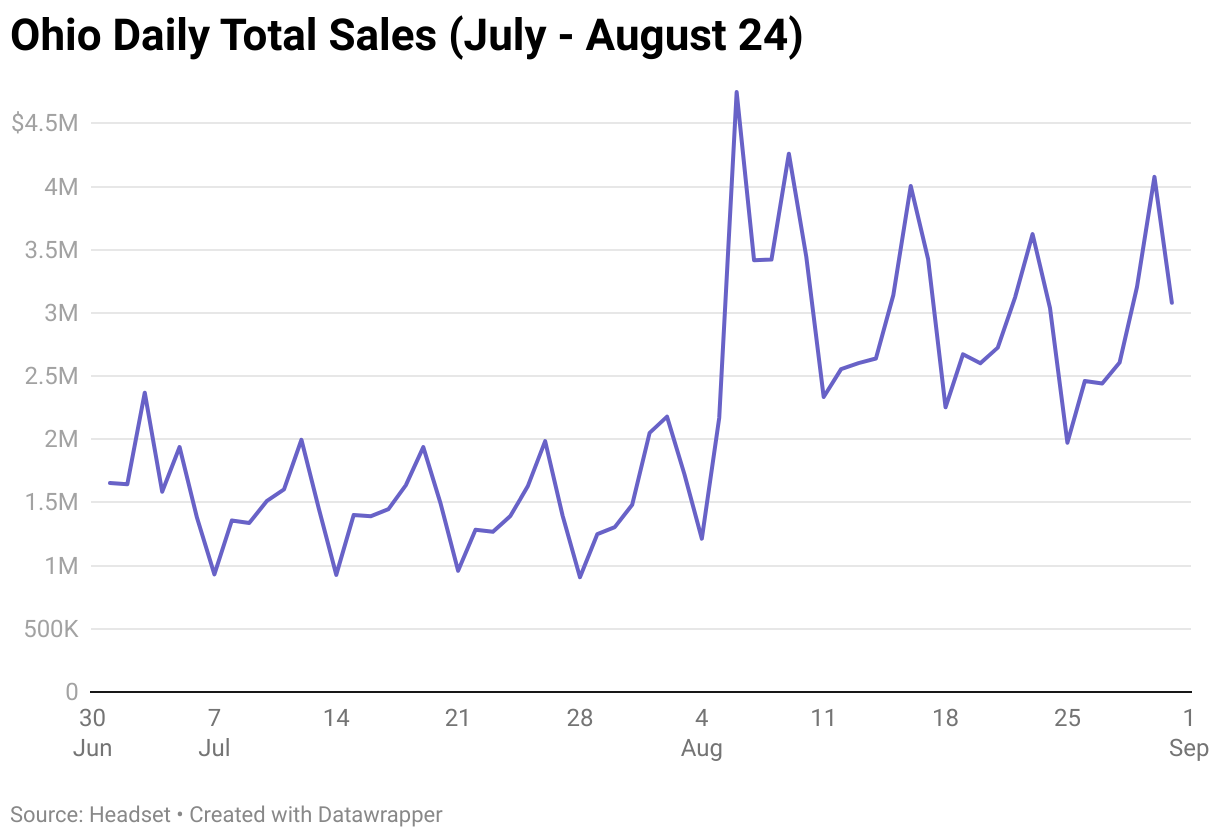

Prior to Ohio’s August launch of their recreational cannabis market the states medical only market had an average daily sales volume of around $1.5M throughout the month of July. However, after the official launch on August 6th the average daily total sales in the Buckeye state nearly doubled to over $3M through the rest of August. Customers, brands, retailers, and regulators love to see the early excitement over this new adult use market, but what can we expect for sales growth in the near future?

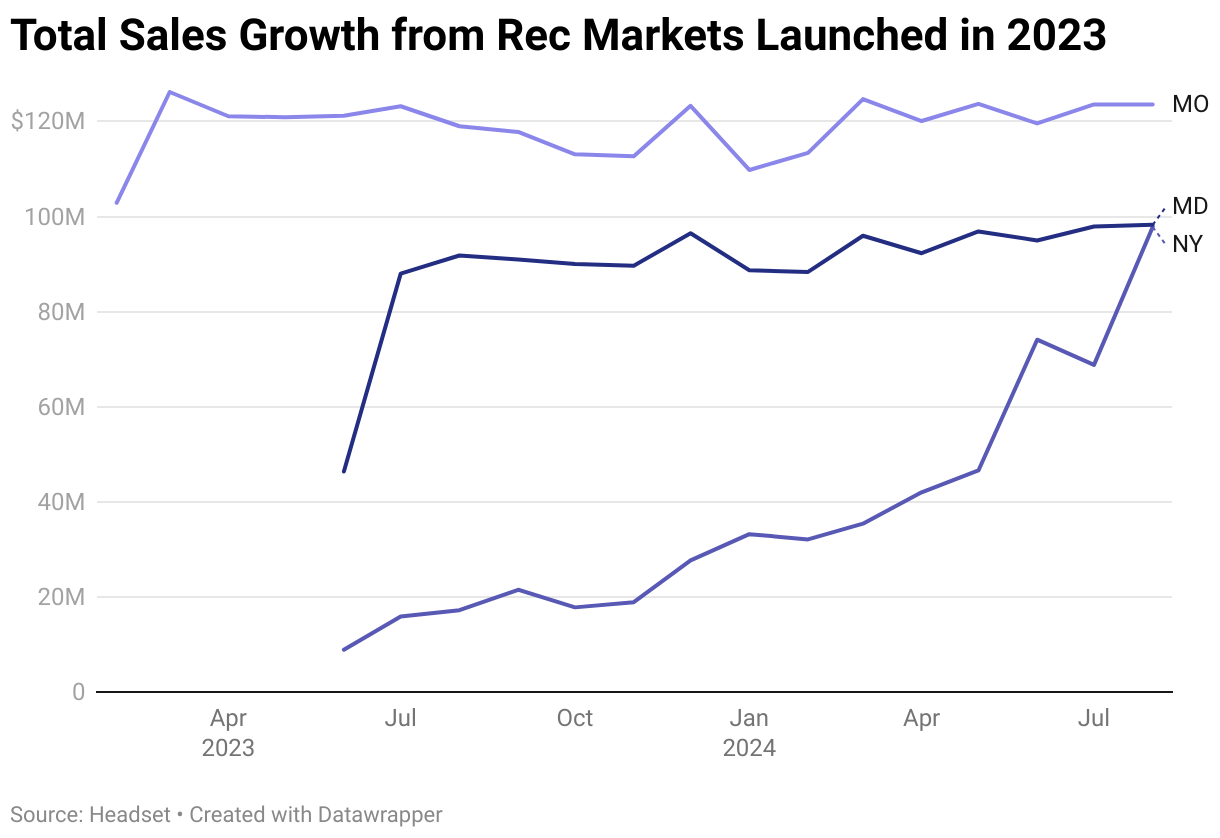

When we take a look at the new market launches over the last year we can see that there are a couple different stories depending on the state. Missouri and Maryland have growth curves that look very similar. Missouri and Maryland had a pre-existing medical market that they were able to transition to a full recreational market almost over night. “Flipping the switch” allowed the market to quickly meet demand before flattening out with some slight sales growth over the months since adult use began. New York on the other hand has seen sales grow over a much longer period of time. This is emblematic of their drawn out process of licensing stores, legal hurdles, and a crack down on illicit sales.

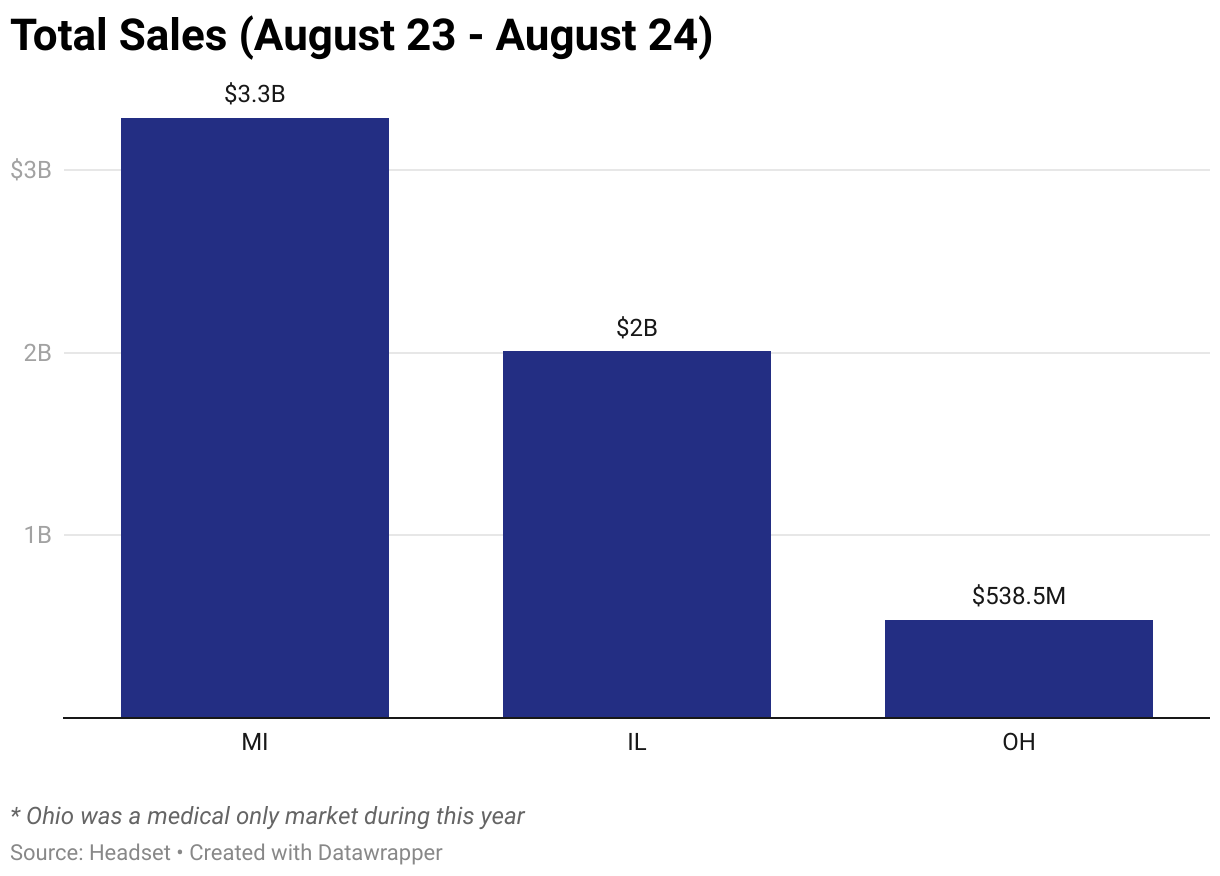

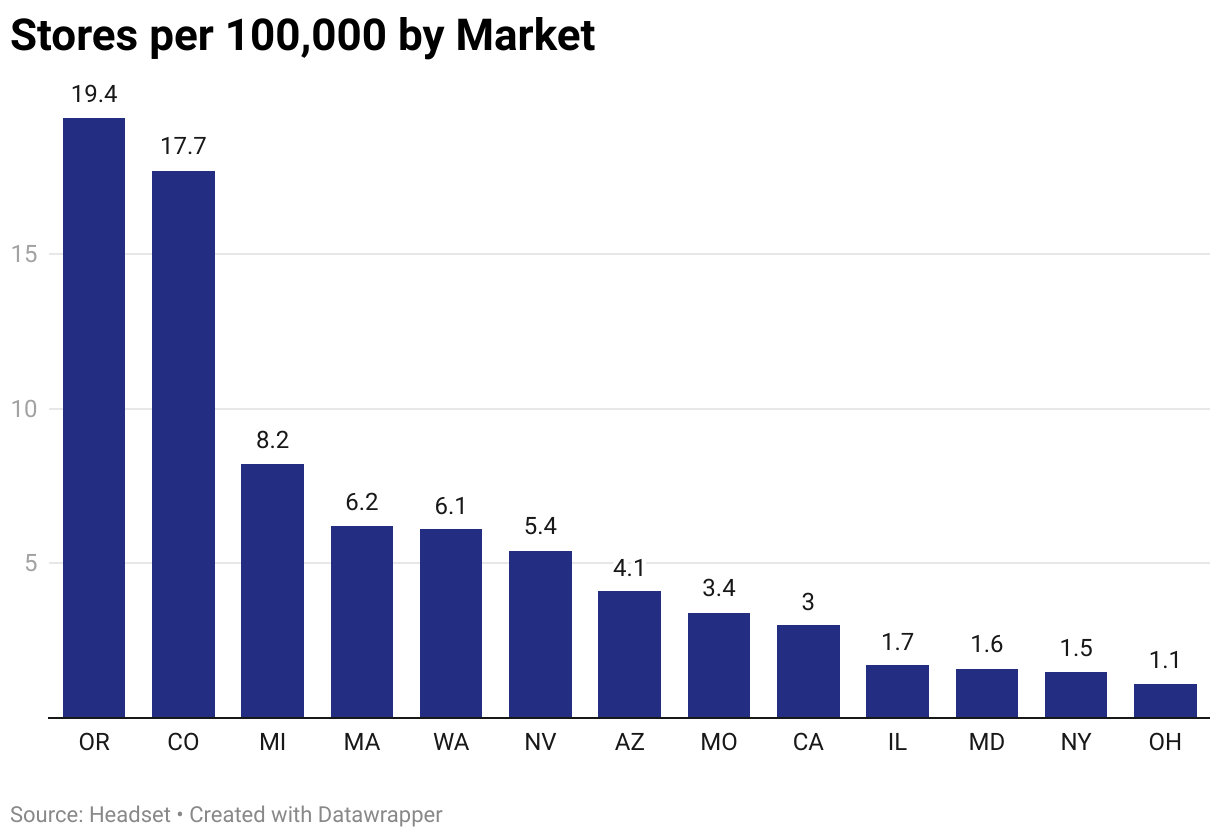

When we look at other midwestern markets with similar population sizes like Michigan (10.1M) or Illinois (12.8M) we can see that the Ohio (11.8M) market has potential to be one of the largest in the region and country. Geography has played a big role in vaulting both Michigan and Illinois to markets totaling in the billions of dollars. These first-to-market midwestern states have benefited from sharing borders with a lot of states without adult use recreational cannabis and this stands true for Ohio as well. Ohio borders five other states, four of which do not have access to recreational cannabis and will likely bolster demand to Ohio’s newly launched market.

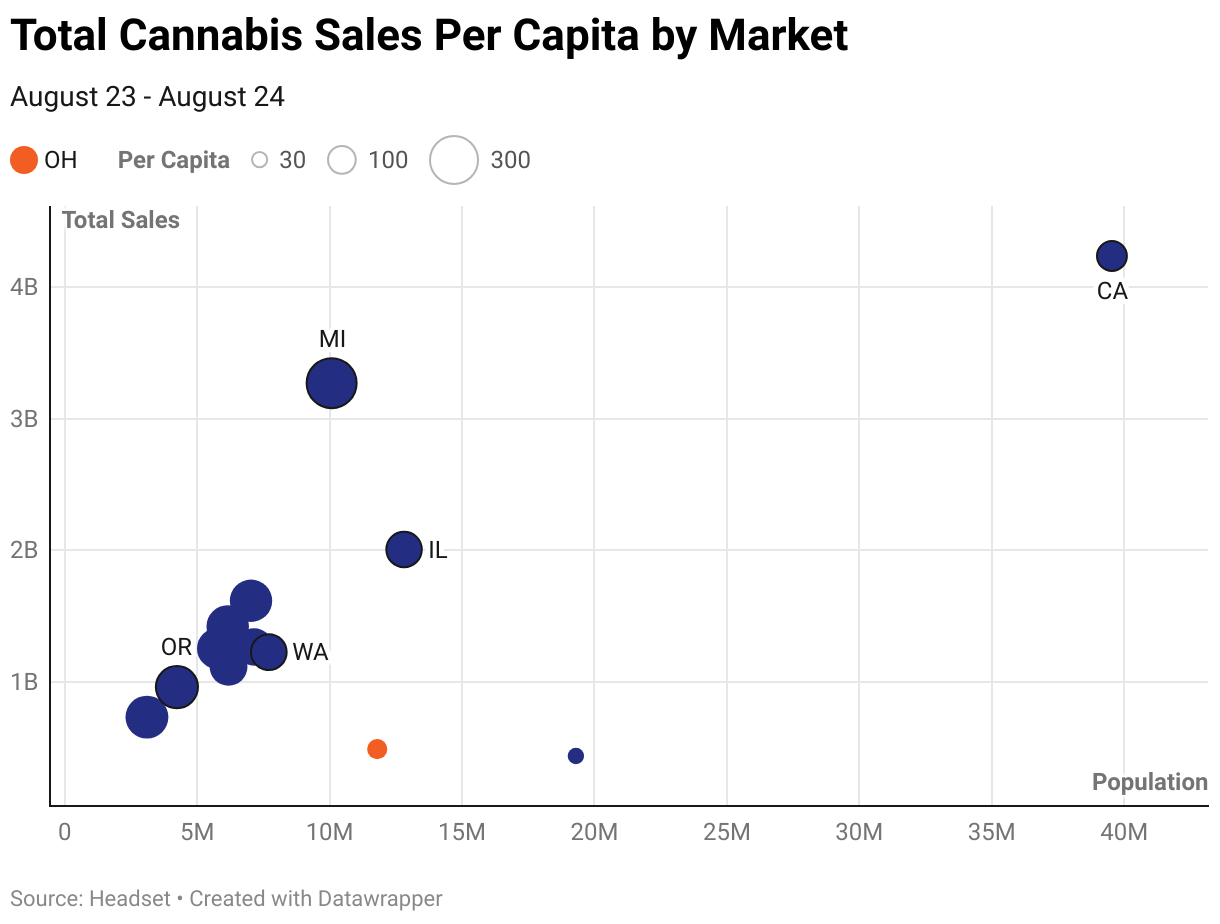

When it comes to per capita sales, Illinois and Michigan are at opposite ends of the scale. In Illinois, the slow expansion of stores across their state as well as high prices have kept sales fairly low for the sixth most populous state in the country. With a sales per capita of $156 Illinois lags 12% behind the US average of $178. Michigan on the other hand has an impressive sales per capita of $325 which is a shocking 83% higher than the average. Low prices and a lax regulatory environment has lead to a market generating over $3.2B in sales annually for the state.

If we apply our average sales per capita rate of $178 to Ohio’s population of nearly 12 million that puts a potential market size of over $2.1B in total sales at maturity. At $2.1B in total yearly sales as of today that would make Ohio the third largest of Headset’s tracked markets, behind only California and Michigan.

The number of authorized retailers in a market has a big effect on how we see sales grow after market launch. In both Missouri and Maryland the licenses were issued around the official launch date and have been stagnant up until this summer. In New York, retailer licenses have been issued on a rolling basis. As more stores get up and running, more customers are able to access the new recreational markets and we see that sales total increase in unison.

Ohio has a mixed approach, initially the state granted 123 licenses from their preexisting medical market stores. However, in order to meet the demand the state announced they will be doubling their license count with an additional 121 retailers surely leading to total sales growth throughout the year.

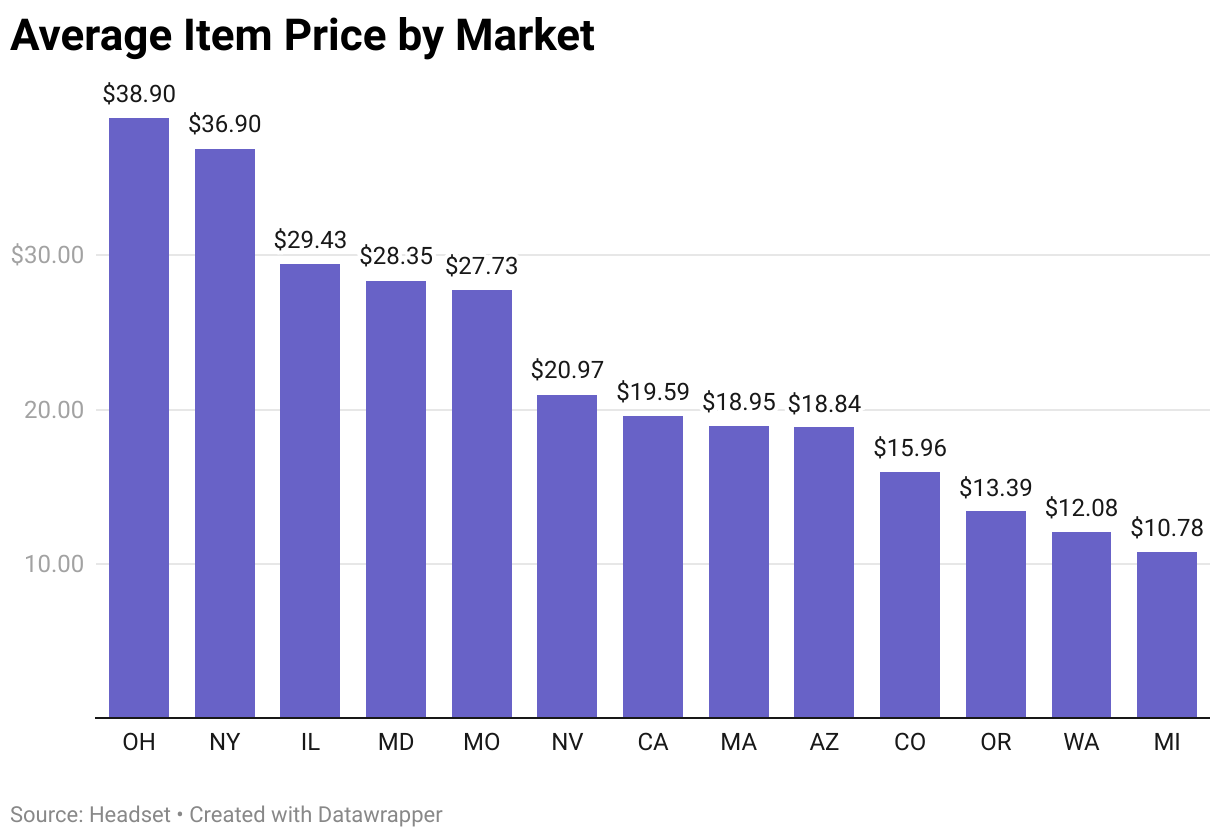

In addition to access through an appropriate amount of retailers, pricing greatly affects sales totals. Currently, OH has the highest prices in the country around $38.90 for the average item as of September 2024. This is typical for being the most recent adult-use market to launch. However, their ability to be competitive in the region, in particular with bordering Michigan, depends on pricing becoming competitive. Illinois began recreational sales in 2020 and they still have higher prices than Missouri and Maryland who just launched last year. Michigan’s high store count and low prices certainly cut into the margin of retailers, but if the Ohio market can find that sweet spot of competitive pricing and a healthy amount of stores than that will help keep a lot the their domestic business, particularly along the borders, in the state.

Conclusion

Each market has its own regulations, culture, competitive landscape, and economics. However, we can see that Ohio has every possibility of exceeding $2B in annual sales once it fully matures making it one of the largest markets in the Midwest and throughout the US. Getting pricing to come down to a competitive level and managing licenses to optimize access across the state will allow the state to grow over the course of the next year and beyond. With all eyes on this massive market Headset has the data retailers, brands, and operators in the state need to be successful.