The New Jersey Cannabis Market in 2025: Growth, Challenges, and Opportunities in the Garden State

.png)

Introduction

A voter-approved ballot initiative made New Jersey the 14th U.S. state to legalize adult-use cannabis. In April 2022, recreational cannabis sales began, adding a new cultivated crop to the Garden State. New Jersey's high population and density positions it to become a key market in the developing Northeast cannabis industry. Our report examines the first few years of business and compares it to the national market, highlighting both current barriers for brands and operators as well as future opportunities for cannabis in New Jersey.

Methodology

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally directly from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. In this report, we examine sales from US Headset Insights markets. This includes AZ, CA, CO, FL, IL, MA, MD, MI, MO, NJ, NV, NY, OH, OR, and WA.

Key Takeaways

- New Jersey generated over $1B in cannabis sales in 2024. Sales saw a 17% increase when comparing the start of 2025 to the same period in 2024.

- Retailers in New Jersey have average daily sales over $17k which is relatively high compared to the rest of US markets.

- Consumer category preferences resemble the rest of the country, though Concentrates and Beverages are underrepresented, likely a symptom of high prices in those categories.

- New Jersey has the second-lowest number of brands (152) and SKUs (6,060) of any US market. However, product count has grown 158% in the past year and continues to steadily increase.

- New Jersey maintains some of the highest cannabis prices nationwide, though these prices are declining at an increasingly rapid pace.

- Declining prices are driving down basket sizes, while the average number of items per basket remains steady. The market is transitioning from seller-driven to buyer-driven, leading to increased discounting.

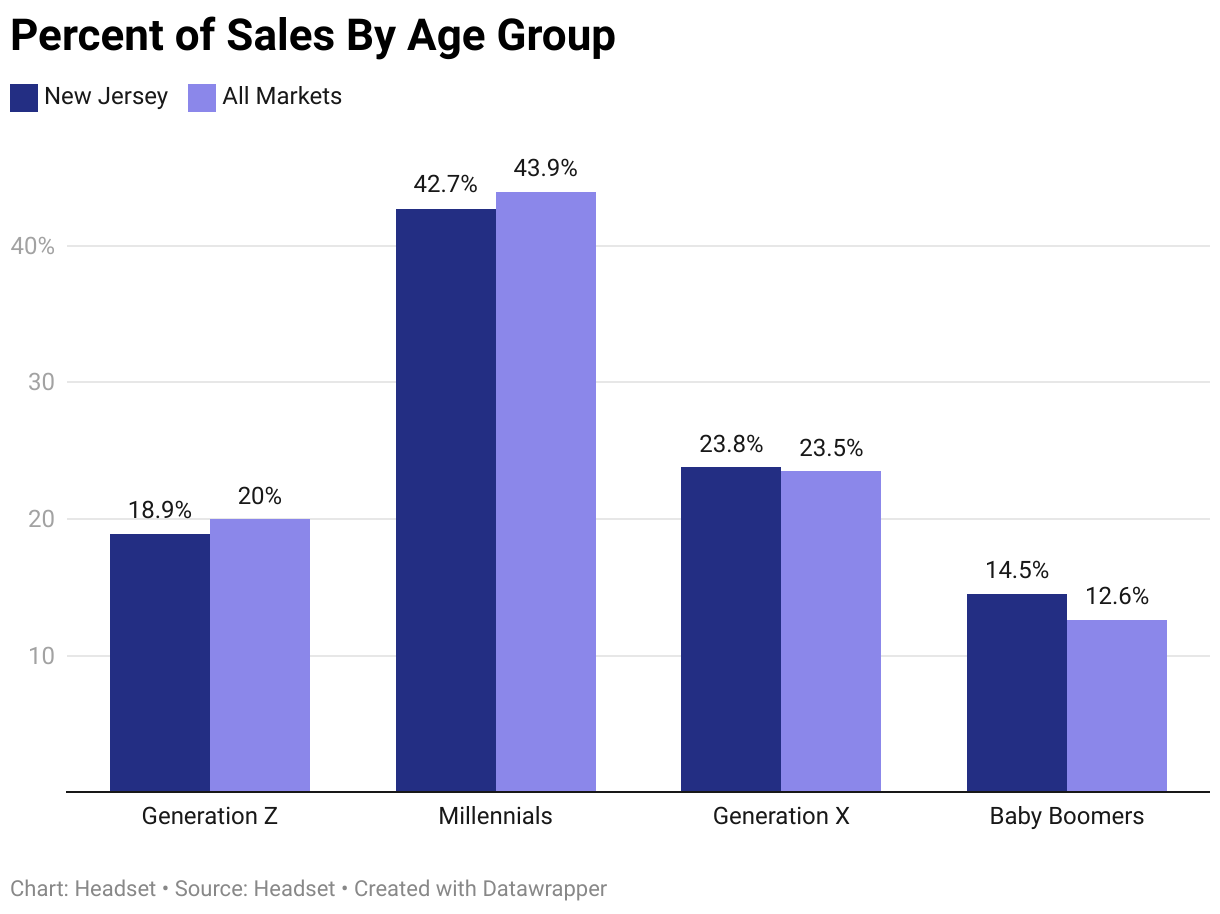

- While Millennial men generate the bulk of sales, there is a higher representation of older consumers and men in New Jersey compared to the rest of the US.

Sales Overview

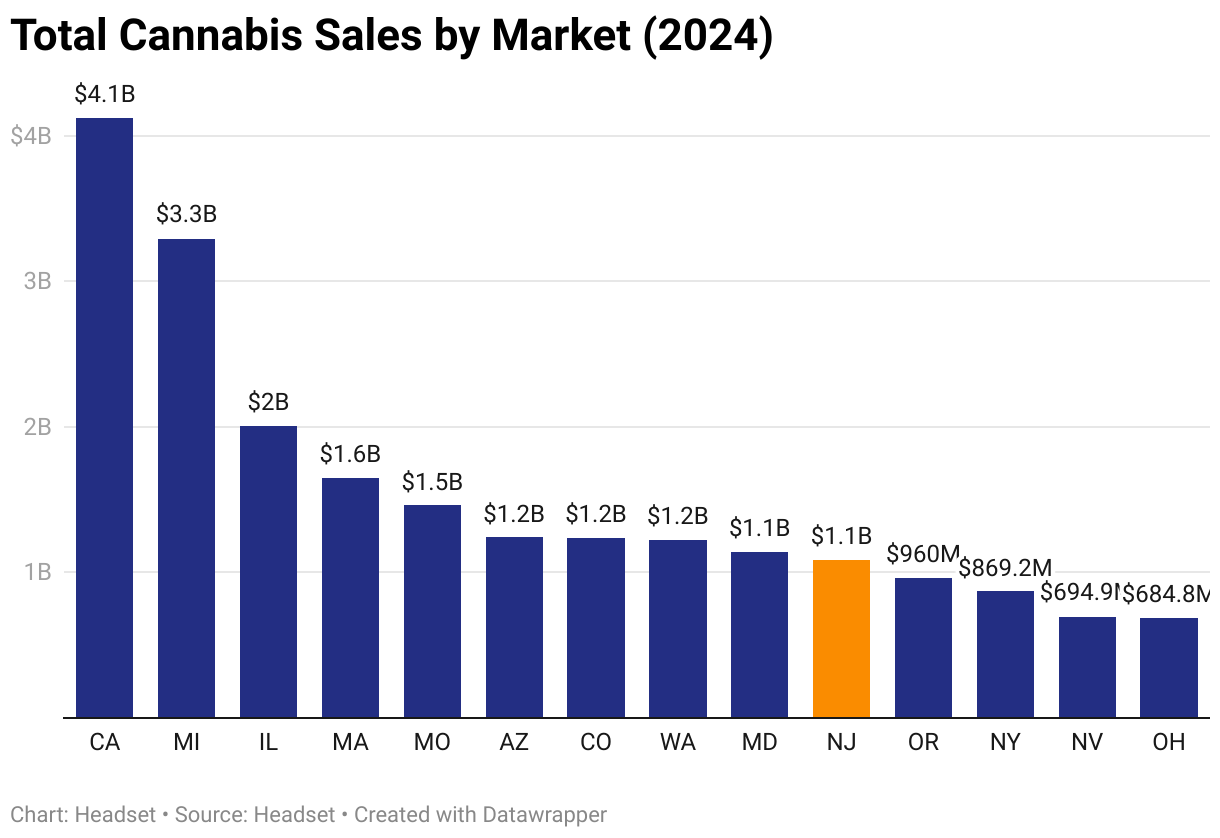

In 2024, New Jersey cannabis retailers surpassed $1 billion in sales, placing the market size on par with markets like Oregon and Maryland.

Sales have grown significantly over the last few years. Comparing the first three months of 2025 to the same period last year, New Jersey's sales have increased by 17%. This growth is substantial, trailing only New York and Ohio—both newer markets. However, as the market matures, there are signs that this growth rate is beginning to slow.

Compared to other markets nationwide, New Jersey retailers perform well, with average daily sales of around $17,000. However, the market faces evolving challenges: falling prices, an increasing number of stores, and a more competitive brand and product landscape. While stores have benefited from high basket totals in recent years, the growing competition means retailers must adapt to changing consumer behavior and market conditions as this young market matures.

Category Assortment

New Jersey's category preferences align with national trends, with some notable differences. Customers show a slight preference for Vapor Pens and Edibles—two categories growing in popularity—suggesting New Jersey consumers may be ahead of the curve. Conversely, Concentrates are significantly underrepresented, which matches the category's declining market share in other regions. Beverages are also underrepresented in New Jersey, presenting a potential opportunity given the category's modest but growing popularity nationwide.

Brand & Product Landscape

New Jersey has one of the lowest brand counts in the country, with only 152 distinct brands—surpassing only Maryland's 132. With Missouri and Ohio also at the bottom of the list, this limited brand presence likely reflects New Jersey's status as a newer market, suggesting opportunities for new competitors to enter.

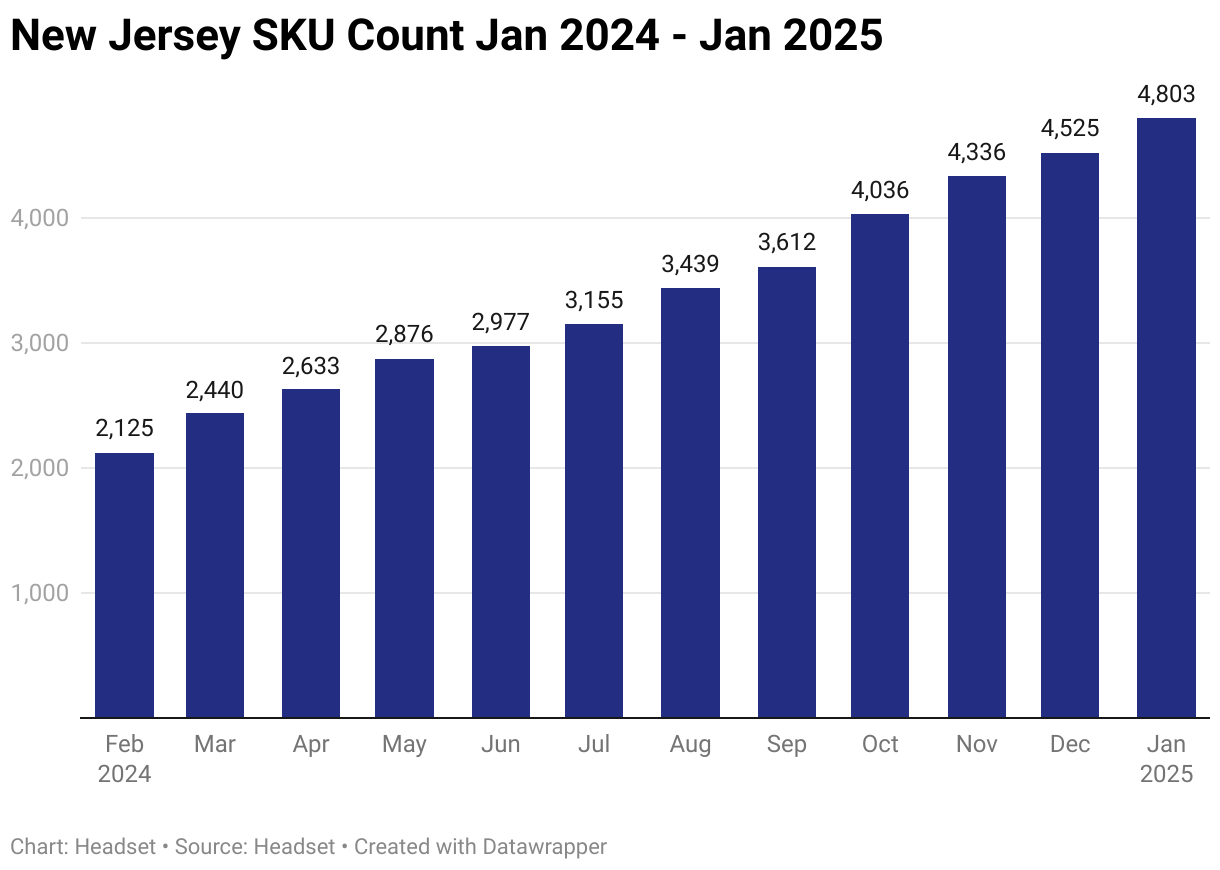

The number of SKUs in the market aligns with the brand count. With just over 6,000 distinct products, New Jersey's selection is limited compared to more mature markets like Oregon, which has nearly 20,000 unique products on dispensary shelves.

There has been strong growth in both the number of brands and the number of distinct products on New Jersey shelves. While the selection is light compared to other markets the number of SKUs grew 158% between January 2024 and January 2025.

Top Products

.png)

Pricing

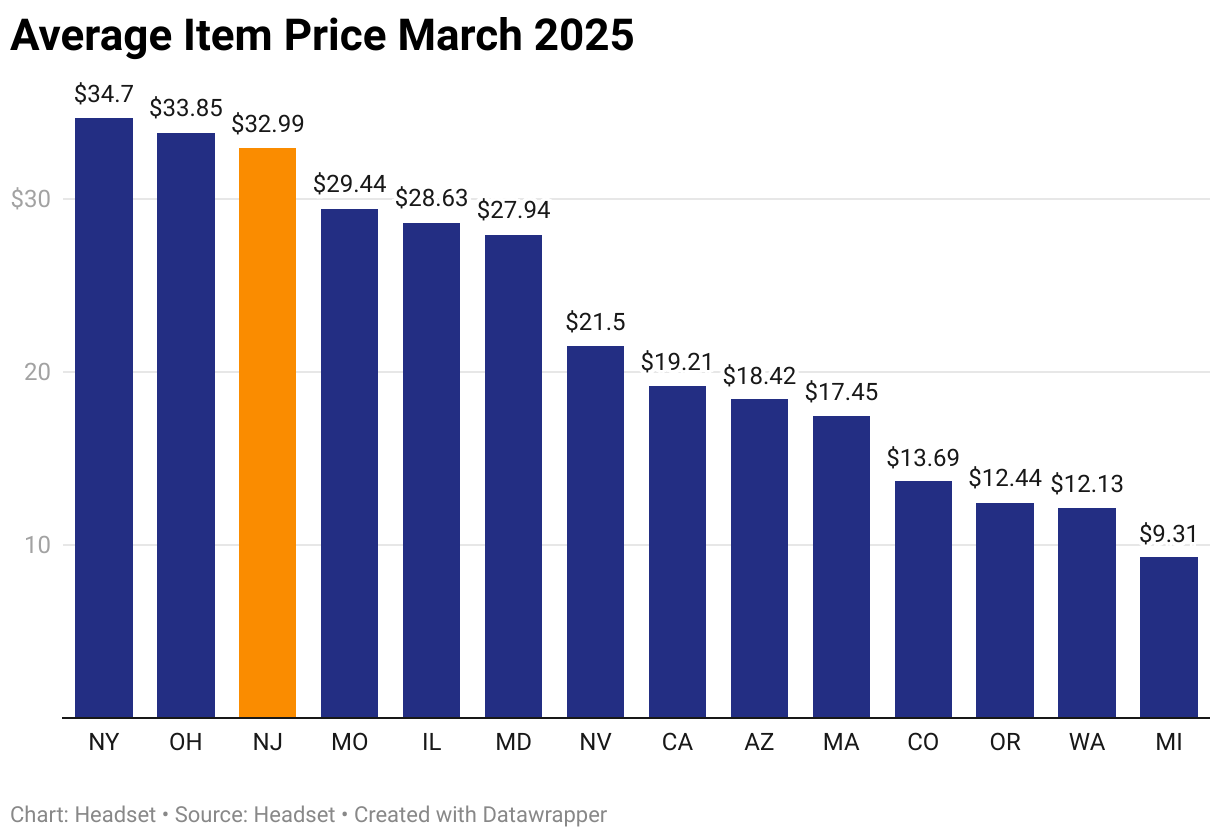

New Jersey has some of the highest prices in the country, with an average item price (AIP) of nearly $40 across all categories—significantly higher than the $23.50 AIP across other tracked markets. Beverages in New Jersey cost 241% more than in other markets, while Concentrates are 153% higher, which helps explain why these categories are less popular among New Jersey consumers.

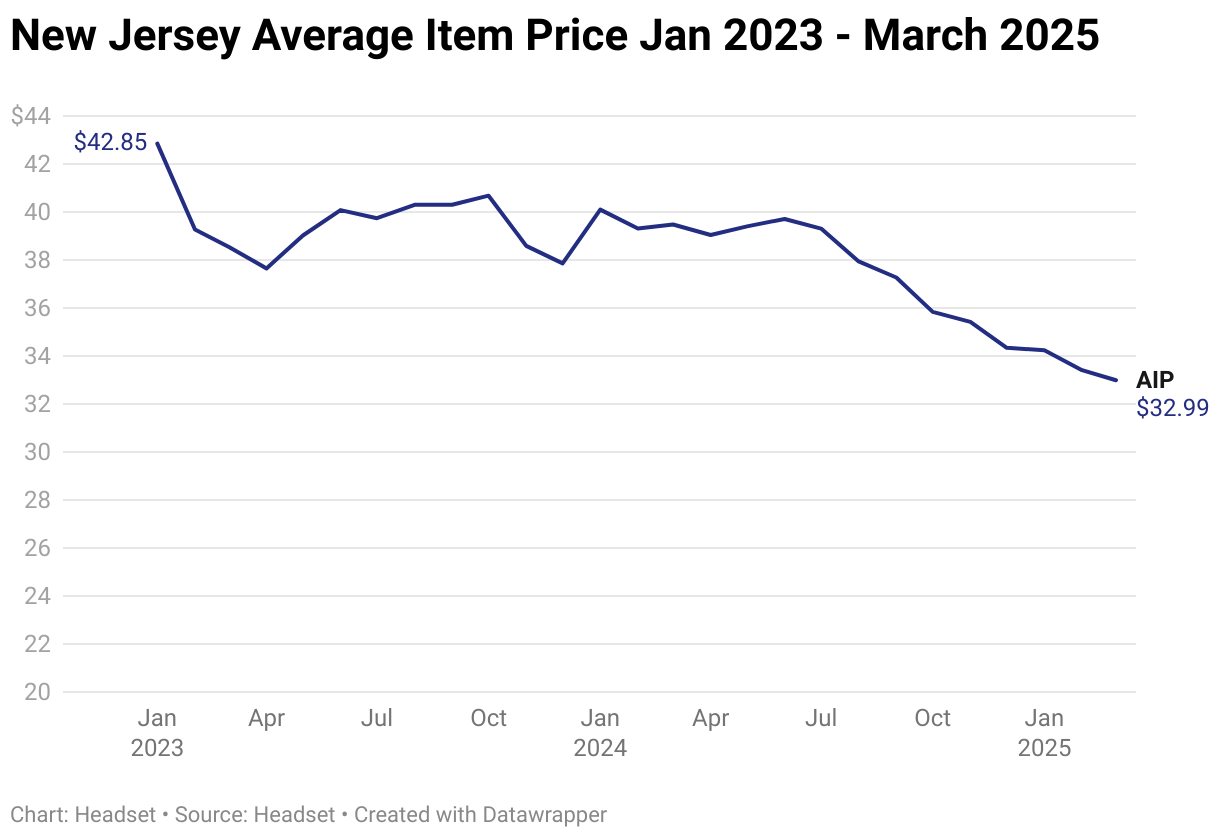

It's typical for newer markets to have high prices that gradually fall to more competitive levels. Between March 2023 and 2024, the Average Item Price (AIP) in New Jersey decreased by only 3%. However, from March 2024 to March 2025, AIP dropped by 16%. While prices remain higher than other markets, they are falling at an accelerating rate—a trend consistent with increased competition in the state.

Basket Analysis

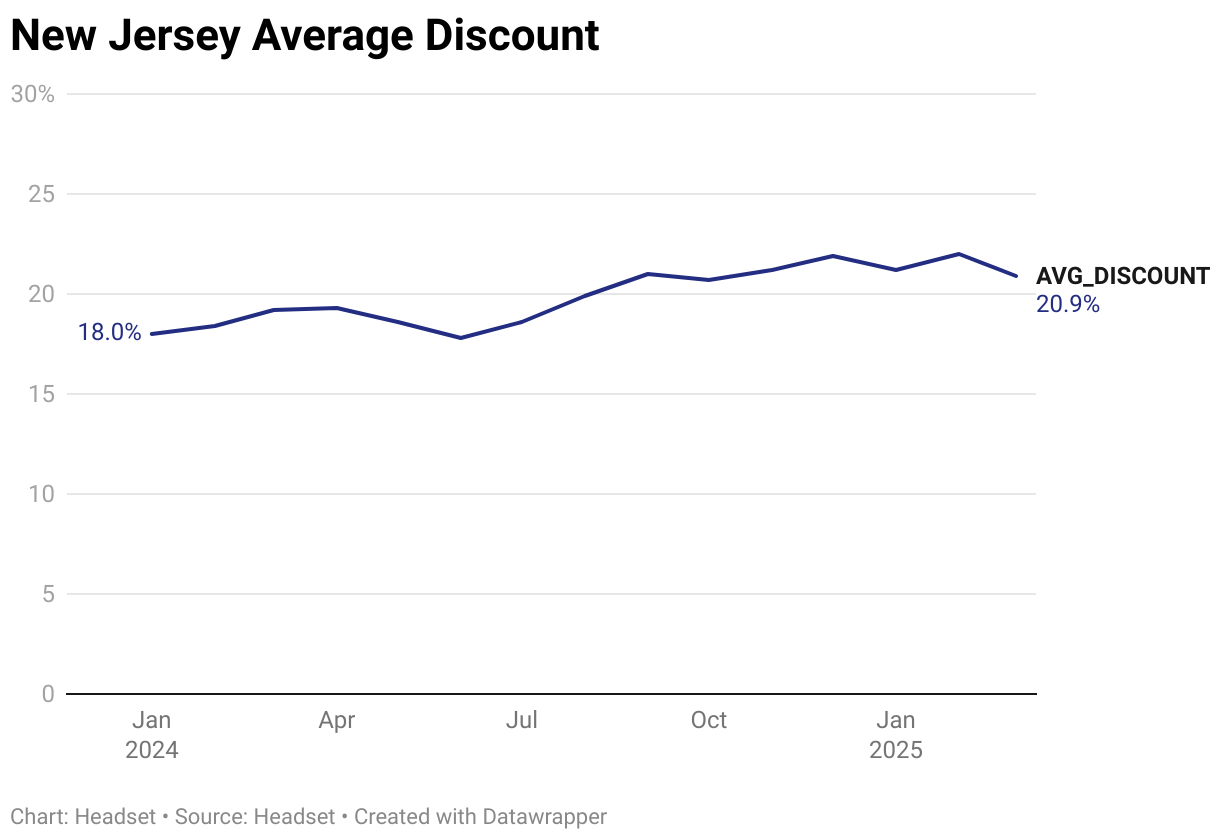

With an average basket size of nearly $72, New Jersey has one of the highest average basket sizes in the country. This is heavily correlated with prices, which have been high in New Jersey since recreational sales began in 2022. As prices have fallen, so have the average basket sizes—dropping 20% between March 2024 and March 2025.

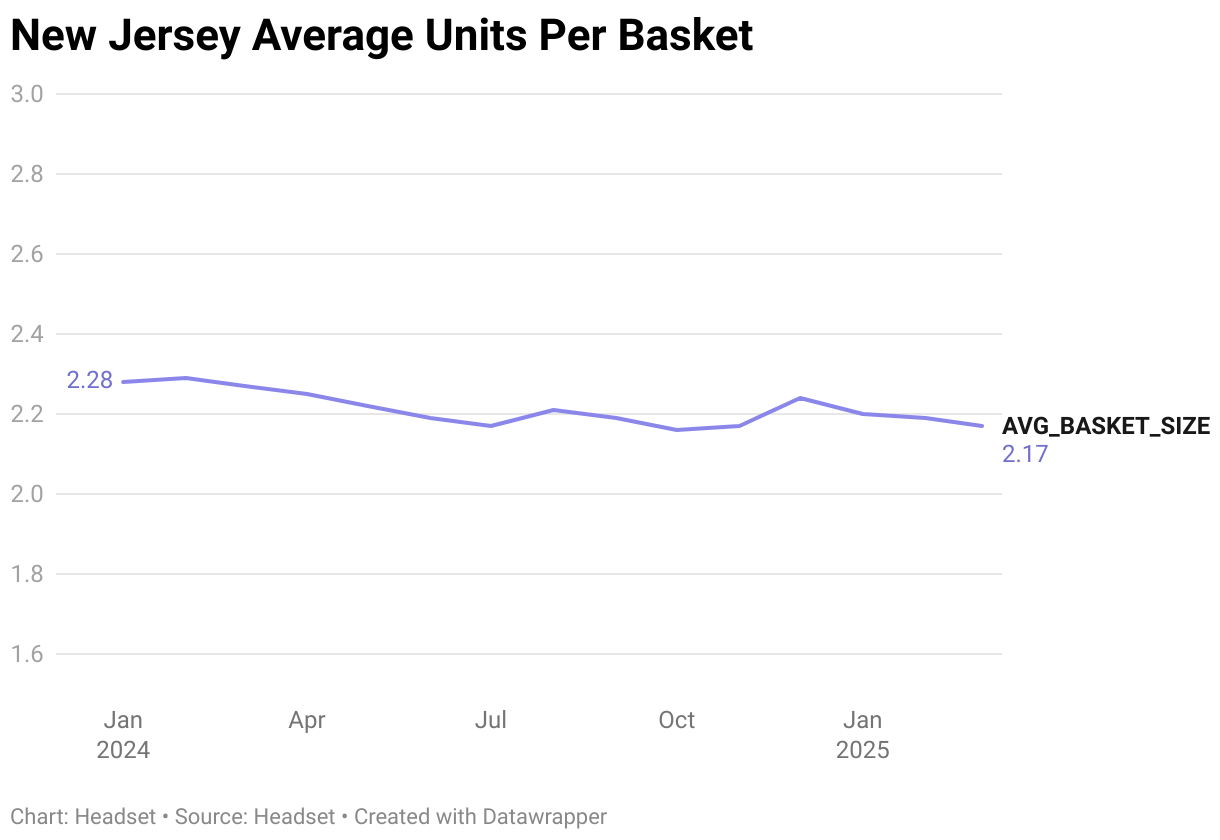

As prices fall, the total amount spent naturally decreases. However, retailers can offset shrinking basket sizes by encouraging customers to purchase more units at the lower prices. New Jersey's current average of 2.2 units per basket falls below the national average of 2.5. To reverse this trend, retailers should focus on upselling and cross-selling strategies.

The market in New Jersey is shifting toward a buyer's market. As more stores enter and compete for business, discounts are increasing to attract customers' attention. With discounts eating into retailer margins, it's crucial to use promotional strategies that encourage upselling and cross-selling to drive larger basket sizes.

Demographics

While Millennials drive the largest portion of overall cannabis sales, Baby Boomers represent a higher share of the market in New Jersey compared to other regions. This aligns with New Jersey's higher median age than the U.S. average.

Nationwide, men account for approximately 65% of total cannabis sales. In New Jersey, this figure is slightly higher at 68%.

Conclusion

While New Jersey's cannabis market has been operating since mid-2022, it remains in a maturing phase. The last few years have been a seller's market, with modest product selection, limited access, and high prices enabling retailers to achieve some of the highest average daily sales nationwide. However, the market is clearly shifting toward a more competitive environment. As new brands and products enter the market, prices are falling and reducing basket sizes. Meanwhile, new retailers are creating stiffer competition for existing operators, leading to higher discounts that cut into margins. With the market becoming more competitive, it's more important than ever for businesses in the state to have comprehensive information to improve operational efficiency, develop high-demand products, and maintain clear visibility into their business operations and market trends.