Mar-2025

Sales

Trend

6-Month

Product Count

SKUs

Overview

Market Insights Snapshot

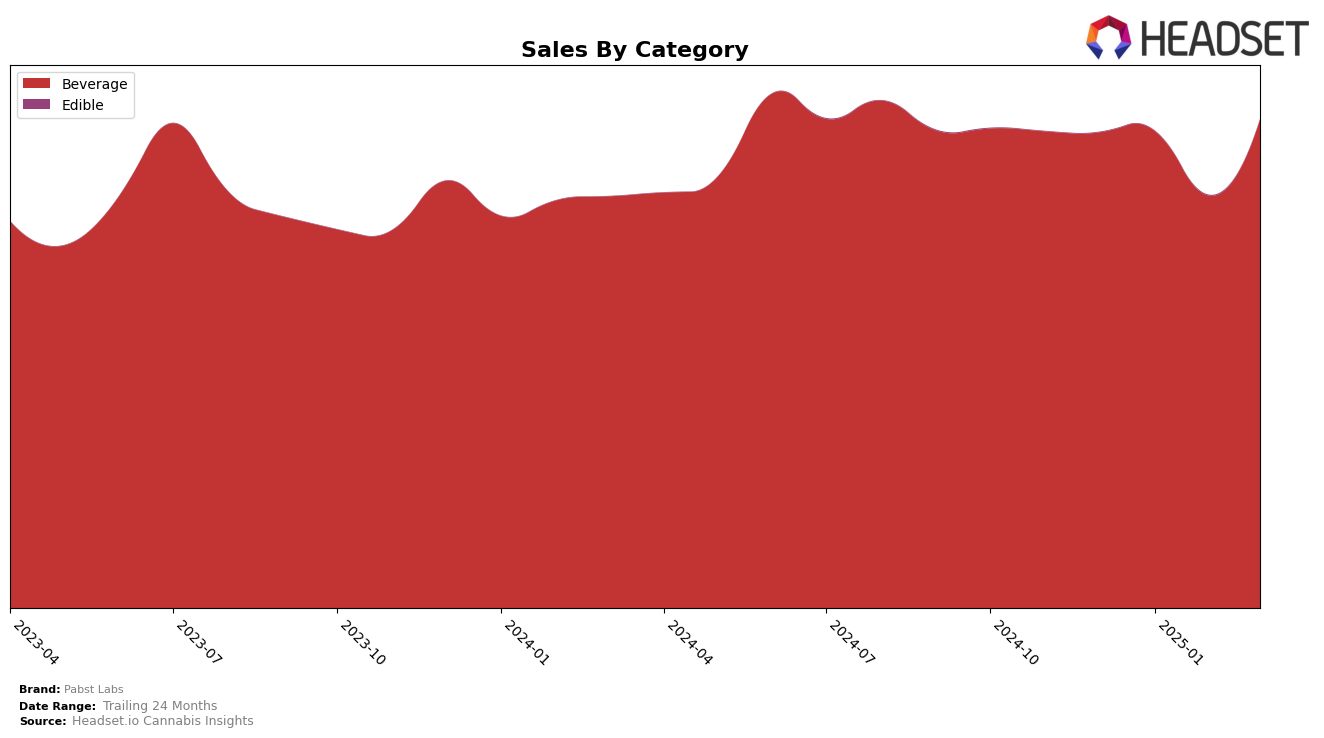

In the highly competitive cannabis beverage category, Pabst Labs has shown consistent performance in California. Over the months from December 2024 to March 2025, Pabst Labs maintained a steady presence, ranking fifth in December before slipping slightly to sixth place from January through March. Despite this minor drop in ranking, the brand demonstrated resilience with a notable increase in sales from February to March, indicating a positive trend in consumer demand. This consistent ranking within the top 10 highlights Pabst Labs' solid foothold in the California cannabis beverage market, although the slight rank drop suggests there may be increasing competition or shifts in consumer preferences that the brand needs to address.

Interestingly, the data reveals that Pabst Labs did not appear in the top 30 brands for any other state or province, which could be interpreted in multiple ways. On one hand, this absence might suggest a focused strategy on dominating the California market, capitalizing on its large consumer base and established distribution networks. On the other hand, it could indicate potential growth opportunities in other regions where the brand is currently underrepresented. The lack of presence in other markets might highlight either a strategic choice or a gap that could be filled with targeted expansion efforts. Such insights could be crucial for stakeholders looking to understand the brand's market dynamics and potential areas for growth.

Competitive Landscape

In the competitive landscape of the California cannabis beverage market, Pabst Labs has maintained a steady presence, although it has faced challenges in climbing the ranks. From December 2024 to March 2025, Pabst Labs consistently held the 6th position, except for December when it was ranked 5th. This stability, however, contrasts with the upward momentum of Not Your Father's Root Beer, which improved its rank from 6th to 4th over the same period, indicating a potential threat to Pabst Labs' market position. Meanwhile, Manzanita Naturals maintained a strong foothold in the top 5, only dropping from 4th to 5th in March 2025, while Lagunitas and Almora Farms remained stable at 8th and 7th positions, respectively. Pabst Labs' sales figures show a fluctuating trend, with a notable dip in February 2025, which may have contributed to its inability to advance in rank. This competitive environment suggests that while Pabst Labs is holding its ground, strategic efforts may be needed to boost sales and improve its ranking against rising competitors.

Notable Products

In March 2025, the top-performing product from Pabst Labs was Cherry Limeade Soda Pop (25mg THC, 12oz), maintaining its first-place ranking consistently since December 2024, with sales reaching 8,561 units. High Seltzer - THC/THCV 2:1 Daytime Energy Guava Seltzer (10mg THC, 5mg THCV, 12oz) also held its position in second place, showing stable demand. Strawberry Kiwi High Seltzer (10mg) climbed to third place, surpassing High Seltzer - CBD/CBN/THC Midnight Berries Seltzer (2mg CBD, 10mg THC, 3mg CBN, 12oz, 355ml), which dropped to fourth. Lemon High Seltzer (10mg THC, 12oz) remained steady in fifth place throughout the months. This data highlights the consistent popularity of the Cherry Limeade Soda Pop and the growing preference for the Strawberry Kiwi High Seltzer among consumers.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.