Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Simply Herb is stocked at 432 licensed dispensaries across Illinois, Massachusetts, and 4 other states, 160 of them in Illinois, with the deepest coverage in Chicago, East Peoria, Naperville, Normal, and Peoria. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

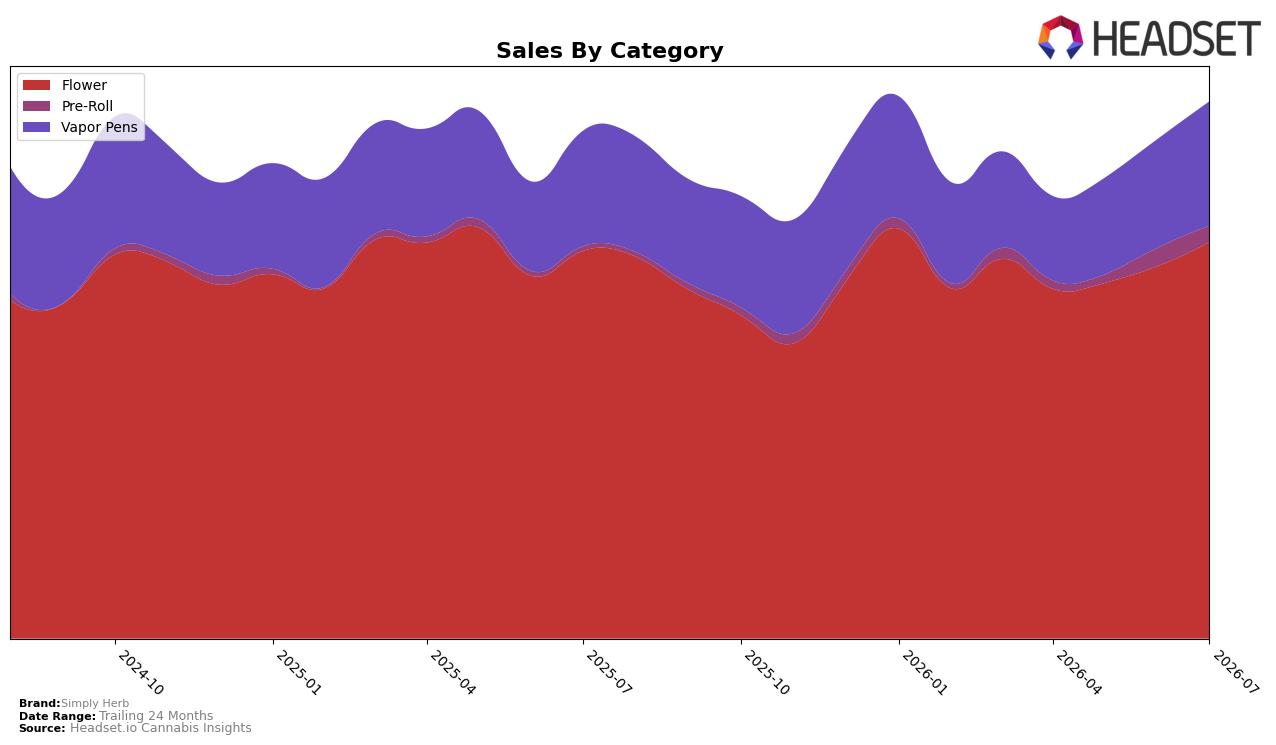

In July 2026, Simply Herb concentrated 68.07% of sales in Flower with a 2.17% year-over-year lift and a 6.00% month-over-month gain, while Vapor Pens held 24.63% share with 6.07% YoY growth and an 11.28% MoM rise; Pre-Roll accounted for 7.30% share with 33.18% YoY growth but a 5.16% MoM decline. Average price fell 13.63% YoY to $23.21 even as total brand sales grew 4.90% YoY, and the brand ranked 2 in Flower within Massachusetts. The pattern implies a volume-led expansion anchored in Flower and reinforced by accelerating Vapor Pens, offset by short-term softness in Pre-Roll, positioning the portfolio to trade on price elasticity rather than mix-led premiumization.

With Flower at 68.07% share and rank 2 in Massachusetts Flower, the 6.00% MoM gain versus an 11.28% MoM rise in Vapor Pens suggests incremental growth is migrating toward inhalables that can scale quickly as prices contract 13.63% YoY; meanwhile, Pre-Roll’s 33.18% YoY growth but 5.16% MoM pullback indicates episodic demand sensitivity. Taken together with a 4.90% YoY brand sales increase and a 9.04% 24‑month expansion, the mix shift implies Simply Herb’s near-term positioning is to prioritize high-velocity Flower while using Vapor Pens as the marginal growth engine, accepting lower average prices to capture share rather than pushing premium tiers.

Competitive Landscape

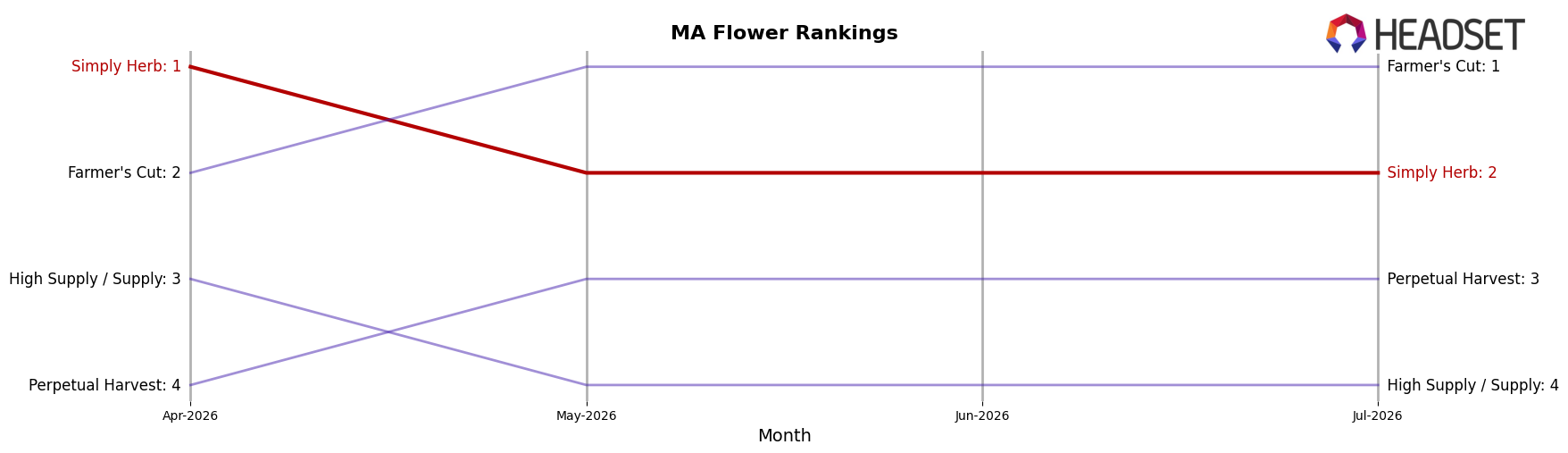

Simply Herb sits at rank #2 in Massachusetts Flower in July 2026, slipping 1 position year over year from #1, and retreating 1 spot from April 2026 when it held its peak at #1; by contrast, Farmer's Cut climbed from #4 to #1 while expanding sales by 56.7% year over year, and Perpetual Harvest improved from #3 to #3 with 36.9% YoY sales growth but did not overtake Simply Herb. The 1-rank slide since April 2026 alongside a 1-rank YoY decline, set against High Supply / Supply holding at #4 with 19.1% YoY growth and Root & Bloom jumping from #10 to #5 on 118.9% YoY growth, implies Simply Herb is defending share against faster risers and must counter accelerating competitor momentum to avoid further rank erosion.

Notable Products

Gorilla Chem (3.5g) posted the standout move with a 63.8% month-over-month surge to $287,646 and rose to rank 1, while Dungeons & Dragonfruit Distillate Cartridge (1g) slid 16.0% to rank 3. Fruity Loops Distillate Cartridge (1g) eased 7.2% at rank 4, and Tropical Thunder Distillate Cartridge (1g) gained 14.8% at rank 5, indicating mixed momentum within Vapor Pens where four of the top ten are Vapor Pens SKUs. The Pre-Roll set held steady with Sour Orange Pre-Roll (1g) up 14.0% at rank 2 and Lemon Fresh Pre-Roll (1g) up 17.8% at rank 7, balancing softer Vapor Pens trends with incremental gains.

The pattern implies Simply Herb is tilting toward a two-pillar mix where a resurgent top Flower SKU funds stability bets in Pre-Rolls while Vapor Pens depth remains important but requires sharper SKU-level curation.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.