Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

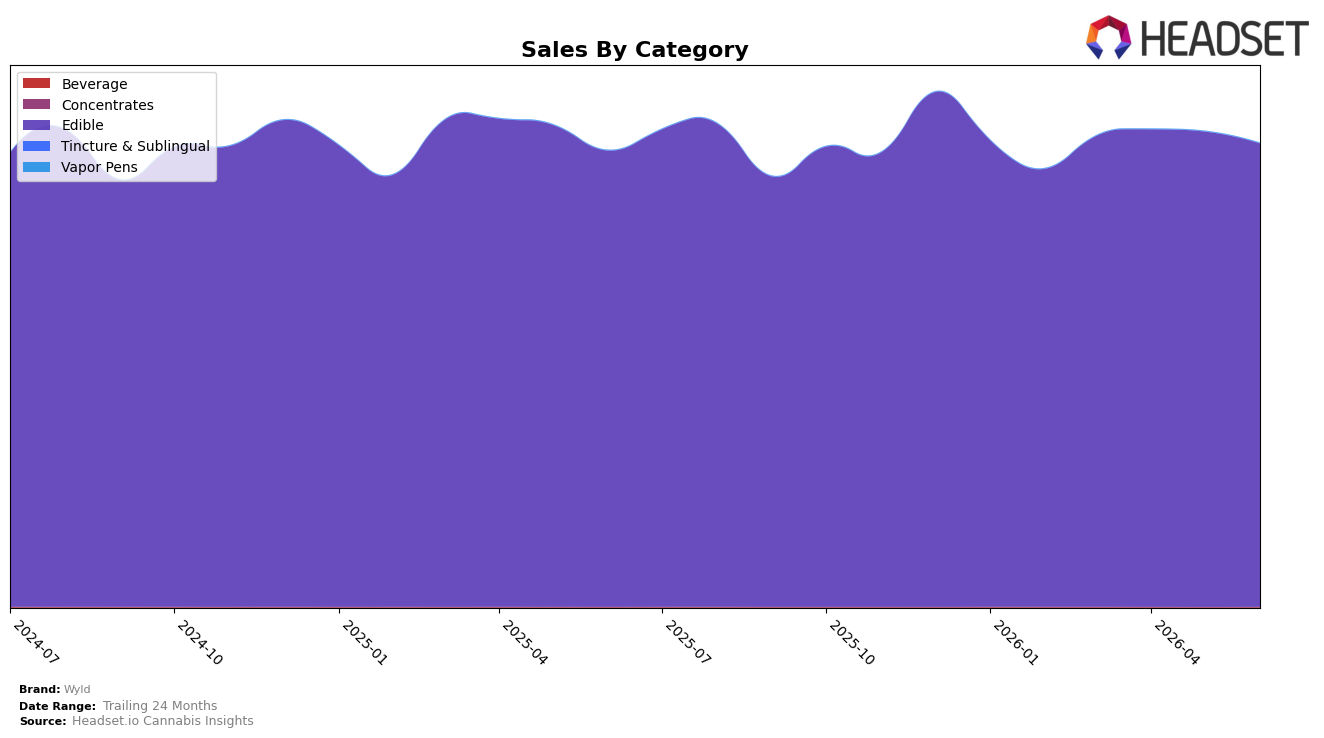

Wyld’s mix in June 2026 is overwhelmingly Edible at 99.95% share, with Edible sales down 2.52% month over month but up 1.56% year over year, while Beverage holds 0.05% share with a 27.71% MoM lift and a 1.76% YoY decline. Tincture & Sublingual remains a rounding-error slice at 0.002% share, but its triple-digit YoY of 1,017.48% and 19.42% MoM uptick signal a tiny but accelerating test. Average price rose 10.23% YoY to $15.10 as Edible average price reached $15.12, and the brand’s Edible rank is 1 in Arizona, indicating that despite a 2.52% MoM softening in the core, price-led contribution and category leadership anchor the portfolio. The pattern implies Wyld is still a single-category specialist using price and rank defense to offset a short-term Edible dip while cautiously probing adjacent formats.

The small but faster-moving edges—Beverage up 27.71% MoM off a 0.05% share base and Tincture & Sublingual surging 1,017.48% YoY—suggest a deliberate option-value strategy rather than a pivot, given Edible’s 99.95% share and 1.56% YoY growth. With average price up 10.23% YoY alongside a 2.52% MoM volume softness in Edibles, the mix points to pricing power and limited elasticity near-term, while the near-zero shares in the two minor categories cap risk. The implication is that Wyld’s positioning remains concentrated on Edibles with rank-led equity, using micro-scale experiments to hedge against further MoM variability without diluting the core.

Competitive Landscape

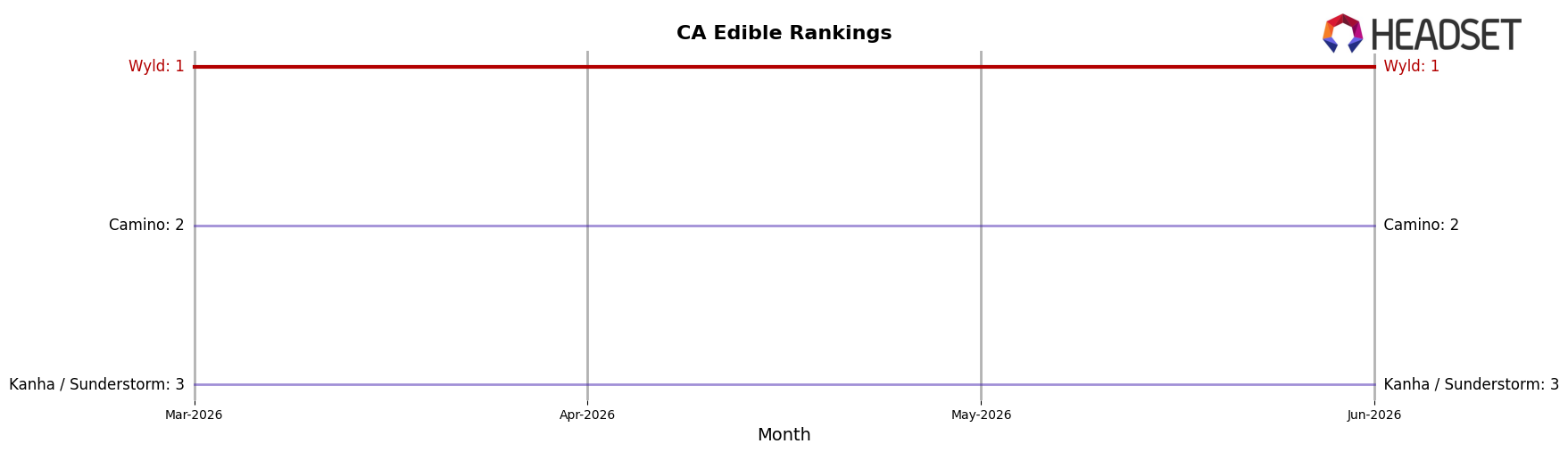

Wyld holds rank #1 in CA Edible for June 2026, unchanged from #1 in June 2025, while Camino remains #2 year over year and Kanha / Sunderstorm stays at #3; competitor sales growth is positive—Camino at 12.9% YoY and Kanha / Sunderstorm at 10.9%—yet neither converted those gains into a rank shift. Over the last three months Wyld has stayed #1 each period while Good Tide holds #5 with a 28.5% YoY sales increase, indicating growth is dispersing across followers without dislodging the leader. The pattern implies Wyld’s lead is anchored more by relative share stability than absolute growth rates, as rivals’ double-digit YoY gains have not translated into rank movement.

Notable Products

Wyld’s CBD/CBN/THC 1:1:1 Indica Boysenberry Gummies 10-Pack (100mg CBD, 100mg CBN, 100mg THC) stayed at rank 1 with a -2.3% month-over-month change, while THC/CBN 2:1 Indica Elderberry Gummies 10-Pack (100mg THC, 50mg CBN) held rank 2 at -0.9%, indicating leadership stability despite broad softening. Sativa Raspberry Gummies 10-Pack (100mg) remained at rank 3 with a -4.4% decline, and six of the top ten sat between ranks 5–10 with declines ranging from -3.4% to -7.9%, pointing to a synchronized downtick rather than product-specific issues. All ten top sellers are Edibles and share negative MoM movements between -0.9% and -7.9%, and the top three account for a consolidated demand center with one product alone generating $5,138,150, implying reliance on a concentrated edible core that may need flavor and ratio refreshes to re-ignite growth.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.