Mar-2025

Sales

Trend

6-Month

Product Count

SKUs

Overview

Market Insights Snapshot

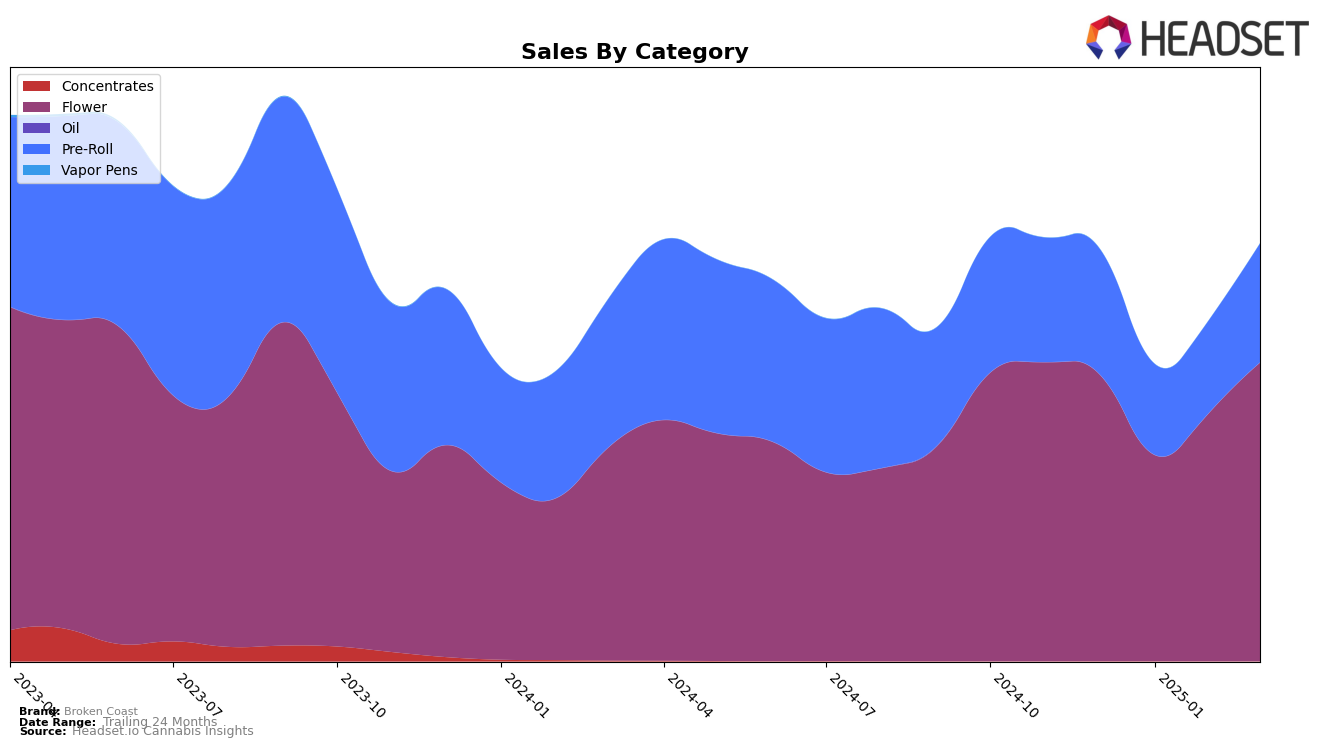

Broken Coast's performance across various Canadian provinces in the Flower category has shown notable fluctuations. In Alberta, the brand has demonstrated a strong upward trajectory, moving from the 11th position in December 2024 to the 9th position by March 2025. This indicates a positive trend, especially with March sales reaching 605,400 CAD, the highest in the observed period. Conversely, in British Columbia, Broken Coast's Flower category ranking has been less stable, declining from 24th in December to 30th in March. This suggests challenges in maintaining a competitive edge in this region. Meanwhile, in Ontario, the Flower category ranking improved slightly from 46th in December to 43rd in March, indicating a modest recovery after a dip in January.

In the Pre-Roll category, Broken Coast's performance has been mixed across the provinces. In Alberta, the brand showed a significant improvement, climbing from the 33rd position in December to 26th by March, suggesting a strengthening market presence. However, in British Columbia, the brand did not make it into the top 30, with rankings hovering around the 70s, indicating a need for strategic adjustments to boost its standing. In Ontario, Broken Coast remained outside the top 30, with rankings in the 70s throughout the observed months. This consistent position may reflect challenges in gaining traction in the Pre-Roll category within this province. Overall, while there are areas of growth, Broken Coast faces varying levels of competition and market dynamics across different regions and product categories.

Competitive Landscape

In the competitive landscape of the flower category in Alberta, Broken Coast has shown a dynamic shift in its ranking and sales performance from December 2024 to March 2025. Starting at 11th place in December, Broken Coast experienced a dip to 17th in January, before climbing back to 12th in February and achieving a notable 9th place in March. This upward trajectory in rank is mirrored by a significant increase in sales, culminating in a robust performance in March. In comparison, Redecan maintained a relatively stable position, consistently ranking higher than Broken Coast, although its sales showed some fluctuations. FIGR also demonstrated consistent rankings, often outperforming Broken Coast, but with a slight decline in March. Meanwhile, Castle Rock Farms and Space Race Cannabis have been close competitors, with Castle Rock Farms showing a similar sales surge in March. These insights highlight Broken Coast's resilience and potential for growth amidst a competitive market, suggesting a strategic opportunity to leverage its recent momentum to capture more market share.

Notable Products

In March 2025, Broken Coast's top-performing product was Platinum Pavé (3.5g) in the Flower category, achieving the number one rank with sales of 7,726 units. Emergen Z Blunt (1g) in the Pre-Roll category saw a significant rise, climbing from fifth to second place with impressive sales figures. Cherry Cheesecake Blunt (1g), also in the Pre-Roll category, dropped to third place from its previous top position in February. Ruxton Pre-Roll (0.5g) maintained a stable presence, ranking fourth, showing consistent sales performance over the months. Milk & Cookies Pre-Roll 3-Pack (1.5g) rounded out the top five, experiencing a slight decline in ranking from February.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.