Mar-2026

Sales

Trend

6-Month

Product Count

SKUs

Overview

Market Insights Snapshot

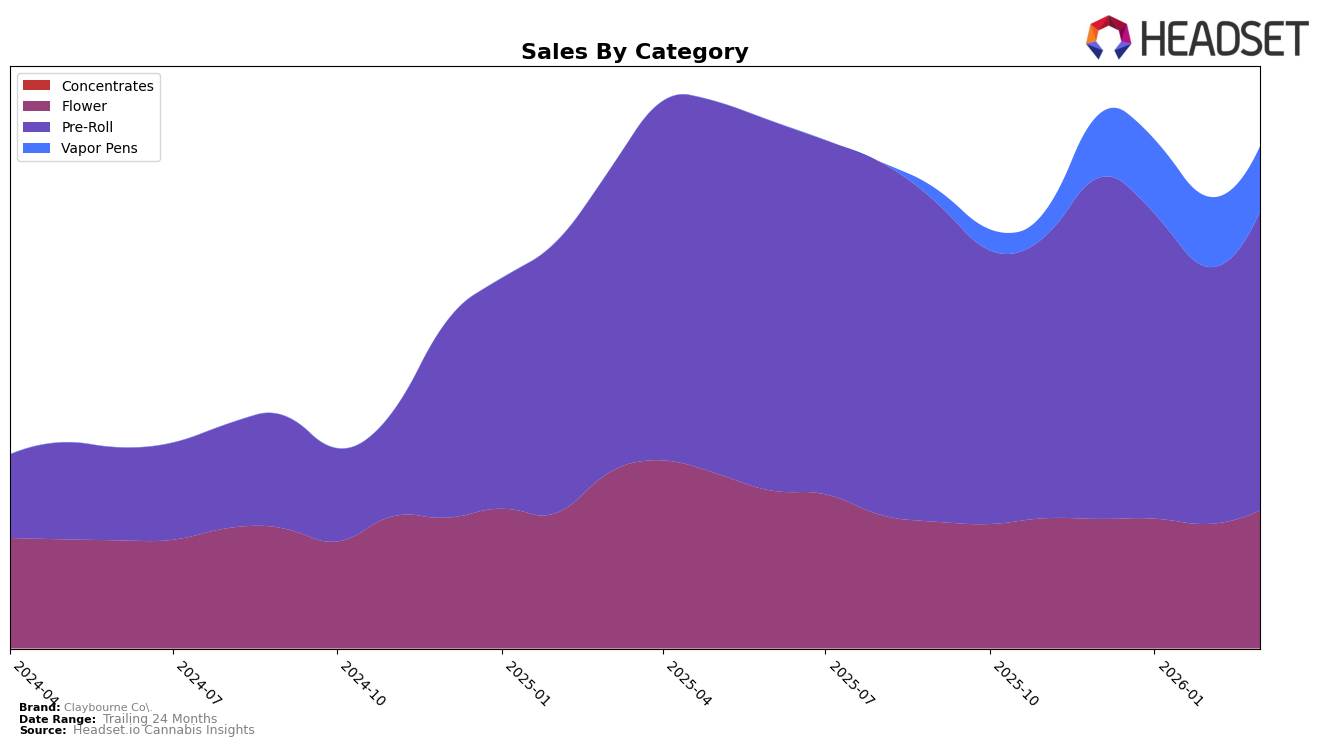

Claybourne Co. has shown a consistent performance in the Alberta market, particularly in the Pre-Roll category where it maintained a steady second position from December 2025 to March 2026. This stability indicates a strong foothold in the Pre-Roll market, despite a slight dip in sales from January to February. However, the Vapor Pens category in Alberta tells a different story, with the brand experiencing fluctuations in rankings, peaking at 15th in February before dropping to 26th in March. This volatility suggests challenges in maintaining a competitive edge in the Vapor Pens market within the province.

In California, Claybourne Co. has demonstrated resilience in the Flower and Pre-Roll categories, consistently ranking within the top 10. The Flower category saw a slight drop from 5th to 6th position in March 2026, while the Pre-Roll category improved from 9th to 7th position during the same period. Notably, the Vapor Pens category in California showed an upward trend from December to February, climbing from 36th to 25th, before dropping again in March. Meanwhile, in Ontario, the brand maintained a stable performance in the Pre-Roll category, consistently ranking 4th or 5th, while facing challenges in the Vapor Pens category, where it fell out of the top 30 in February. This indicates a need for strategic adjustments to enhance their presence in the Vapor Pens market across these regions.

Competitive Landscape

In the competitive landscape of the California flower category, Claybourne Co. has demonstrated a consistent presence, maintaining its rank within the top six brands from December 2025 to March 2026. Despite a slight fluctuation, moving from rank 5 in December and February to rank 6 in January and March, Claybourne Co. has shown resilience in its sales performance. Notably, Allswell consistently held the 4th position, indicating a stable market leader above Claybourne Co. Meanwhile, Blem and Alien Labs have been close competitors, with Blem occasionally surpassing Claybourne Co. in rank, particularly in January and March. Despite these competitive pressures, Claybourne Co.'s sales figures have shown a positive trajectory, especially in March 2026, suggesting a potential for upward movement in the rankings if this trend continues. This competitive analysis highlights the dynamic nature of the California flower market and underscores the importance for Claybourne Co. to leverage its sales momentum to climb higher in the ranks.

Notable Products

In March 2026, the top-performing product for Claybourne Co. was the Frosted Flyers - Variety Pack Infused Pre-Roll 5-Pack (2.5g), maintaining its first-place rank consistently from December 2025 through March 2026, with sales reaching 37,783 units. The Frosted Flyers - Hybrid Flight Pack Resin Infused Pre-Roll 5-Pack (2.5g) held steady in second place from January to March 2026, showing a notable increase in sales to 17,151 units. The Frosted Flyers - Berry Variety Infused Pre-Roll 8-Pack (2.8g) moved up from fifth place in December 2025 to third place by February 2026, maintaining this rank in March with sales of 12,441 units. Flyers - Blue Dream Frosted Liquid Diamond Infused Pre-Roll 3-Pack (1.5g) dropped from second in December 2025 to fourth by March 2026, while Flyers - Grape Gasolina Liquid Diamond Infused Pre-Roll 3-Pack (1.5g) re-entered the rankings in fifth place with 9,116 units sold in March. Overall, the rankings for these products remained relatively stable, with only minor shifts observed over the months.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.