Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Eureka is stocked at 354 licensed dispensaries across New York, Colorado, and 5 other states, 132 of them in New York, with the deepest coverage in New York, Queens, Buffalo, Farmingdale, and Rochester. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

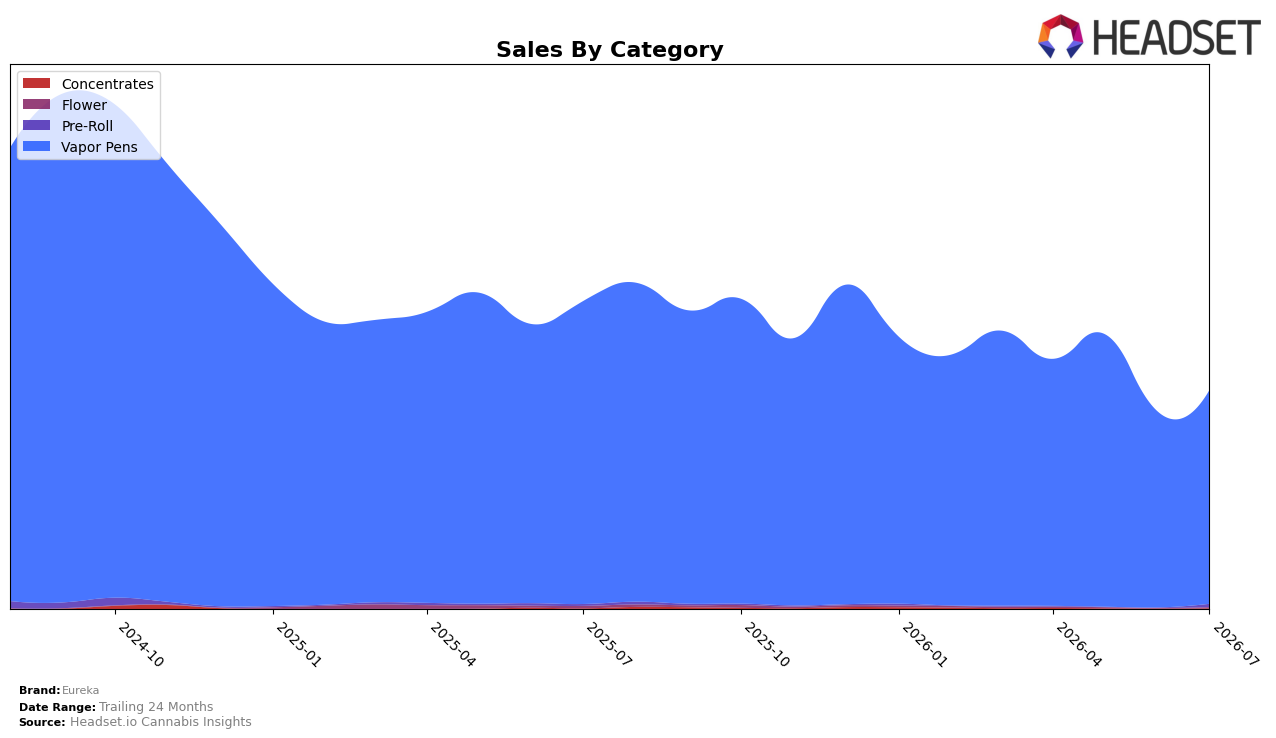

Eureka concentrated 98.10% of July 2026 sales in Vapor Pens, with that core down 29.49% year over year but up 9.26% month over month, while Pre-Roll held 1.33% share with 106.70% year-over-year growth and no reported month-over-month change. Smaller lines moved sharply: Flower at 0.29% share fell 67.05% year over year but jumped 227.27% month over month, and Concentrates at 0.27% share slipped 0.67% year over year but rose 86.65% month over month. Average price declined 1.14% year over year to $32.52, and in Colorado Vapor Pens the brand sat at rank 15; this mix and trajectory indicate reliance on a single category is softening year over year while near-term momentum and nascent diversification are beginning to offset it.

The combination of a 29.05% brand-level year-over-year sales drop alongside a 9.26% month-over-month lift in the 98.10% share core suggests Eureka’s base is stabilizing in the short term even as annual comparables remain negative, and the rank 15 position in Colorado Vapor Pens frames the brand as mid-pack rather than a share leader. Triple-digit month-over-month surges in Flower (227.27%) and strong month-over-month gains in Concentrates (86.65%) against tiny shares under 0.30% imply test-and-expand behavior that can add incremental reach without diluting the Vapor Pens focus, while a 106.70% year-over-year rise in Pre-Roll at 1.33% share points to a small but growing adjacency; taken together, the pattern implies Eureka’s positioning is evolving from a single-category specialist toward a slightly broader portfolio to buffer volatility in its mainline channel.

Competitive Landscape

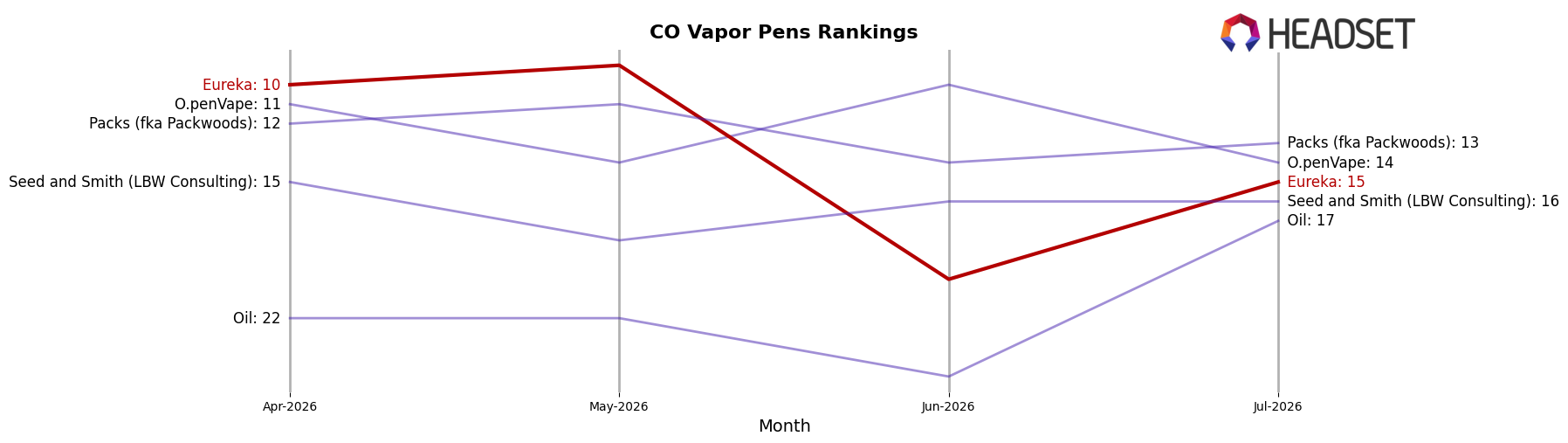

Eureka sits at rank #15 in CO Vapor Pens in July 2026, down 5 positions year over year from #10, and also down 5 positions versus April 2026 when it was #10; the brand once peaked at #3 in October 2024, a 12-rank spread from today. In contrast, Spherex held #1 year over year and remains #1, while Jetty Extracts jumped from #19 to #5 alongside a 181.35% YoY sales increase, and PAX moved from #3 to #2 with 21.69% YoY growth; this combination of Eureka’s 5-rank YoY decline and competitor ascents indicates share is consolidating toward faster-growing leaders, implying Eureka’s trajectory points to continued mid-tier pressure unless it reclaims momentum.

Notable Products

Gorilla Juice Live Resin Reload Pod (1g) stands out for the steepest movement in July 2026 with a -19.5% month-over-month drop to rank 4, while Slid3 - Melon Madness x Sour Applelicious Live Resin Disposable (1g) also declined -14.6% at rank 10. In contrast, Cherry Slushie Live Resin Reload Pod (1g) grew 8.2% to rank 6 and Slide - Strawberry Clemonade x Nectarine Dream Distillate Disposable 2-Pack (1g) rose 8.6% to rank 8, indicating mixed momentum within live resin formats. With nine of the top ten SKUs in Vapor Pens and multiple Classic distillate pods anchoring ranks 1–3 alongside a $33,071 2g entry at rank 5, the lineup tilts toward higher-capacity distillate as the volume engine while live resin variability creates selective upside and downside risk.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.