May-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

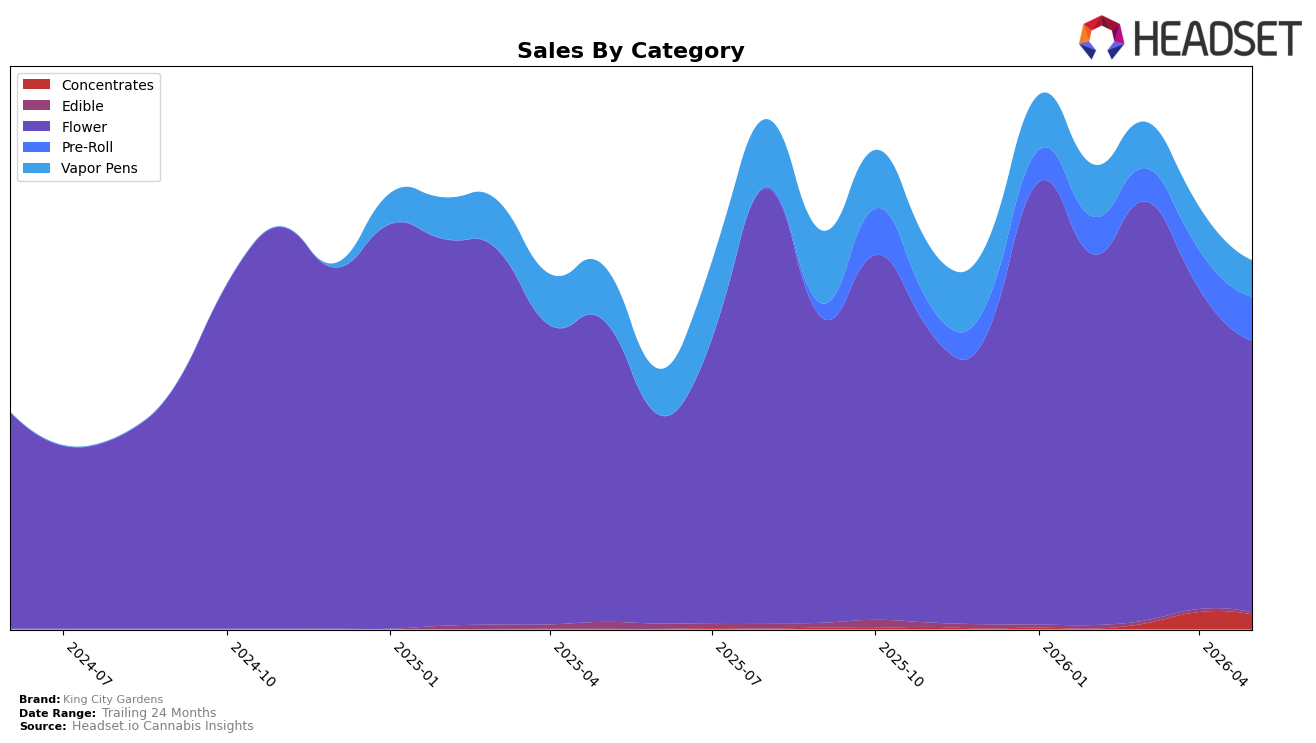

In May 2026, King City Gardens concentrated 73.78% of sales in Flower, where sales fell 10.01% year over year and 15.45% month over month, while Vapor Pens at 9.85% share declined 33.08% year over year and 15.98% month over month. Countering those drops, Pre-Roll rose 14.28% month over month to 11.91% share, and Concentrates, though only 4.01% share, posted a 4,478.03% year-over-year surge even as month-over-month slipped 13.62%. Edible contracted to 0.45% share with a 74.24% year-over-year and 36.15% month-over-month decline, and the brand’s average price fell 31.22% year over year to $25.28, indicating mix and pricing shifts are redistributing volume toward lower-priced formats while Flower remains the anchor. With Flower ranked 14 in Ohio, the pattern implies over-reliance on a weakening core and an emerging but volatile secondary focus in Pre-Roll and Concentrates.

The combination of a 1.46% brand-level year-over-year sales lift alongside a 31.22% year-over-year price drop and a 15.45% month-over-month decline in Flower signals that unit growth is being maintained by discounting and by channeling demand into Pre-Roll, which grew 14.28% month over month, while Vapor Pens erosion of 33.08% year over year constrains premium mix. Concentrates’ 4,478.03% year-over-year growth from a low base and a 13.62% month-over-month pullback point to experimentation rather than stable adoption, whereas Edible’s 74.24% year-over-year contraction and 36.15% month-over-month drop indicate deliberate deprioritization. Given a 14th-place Flower rank in Ohio and a category mix still three-quarters Flower, the implication is a near-term need to defend Flower while scaling Pre-Roll as the volume hedge and using Concentrates selectively to test premium headroom without further diluting average price.

Competitive Landscape

King City Gardens sits at rank #14 in OH Flower in May 2026, down 5 positions from #9 year over year, and off 8 spots from #6 in February 2026, while still far from its peak at #2 in June 2024; meanwhile, Riviera Creek holds #1 after rising from #2 year over year as its sales fell 10.1%, and Klutch Cannabis moved up to #3 from #16 on 161.1% sales growth. With category leaders shifting upward despite mixed sales trends and King City Gardens declining from #9 to #14, the trajectory implies share is being ceded to faster-climbing rivals and that regaining former peak position likely requires a reset in assortment, pricing, or distribution to counter competitors’ rank momentum.

Notable Products

Blueberry Muffin (2.83g) set the month’s tone with a -18.3% month-over-month drop while holding rank 8, signaling demand softness lower in the top 10 and creating mix pressure alongside a stable top tier. In contrast, Frosted Enigma (2.83g) rose +4.8% MoM at rank 1, widening its lead over rank 2 and concentrating share at the top as four of the top ten are Smalls SKUs that cluster between ranks 2 and 9, indicating value-size formats are anchoring volume. With Apples and Bananas Smalls (3.5g) at rank 2 and Dulce De Uva (3.5g) at rank 4, the upper ranks lean toward Flower staples while mid-pack volatility grows, implying King City Gardens is tilting the lineup toward dependable flagship Flower while using Smalls to defend price-sensitive segments.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.