Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Level is stocked at 910 licensed dispensaries across California, New York, and 7 other states, 588 of them in California, with the deepest coverage in Los Angeles, San Diego, Sacramento, San Francisco, and Santa Rosa. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

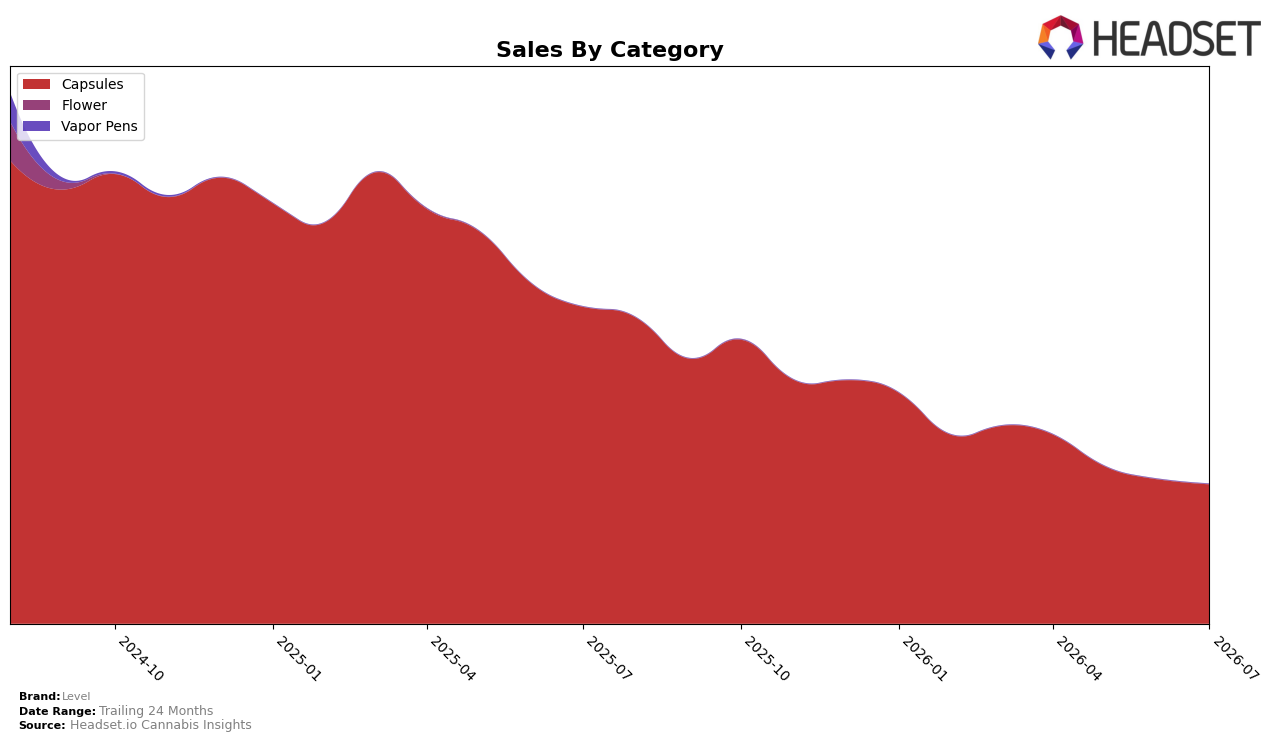

Capsules accounted for 99.92% share in July 2026 with a year-over-year change of -56.06% and month-over-month change of -3.40%, while Flower held 0.08% share with a year-over-year change of 3,181.96% and month-over-month change of 45.26%. The average price fell 7.81% year over year to $16.95, aligning with a 56.03% brand sales contraction year over year and a 72.80% decline over 24 months. With Capsules concentrated at 99.92% share and rank 2 in Capsules in Nevada, the pattern implies a highly specialized portfolio where small but rapid gains in Flower do not yet offset the sustained volume erosion in the core format.

The 45.26% month-over-month increase and 3,181.96% year-over-year surge in Flower from a 0.08% base, alongside a -3.40% month-over-month dip and -56.06% year-over-year decline in Capsules, indicates portfolio fragility if Capsules continue to contract. Given average pricing down 7.81% year over year and Capsules at a 99.92% share, maintaining rank 2 in Capsules in Nevada while diversifying into a higher-priced Flower line at $29.52 suggests Level is trading some price for volume in its core and probing premium positioning at the margin; the implication is a need to rebalance mix to stabilize share without overreliance on a single format.

Competitive Landscape

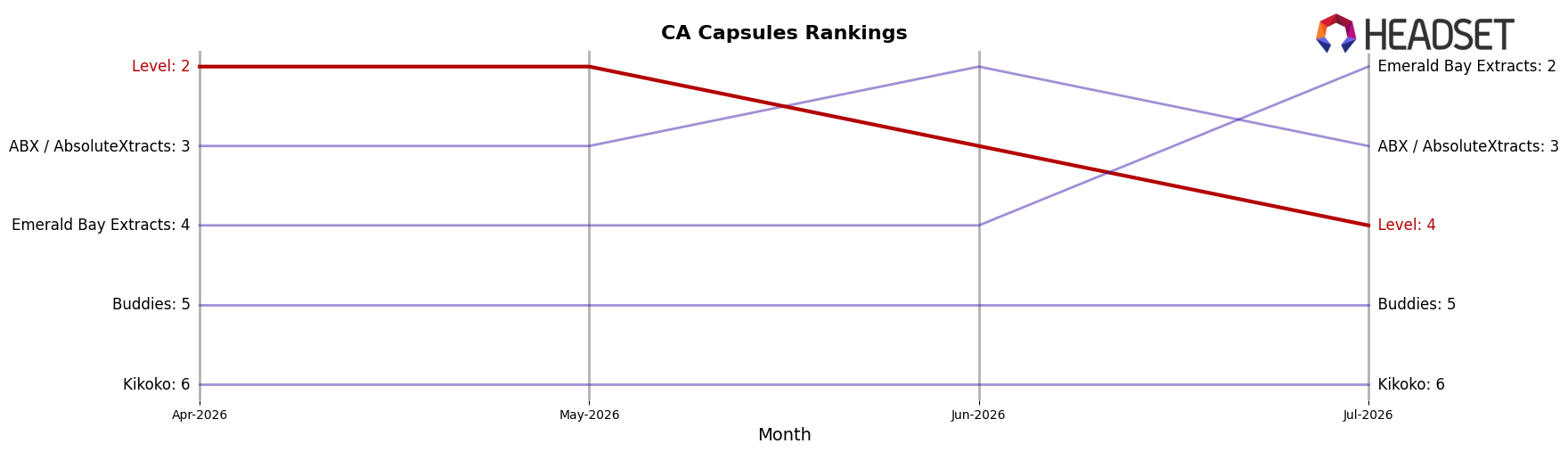

Level sits at rank #4 in California Capsules in July 2026, down 3 positions from #1 year over year, and off 2 places from April 2026’s #2, while having previously peaked at #1 in January 2026; in contrast, Breez holds #1 despite a -32.37% year-over-year sales change and ABX / AbsoluteXtracts is #3 with a -6.98% year-over-year decline, whereas Emerald Bay Extracts climbed to #2 from #5 year over year on a +40.61% lift; this pattern implies Level’s rank trajectory has shifted from a January 2026 leadership position toward a mid-pack posture as competitors with either recovering or contracting sales dynamics re-ordered the top three.

Notable Products

Hashtab 100 - Indica Tablet (100mg) delivered the standout move in July 2026 with a 56.5% month-over-month gain into rank 4, while Protab+ - Lights Out Tablets 10-Pack (50mg CBN, 20mg CBG, 200mg Delta-9 THC, 50mg Delta-8 THC, 20mg THCA) fell 38.8% to rank 5. Protab - Sativa Profesional Strength Tablet (100mg) declined 15.5% to rank 2 as Protab - Indica Tablet (100mg) inched up 4.4% at rank 1, indicating a tilt toward indica-led formats over sativa in the month. With all ten top sellers in Capsules and four SKUs clustered in the top six despite mixed movements ranging from +56.5% to -38.8%, the concentration implies Level is consolidating around pill-based dosing rather than dispersing into other form factors.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.