Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Magic Number is stocked at 302 licensed dispensaries across Oregon, with the deepest coverage in Portland, Eugene, Salem, Bend, and Medford. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

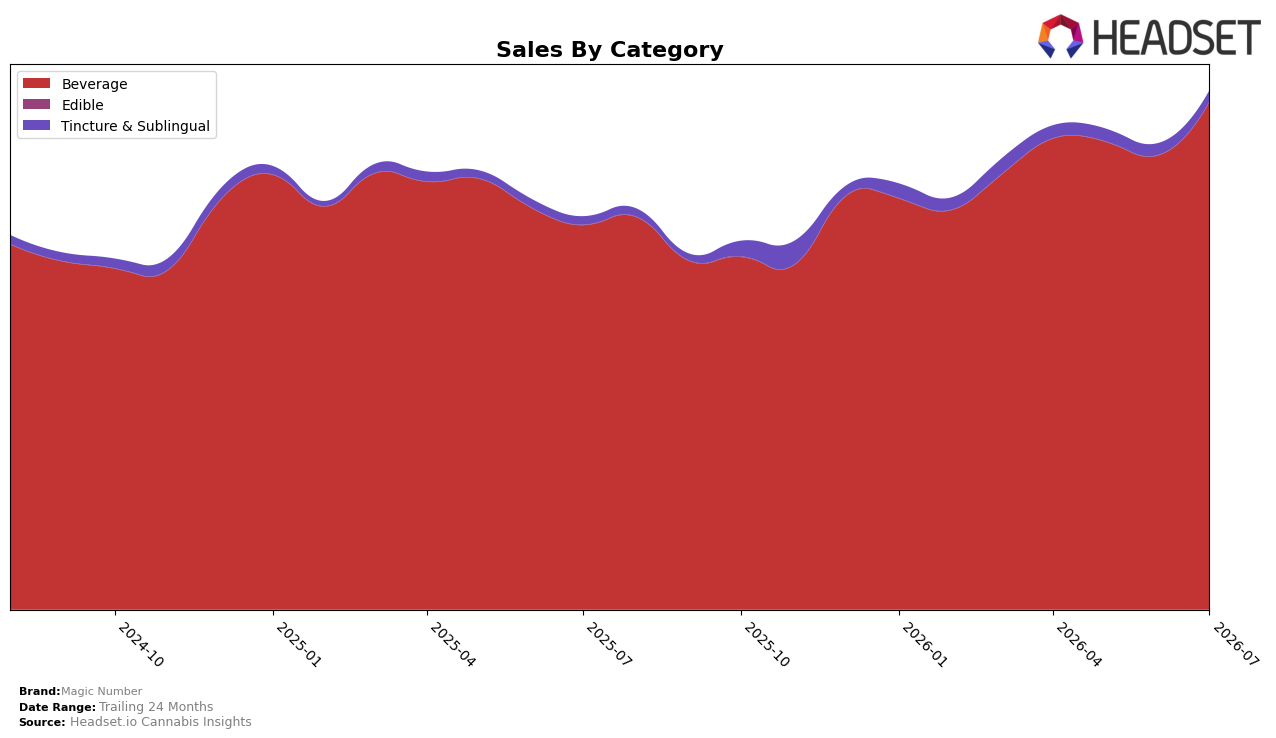

Magic Number concentrated 97.91% of sales in Beverage during July 2026, with Beverage up 32.07% year over year and 11.79% month over month, while Tincture & Sublingual held 2.09% share with 34.65% year-over-year growth but a 5.72% month-over-month decline. Average price in Beverage at $10.63 sat near the brand’s overall $10.76 average with a 0.63% year-over-year price lift, versus a higher $27.23 in Tincture & Sublingual, implying mix-driven revenue gains from volume rather than price. With Oregon Beverage rank at #1 and category share near 98%, the brand’s July 2026 profile implies a strategy anchored in Beverage where incremental month-over-month gains compound faster than smaller, more volatile extensions.

The widening MoM gap—Beverage up 11.79% versus Tincture & Sublingual down 5.72%—alongside a 32.12% brand-level year-over-year increase and a 32.07% Beverage year-over-year lift indicates that July 2026 growth is predominantly category-core and not reliant on premium-priced niches. Holding a #1 Beverage rank in Oregon while running a 97.91% Beverage mix implies defensibility via scale and repeat purchasing, but also concentration risk if Beverage growth decelerates; the pattern points to prioritizing depth in core Beverage where momentum is evident and selectively pruning or repositioning Tincture & Sublingual to stabilize its negative month-over-month swing.

Competitive Landscape

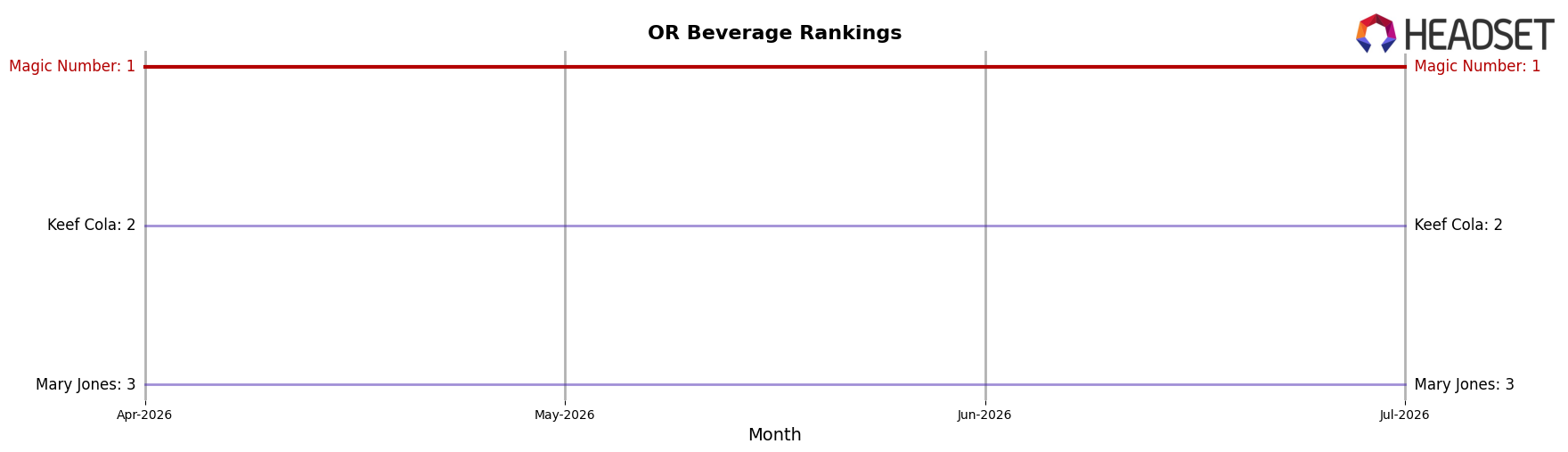

Magic Number holds #1 in OR Beverage in July 2026 with a 0-place YoY rank change and a 0-place change versus April 2026, while maintaining a 0-place shift over the last three months; in contrast, Keef Cola remains #2 with a -31.6% YoY sales decline and no rank movement, and Mary Jones sits at #3 with a -0.1% YoY sales change and no rank movement. Further back, Mule Extracts holds #4 with +1.8% YoY sales growth as Crown B Alchemy is #5 with a -33.0% YoY sales decline, collectively indicating the top five has been static in rank positions while competitors diverge on sales velocity. The pattern implies that Magic Number’s flat YoY rank at #1 amid mixed competitor sales trends points to entrenchment at the top driven more by peers’ stagnation or contraction than by disruptive rank shifts.

Notable Products

Classic Cola Live Rosin Soda (100mg THC, 355ml) posted the standout move in July 2026 with a +50.5% month-over-month surge to rank 6, while Artisan Series -Old Fashioned Lemonade (100mg THC, 237ml, 8oz) grew +37.7% to hold rank 1. Sasparilla Soda (25mg THC, 12oz) climbed +46.0% at rank 3, whereas Blue Raspberry Live Resin Soda (100mg THC, 355ml) dipped -3.8% to rank 5. With all of the top ten sitting in Beverage and multiple colas and citrus profiles clustered in the top six, the mix signals a tilt toward classic soda formats and bright citrus that can be scaled further without diluting the brand’s beverage-led positioning.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.