Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

National Cannabis Co. is stocked at 87 licensed dispensaries across Oregon, with the deepest coverage in Eugene, Portland, Salem, Bend, and Medford. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

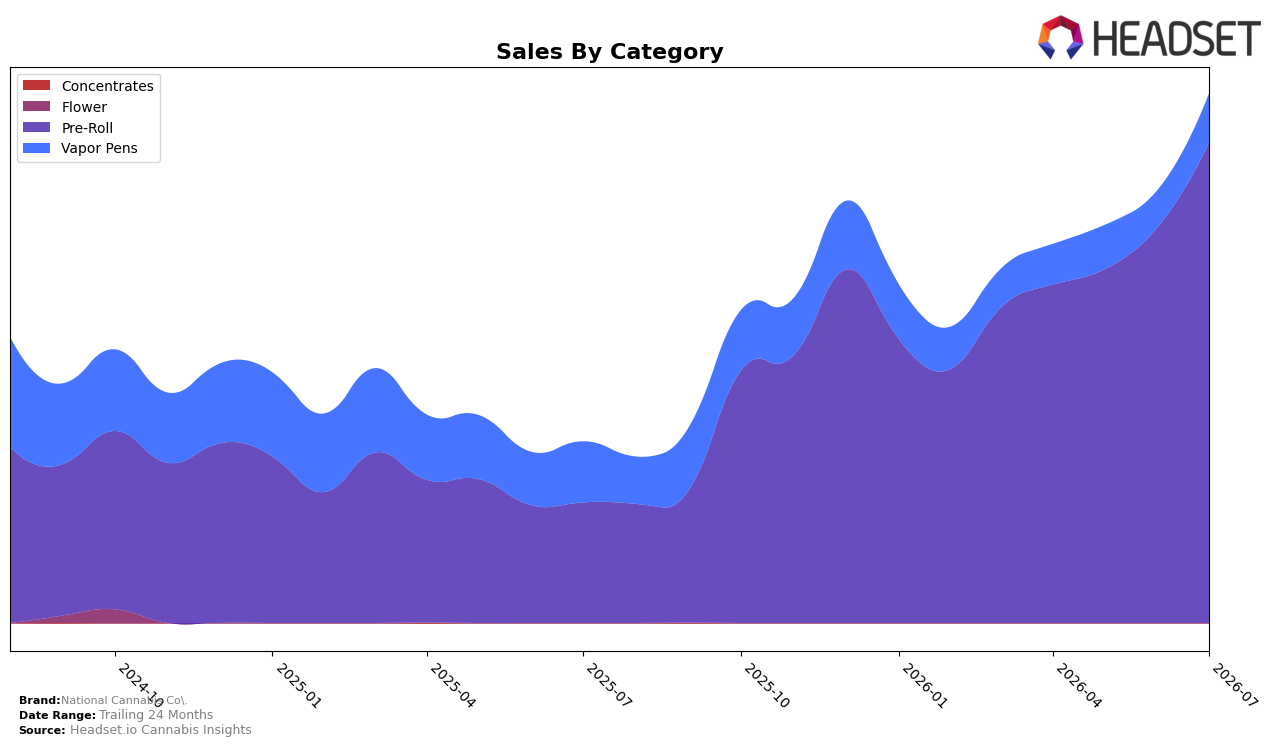

Pre-Roll expanded to 90.76% share in July 2026 with 299.84% year-over-year growth and 21.39% month-over-month, while Vapor Pens held 9.24% share with -19.53% year-over-year and 32.27% month-over-month. Overall brand sales grew 192.56% year-over-year alongside an average price decline of 8.70%, and within Pre-Roll the average price sat at $5.21 versus $17.43 in Vapor Pens. The mix now leans decisively into value-priced Pre-Rolls, implying National Cannabis Co. is consolidating around high-velocity, low-price units to compound volume faster than price compression erodes revenue.

With a Pre-Roll market rank of 17 in Oregon and Pre-Rolls at 90.76% mix, the 21.39% month-over-month lift in that category outpaced the brand’s 32.27% month-over-month rebound in Vapor Pens in absolute contribution, while the -19.53% year-over-year in Vapor Pens limits premium diversification. The brand’s 78.74% two-year growth paired with an 8.70% average price decline indicates reliance on unit expansion over pricing power, and July 2026’s category posture concentrates competitive exposure in a single format. The pattern implies National Cannabis Co. should treat Vapor Pens as an optional upsell while defending July 2026’s Pre-Roll rank position through sub-$6 price-points and incremental assortment depth, using the dominant share to anchor distribution while selectively testing higher-margin pen SKUs.

Competitive Landscape

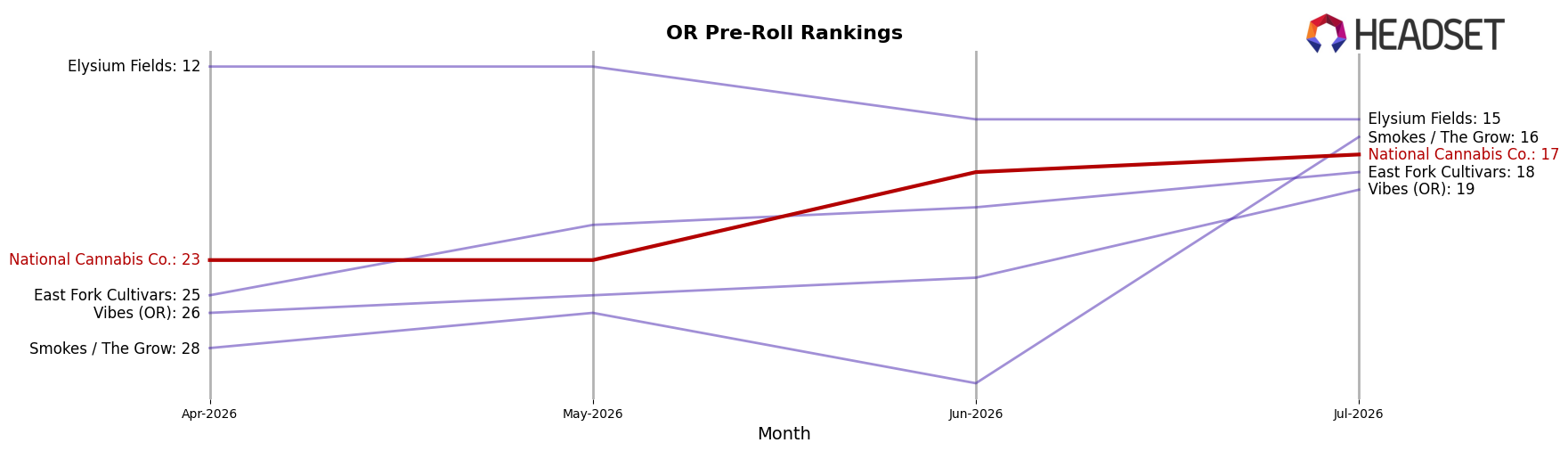

National Cannabis Co. is ranked #17 in OR Pre-Roll in July 2026, improving 37 positions from #54 year over year, and rising 6 spots from #23 since April 2026; this new peak at #17 marks a 0-position change from its best historical rank while the category’s top end tightened as STiCKS held #1 with 148.4% YoY sales growth and Kaprikorn advanced from #6 to #2 with 144.3% YoY growth. Against that backdrop, Portland Heights slid from #3 to #4 with a -23.1% YoY sales change while Hellavated eased from #2 to #3 despite positive 5.5% YoY growth, indicating that National Cannabis Co.’s rank ascent is tied less to broad market lift and more to share capture from mid-tier incumbents as volatility at the top compresses the ladder.

Notable Products

Oregon Apple Infused Pre-Roll (1g) posted the standout move with a 140.6% month-over-month surge to rank 4, while Blood Orange Gelato Infused Pre-Roll (1g) slipped 9.4% at rank 9, signaling a widening gap between fast-risers and laggards. Guava Botanical Infused Pre-Roll (1g) held rank 1 with a modest 3.3% lift as CBD/THC 1:1 Raspberry Skywalker Infused Pre-Roll (1g) advanced 22.3% to rank 2, indicating leadership is still anchored by steady performers despite sharp mid-pack gains. With all top ten items concentrated in Pre-Roll and multiple 1:1 SKUs logging double-digit growth (22.3% and 23.8%) alongside a single downturn of -9.4%, July 2026 points to an infused and ratio-led lineup pulling volume rather than breadth by category. The pattern implies National Cannabis Co. is consolidating around infused Pre-Rolls and 1:1 variants to scale velocity, prioritizing depth in a narrow form factor over diversification.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.