Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

No.9 Sunflower Collection is stocked at 82 licensed dispensaries across Massachusetts, with the deepest coverage in Fall River, Brockton, Franklin, Northampton, and Worcester. Search by ZIP code or city below to find the closest one.

Market Insights Snapshot

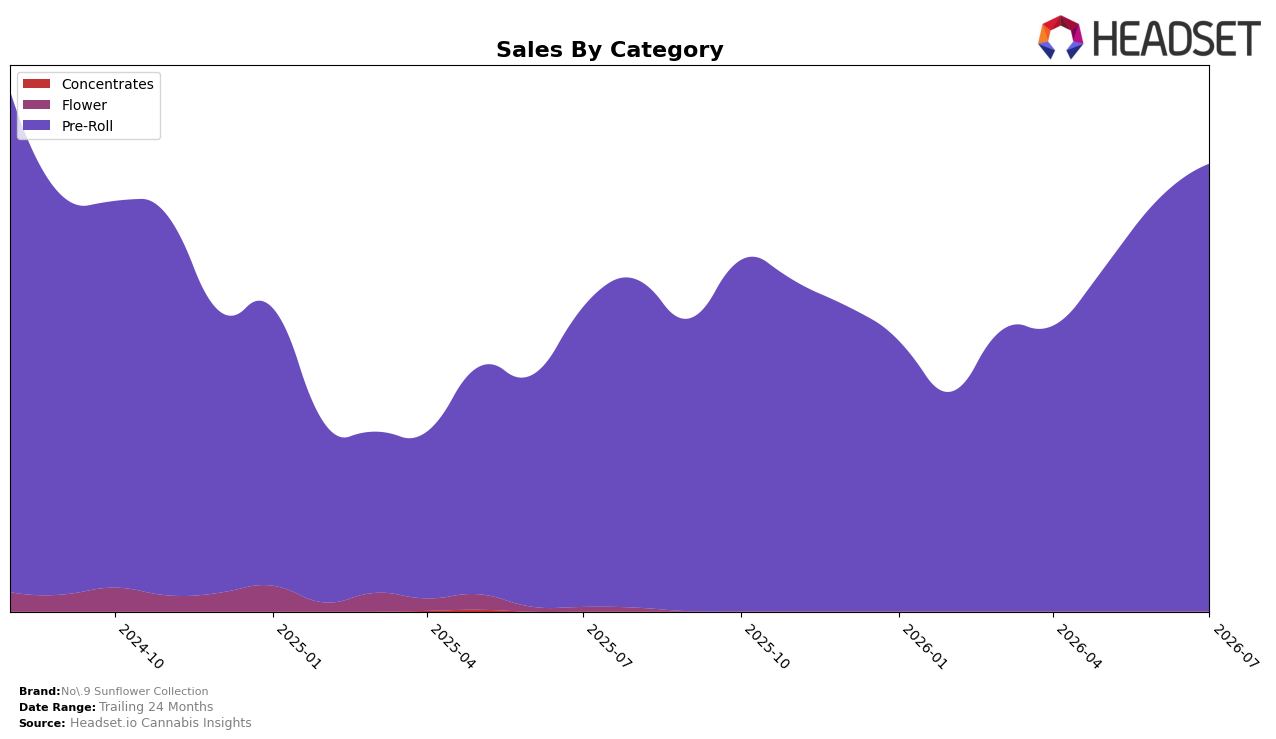

No.9 Sunflower Collection operated as a single-category brand in July 2026, with Pre-Roll accounting for 100.0% of sales and posting 49.25% year-over-year growth alongside an 8.76% month-over-month gain; this compares with the brand-level year-over-year growth of 47.15% and a 24-month change of -2.96%. Within this mono-focus, average price rose 7.81% year-over-year to $26.32 while unit growth necessarily outpaced price, implying that July 2026 momentum was volume-led rather than price-driven despite the price lift.

These shifts position No.9 Sunflower Collection as a category specialist whose performance is tied tightly to Pre-Roll demand, with July 2026 rank at 5 in Massachusetts Pre-Roll indicating upper-tier placement while still leaving headroom for share capture. The combination of an 8.76% month-over-month sales increase and a 7.81% year-over-year price rise signals elasticity room in Pre-Roll and suggests that incremental distribution or pack architecture can extend volume without eroding rank, implying that maintaining focus in Pre-Roll is currently more accretive than diversifying into adjacent formats.

Competitive Landscape

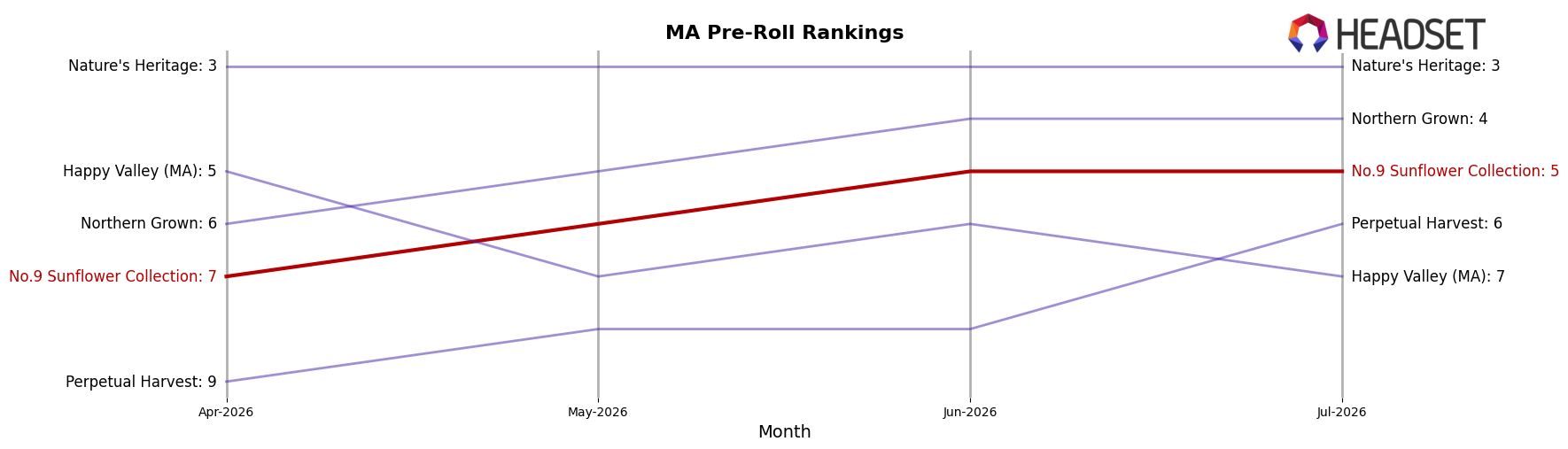

No.9 Sunflower Collection sits at rank #5 in July 2026, unchanged YoY from #5, after improving two spots from #7 in April 2026; meanwhile its historical peak was #2 in August 2024, marking a three-position gap from today that frames the current plateau. Competitors moved more decisively: Jeeter held #1 YoY while growing sales by 44.2%, and Cali-Blaze jumped from #16 YoY to #2 with a 241.1% sales increase, indicating that No.9 Sunflower Collection’s flat YoY rank at #5 alongside a three-month climb from #7 to #5 signals stability but also share pressure from faster risers.

Notable Products

Doob Cube Mini - Variety Pre-Roll 20-Pack (7g) posted the headline move with a +54.96% month-over-month jump to rank 1, while Blueberry Cupcake Pre-Roll (1g) slid -16.83% at rank 8 and Hella Jelly Pre-Roll (1g) fell -17.65% at rank 10. Doob Cube Micro - Variety Pre-Roll 14-Pack (7g) dropped -11.22% into rank 2 as Doob Cube Micro Magnum - Variety Pre-Roll 28-Pack (14g) advanced +40.87% at rank 6, tilting share toward larger-count packs. With all ten top SKUs in the Pre-Roll category and multiple Doob Cube formats occupying ranks 1-3, the mix indicates a pivot toward value-driven multi-packs over single grams, concentrating demand in higher-count offerings.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.