Mar-2025

Sales

Trend

6-Month

Product Count

SKUs

Overview

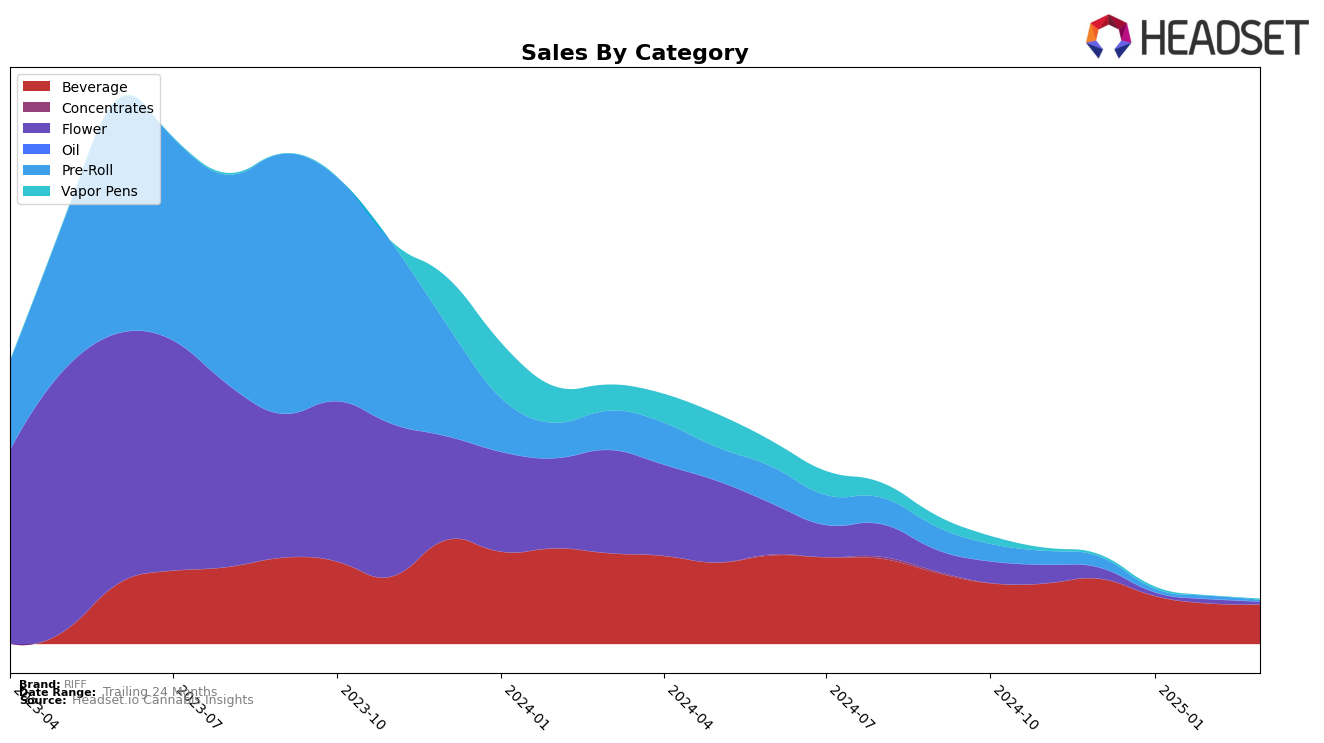

Market Insights Snapshot

In the Canadian market, RIFF shows a consistent presence in the Beverage category across multiple provinces, although its ranking varies. In Alberta, RIFF maintained a stable ranking at 13th place from December 2024 to March 2025, despite a noticeable decline in sales over this period. This suggests that while the brand holds a steady position, it faces challenges in increasing its market share or sales volume. Similarly, in Ontario, RIFF's rank remained unchanged at 14th, highlighting a parallel trend of stable ranking but declining sales. The brand's performance in Saskatchewan is noteworthy; it achieved a 6th place ranking in December 2024 but did not appear in the top 30 in subsequent months, indicating a significant drop in its competitive standing.

The absence of RIFF in the top 30 rankings in Saskatchewan for January, February, and March 2025 may signal either a strategic withdrawal or a significant shift in consumer preferences. This lack of presence could be perceived as a challenge for RIFF to regain momentum in the province. While the brand's steady rankings in Alberta and Ontario suggest a certain level of consumer loyalty or brand recognition, the consistent decline in sales figures across these regions could imply increasing competition or changing market dynamics that RIFF needs to address. These trends highlight the importance for RIFF to adapt its strategies to maintain and improve its market position in the growing and competitive cannabis beverage market.

Competitive Landscape

In the competitive landscape of the beverage category in Ontario, RIFF has maintained a consistent presence, albeit with some challenges in climbing the ranks. From December 2024 to March 2025, RIFF's rank hovered around the 14th position, indicating a stable yet stagnant performance. In comparison, Keef Cola started and ended this period at the 12th position, suggesting a stronger foothold in the market. Meanwhile, Astro Lab showed improvement, rising from 16th in December to 13th by March, surpassing RIFF in the process. Palmetto also demonstrated upward momentum, climbing from 20th to 15th, while Señorita remained relatively stable around the 18th position. This competitive analysis highlights the need for RIFF to innovate or enhance its market strategies to improve its rank and sales, as competitors like Astro Lab and Palmetto are gaining ground.

Notable Products

In March 2025, Wild Raspberry Lemonade (10mg THC, 355ml) continued to dominate the sales chart for RIFF, maintaining its first-place ranking since December 2024, with a sales figure of 4361. Blue Raspberry Ice Lemonade (10mg THC, 355ml) also held steady in second place throughout the same period. The Boost- THC/CBG 1:1 Tropical Burst Carbonated Drink (10mg THC, 10mg CBG 355ml) remained consistently in third place, showcasing stable demand. Boost- THC/CBG 1:1 Vanilla Frost Carbonated Drink (10mg THC, 10mg CBG) experienced no change in its fourth-place ranking since January 2025. Subway Scientist Pre-Roll (1g) maintained its fifth-place position from January to March 2025, indicating a consistent performance in its category.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.