Mar-2025

Sales

Trend

6-Month

Product Count

SKUs

Overview

Market Insights Snapshot

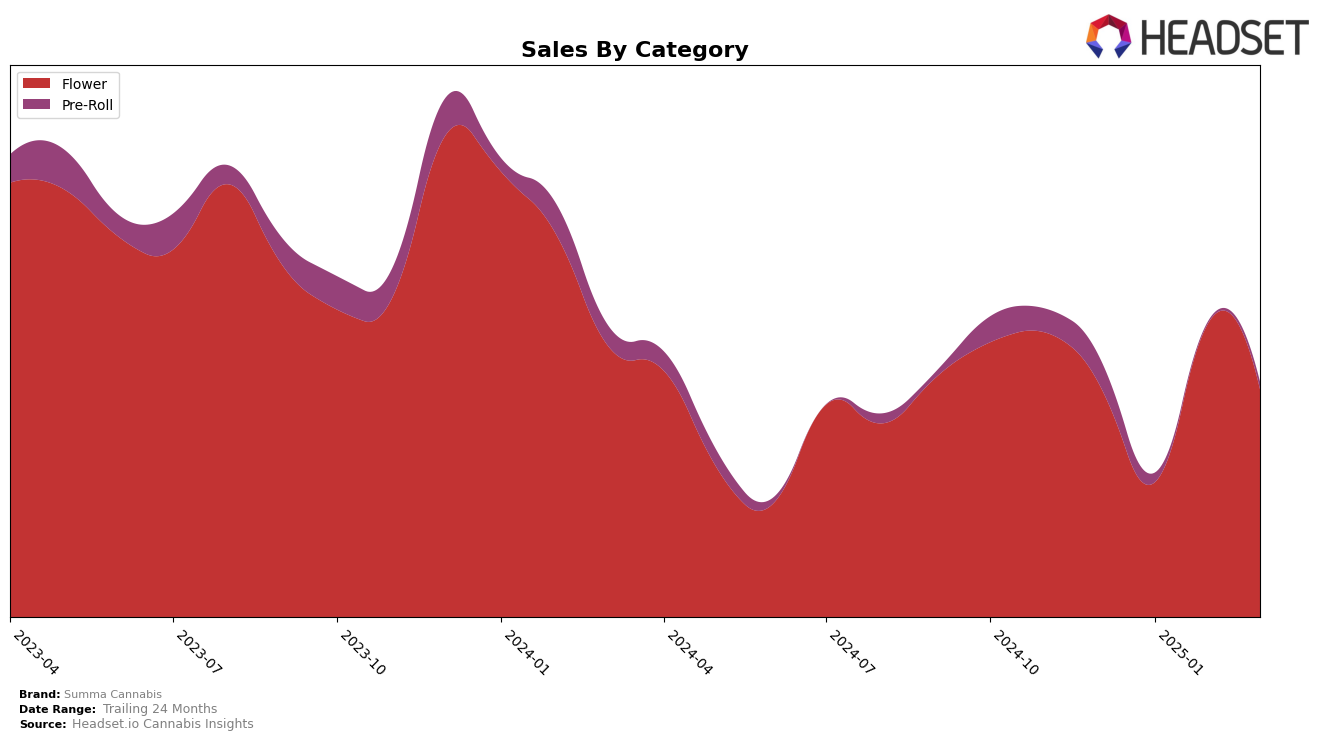

Summa Cannabis has demonstrated notable performance in the Nevada market, particularly within the Flower category. Starting from December 2024, the brand ranked 13th, and despite a brief dip to 27th in January 2025, it quickly rebounded to 11th by February and maintained a strong position at 12th in March. This fluctuation in rankings suggests a dynamic market presence and adaptability to consumer preferences. The sales figures reflect this upward trend, with February 2025 seeing a significant increase compared to the previous months, indicating a successful strategy in capturing market share during this period.

In contrast, the Pre-Roll category presents a different narrative for Summa Cannabis. The brand did not secure a spot within the top 30 in Nevada during the months of February and March 2025, highlighting a potential area for improvement. The rankings in December 2024 and January 2025 were 31st and 39th, respectively, before falling out of the top 30 entirely. This decline could suggest challenges in maintaining competitiveness or consumer interest within this specific product line. The downward trend in sales from December to February further underscores the need for strategic adjustments to regain traction in this category.

Competitive Landscape

In the Nevada Flower category, Summa Cannabis has experienced notable fluctuations in its market position over the past few months. Starting from December 2024, Summa Cannabis was ranked 13th, but it saw a dip in January 2025, dropping out of the top 20, before rebounding to 11th in February and settling at 12th in March. This volatility is contrasted by competitors like Good Green, which maintained a more stable trajectory, moving from 16th to 13th place over the same period. Find. also demonstrated resilience, consistently ranking within the top 10, except for a brief dip to 13th in February. Meanwhile, Kushberry Farms showed a strong performance in March, climbing to 11th place. The sales figures for Summa Cannabis reflect these ranking changes, with a significant drop in January but a recovery in February, indicating potential challenges in maintaining consistent market share amidst strong competition from brands like Dope Dope, which also showed dynamic movement, peaking at 13th in January.

Notable Products

In March 2025, Mule Fuel (3.5g) led the sales for Summa Cannabis, maintaining its top position from February with sales reaching 739 units. Wedding Cake (3.5g) emerged as the second-best performer, marking its first appearance in the rankings. Gary Payton (3.5g) secured the third position, showing strong sales momentum. Mother's Milk (14g) experienced a drop from second to fourth place compared to the previous month. Jealousy 58 (3.5g) rounded out the top five, entering the ranks for the first time in March.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.