Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

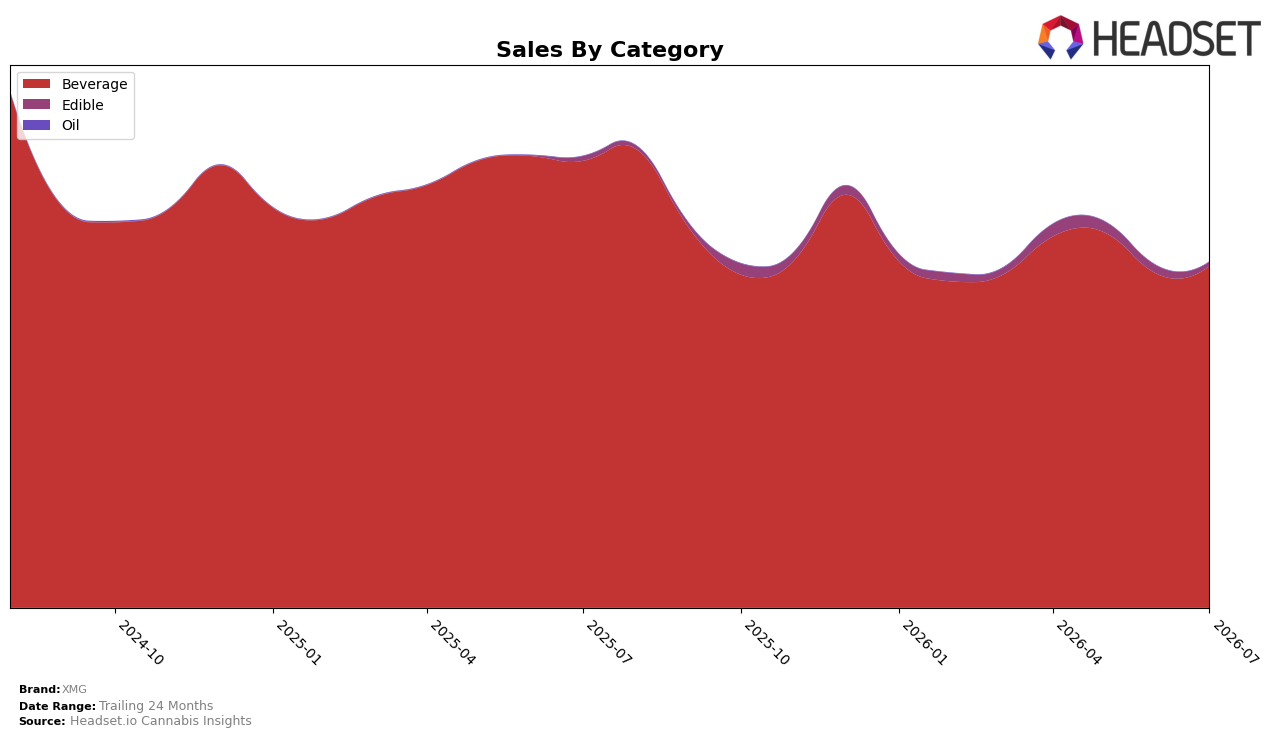

In July 2026, Beverage held 98.86% share with a month-over-month gain of 2.48% despite a year-over-year decline of 23.57%, while Edible sat at 1.14% share with a 48.58% MoM drop and a 9.62% YoY decline; the average brand price rose 14.92% YoY to $7.95. XMG’s overall sales fell 23.44% YoY as mix concentrated further into Beverage, but the category’s MoM uptick alongside Edible’s sharp MoM contraction indicates a consolidation around a single high-volume lane that is stabilizing sequentially. The pattern implies XMG is trading depth in Edible for incremental Beverage traction, accepting YoY contraction to defend its Beverage footprint where it holds Rank 1 in Beverage in Alberta.

With Beverage at 98.86% share and Edible at 1.14%, the brand’s exposure is highly concentrated, and the 2.48% MoM gain in Beverage against a 48.58% MoM decline in Edible signals a deliberate prioritization rather than broad category recovery. Coupled with a 14.92% YoY price increase and a 23.57% YoY Beverage decline, the mix suggests price-led revenue preservation in core Beverage while deprioritizing Edible, positioning XMG as a category specialist whose short-term volume risk is offset by leadership signaling via Rank 1 in Beverage in Alberta.

Competitive Landscape

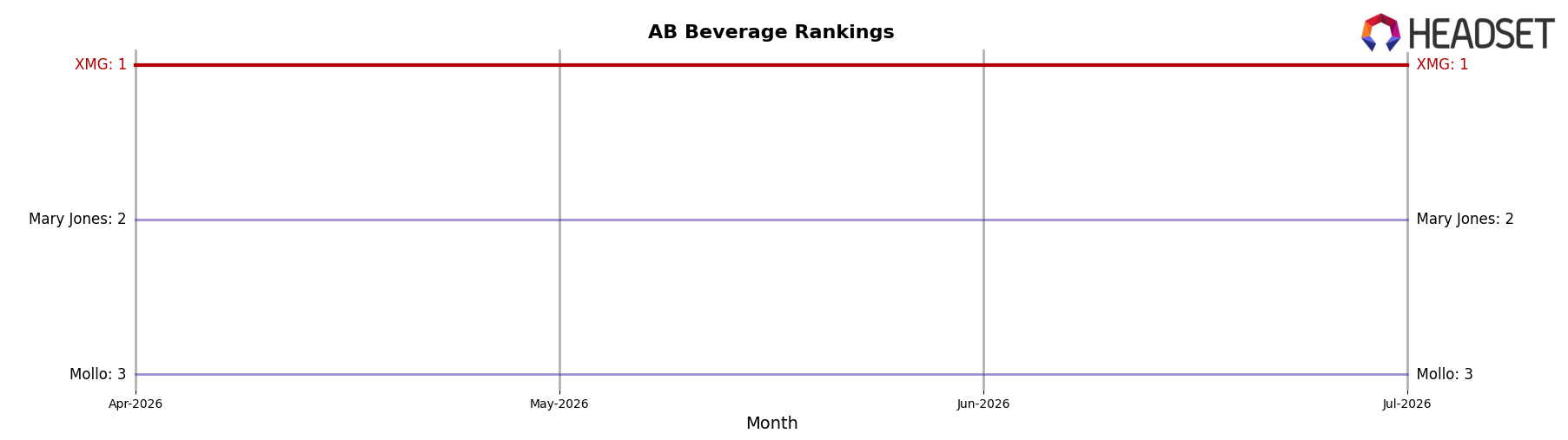

XMG holds #1 in AB Beverage in July 2026 with no year-over-year rank change from #1, while Mary Jones climbed from #6 to #2 on 198.2% YoY sales growth and Bubble Kush advanced from #7 to #4 with 92.4% YoY growth; by contrast, Sweet Justice slipped from #2 to #5 alongside a 27.6% YoY sales decline. XMG’s steady #1 in April 2026 through July 2026 versus Mollo holding flat at #3 with only 10.5% YoY growth indicates the gap is defended more by incumbency and retention than by outsized expansion, implying the top position is durable short term but exposed if the accelerating #2 continues compounding.

Notable Products

Plus - THC/CBG 1:1 Blackberry Lemonade Sparkling Beverage (10mg THC, 10mg CBG, 355ml) posted the steepest decline at -17.1% and slid to rank 9, while category leader Cherry Cola (10mg THC, 355ml) fell -31.3% yet held rank 1, indicating demand concentrated at the top despite a sharp pullback. Zero - Orange Soda (10mg THC, 355ml) rose +43.1% to rank 2, contrasting with Cream Soda (10mg THC, 355ml) at -7.8% in rank 3, and eight of the top ten are Beverage SKUs in the core soda formats, with just one raw-dollar anchor at $122,132 for the lead item. Across the portfolio, modest single-digit gains on three mid-pack items (+3.9% to +4.3% at ranks 4, 6, and 7) coexist with a near-flat Zero - Cream Soda at +0.18% in rank 8, pointing to mix stability beneath the headline swings. The pattern implies XMG is pivoting toward zero-sugar and functional 1:1 variants to defend share while premium fruit-led 1:1 flavors face volatility, suggesting assortment pruning and sustained support for rank 1–2 tentpoles.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.