Mar-2025

Sales

Trend

6-Month

Product Count

SKUs

Overview

Market Insights Snapshot

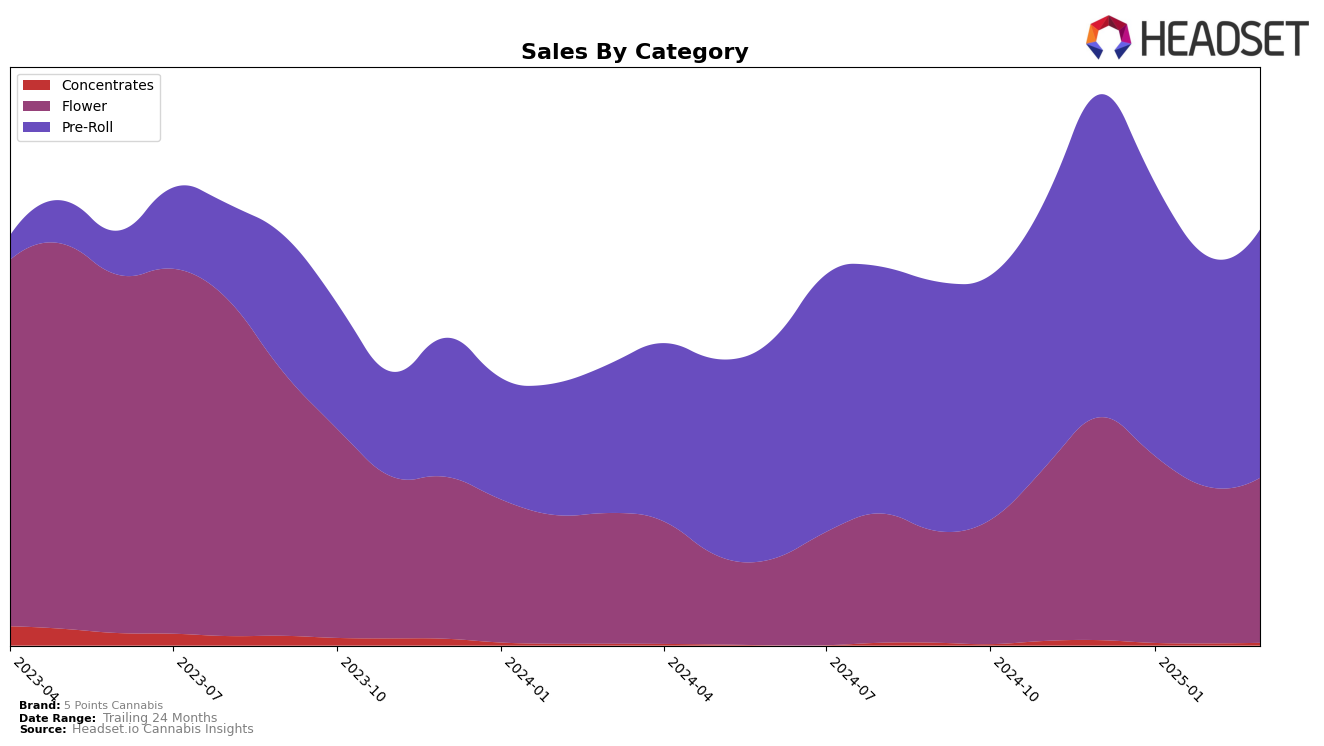

In the British Columbia market, 5 Points Cannabis has shown a consistent upward trajectory in the Flower category, climbing from a rank of 68 in December 2024 to 55 by March 2025. This improvement is supported by a steady increase in sales, culminating in a notable rise to 76,091 CAD in March. In contrast, the Ontario market presents a mixed performance. While the brand saw a dip in the Flower category rankings, moving from 39 in January to 50 in February before slightly recovering to 48 in March, the Pre-Roll category maintained a more stable position, remaining in the top 30 throughout this period. However, the absence of a top 30 ranking in the Concentrates category since December 2024 suggests potential challenges or a strategic shift away from this segment.

In Saskatchewan, 5 Points Cannabis experienced fluctuations in the Pre-Roll category, where it dropped from a rank of 19 in December 2024 to 38 by March 2025. This decline is mirrored by a significant reduction in sales, indicating potential market pressures or increased competition. Meanwhile, the brand's presence in the Flower category in Saskatchewan is less prominent, with rankings only available for December and January, suggesting they did not maintain a top 30 position in subsequent months. These variations across different provinces and categories highlight the diverse market dynamics 5 Points Cannabis faces, with some areas showing promise and others indicating challenges that may require strategic adjustments.

Competitive Landscape

In the competitive landscape of the Ontario pre-roll category, 5 Points Cannabis has demonstrated a steady performance, maintaining its rank at 27th place from February to March 2025, after a slight dip from 26th in January. This consistency in rank suggests a stable market presence amidst fluctuating sales figures. Notably, 1964 Supply Co has shown an upward trend, improving its rank from 37th in December 2024 to 29th in March 2025, indicating a potential threat if this trajectory continues. Meanwhile, CountrySide Cannabis experienced a decline, dropping from 17th in December to 26th in March, which could present an opportunity for 5 Points Cannabis to capture market share. Additionally, Buddy Blooms and Tribal have shown variable rankings, with Buddy Blooms slipping slightly from 22nd in January to 25th in March and Tribal experiencing a similar dip. These shifts highlight a dynamic market environment where 5 Points Cannabis can leverage its consistent ranking to strategize for growth and increased sales.

Notable Products

For March 2025, the top-performing product for 5 Points Cannabis remains the Zsweet Pre-Roll 10-Pack (3g), holding its consistent first-place ranking with sales of 5711 units. The Blueberry Yum Yum Pre-Roll 10-Pack (3g) continues to secure the second position, although its sales have decreased compared to previous months. The Strawberry Kush Pre-Roll 10-Pack (3g) maintains its third-place ranking, showing a slight increase in sales from February. The Strawberry Kush (3.5g) has consistently held the fourth position since January 2025, with a gradual decline in sales. The Permanent Marker (3.5g) has remained in fifth place since its entry into the rankings in February 2025, showing a modest increase in sales.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.