Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

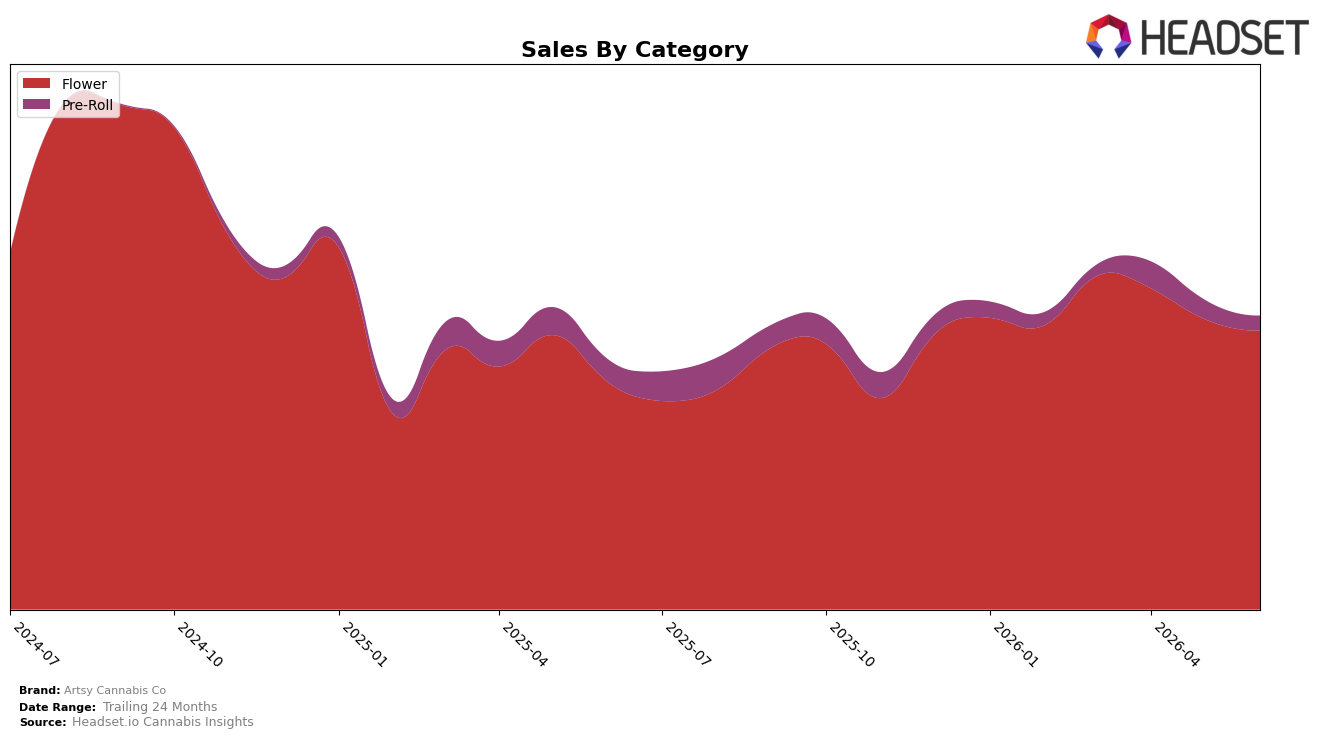

In June 2026, Artsy Cannabis Co concentrated 94.89% of sales in Flower while Pre-Roll accounted for 5.11%, with Flower up 22.71% year over year but down 3.97% month over month, and Pre-Roll down 34.06% year over year and 22.42% month over month. Despite a 17.53% brand-level year-over-year sales increase and a 4.91% decline in average price, the category mix leaned further into higher-priced Flower at an average of $36.21 versus $7.23 for Pre-Roll, implying volume gains in Flower offset steep declines in Pre-Roll. The brand held rank 13 in Flower in Colorado, and the combination of a top-heavy mix and negative month-over-month shifts suggests short-term volatility even as the year-over-year trajectory favors Flower-led growth.

The tilt toward Flower, paired with a 22.71% year-over-year lift and a 3.97% month-over-month pullback, positions Artsy Cannabis Co as a price-flexible Flower player rather than a balanced portfolio brand, especially with Pre-Roll shrinking 34.06% year over year and 22.42% month over month. With overall sales up 17.53% year over year but down 27.50% versus 24 months, and average prices down 4.91%, the path to improving the rank 13 slot in Colorado likely rests on sustaining Flower volume while stabilizing Pre-Roll contribution above the current 5.11% share; this pattern implies market share defense hinges on deepening Flower penetration while using selective price architecture to rebuild an entry-tier Pre-Roll on-ramp.

Competitive Landscape

Artsy Cannabis Co sits at rank #13 in CO Flower for June 2026, unchanged from #13 year over year, after slipping 1 position since March 2026 when it was #12; this flat YoY rank alongside a 7-position gap from its peak at #6 in June 2024 signals stalled competitive momentum as the category reorders. Meanwhile, Seed & Strain Cannabis Co. moved up from #2 to #1 with a 62.8% YoY sales increase, and Natty Rems surged from #28 to #5 on 221.0% YoY growth, while Good Chemistry Nurseries slid from #1 to #3 on a -2.8% YoY sales decline; compared to these shifts, Artsy Cannabis Co’s flat #13 YoY rank and 1-position quarter-over-quarter dip indicate it is losing relative share even without a large absolute decline, implying the brand must counter faster risers or risk drifting further from its historical #6 ceiling.

Notable Products

The steepest decline came from Fugazi Funk Pre-Roll (1g), down 51.5% month over month and sitting at rank 7, while Premium White Truffle (3.5g) fell 33.4% to rank 5, indicating demand is concentrating away from certain specialty SKUs. Pineapple Jarritos (3.5g) held rank 1 with a mild 2.7% dip, and Moon Suit (3.5g) occupied rank 3, as Flower captured 6 of the top 10 positions, pointing to a category-weighted mix favoring larger-pack and eighth formats. Brisket Pre-Roll (1g) at rank 2 alongside multiple Flower entries inside the top 5 suggests a barbell between a leading single pre-roll and flagship Flower that narrows variety risk. The pattern implies Artsy Cannabis Co is leaning into Flower-led volume while culling or repositioning underperforming pre-rolls, a shift that prioritizes stable rank retention over chasing volatile SKUs.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.