Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Bonanza Cannabis Company is stocked at 346 licensed dispensaries across Colorado, New Mexico, and 2 other states, 166 of them in Colorado, with the deepest coverage in Denver, Colorado Springs, Boulder, Durango, and Aurora. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

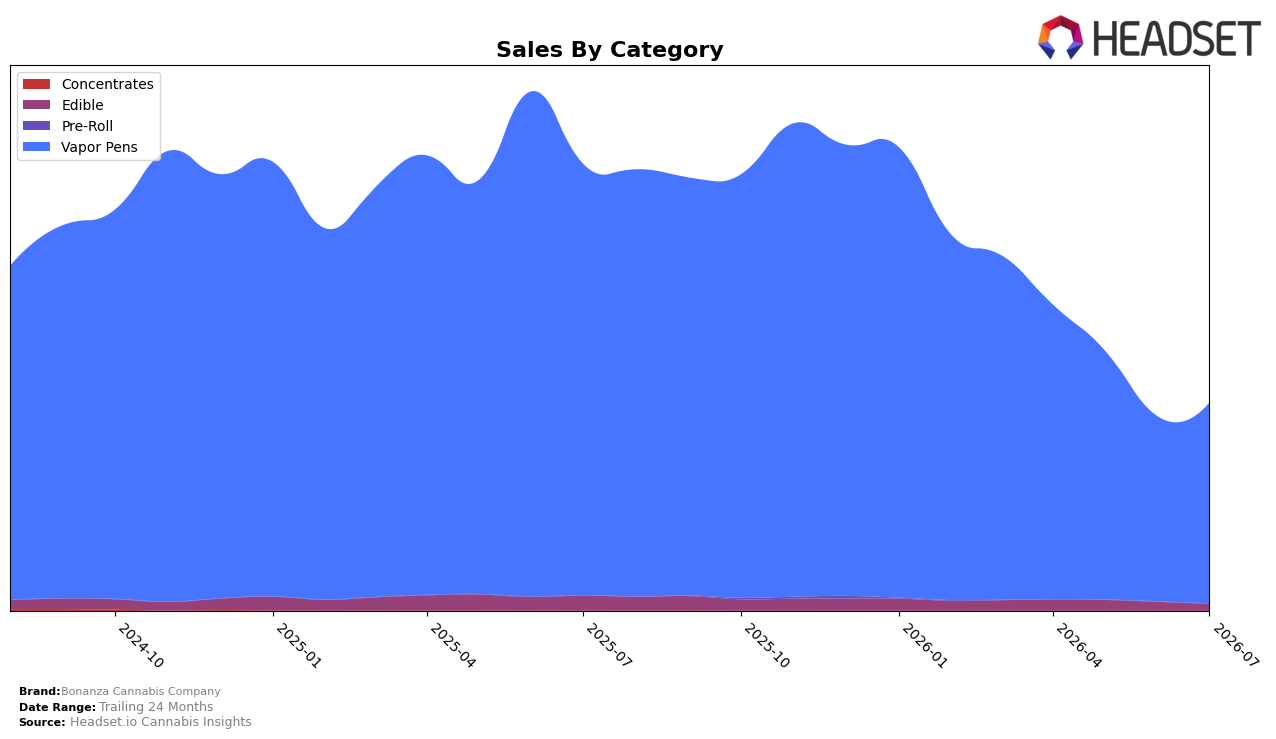

In July 2026, Bonanza Cannabis Company concentrated 96.86% of sales in Vapor Pens with an 8.70% month-over-month lift, while Edible held 3.14% with a -23.29% month-over-month decline; year-over-year, Vapor Pens fell -53.50% and Edible contracted -55.65%. The average price rose 5.99% year-over-year to $26.97, with Vapor Pens averaging $29.09, indicating mix and pricing shifts alongside a -53.57% brand sales year-over-year change. With Vapor Pens anchoring category mix and posting month-over-month recovery as Edible retreats, the pattern implies a deliberate narrowing toward a single-category focus that trades breadth for depth.

Bonanza Cannabis Company’s Vapor Pens concentration aligns with a rank of 6 in Vapor Pens in Colorado, suggesting sufficient scale to compete on velocity despite broad brand contraction and a 24-month sales change of -34.79%. The month-over-month gain in Vapor Pens alongside its 96.86% share, versus Edible’s double-digit month-over-month decline and 3.14% share, implies positioning oriented toward defending mid-tier rank via price-point management (average price up 5.99% year-over-year) and assortment pruning rather than multi-category expansion.

Competitive Landscape

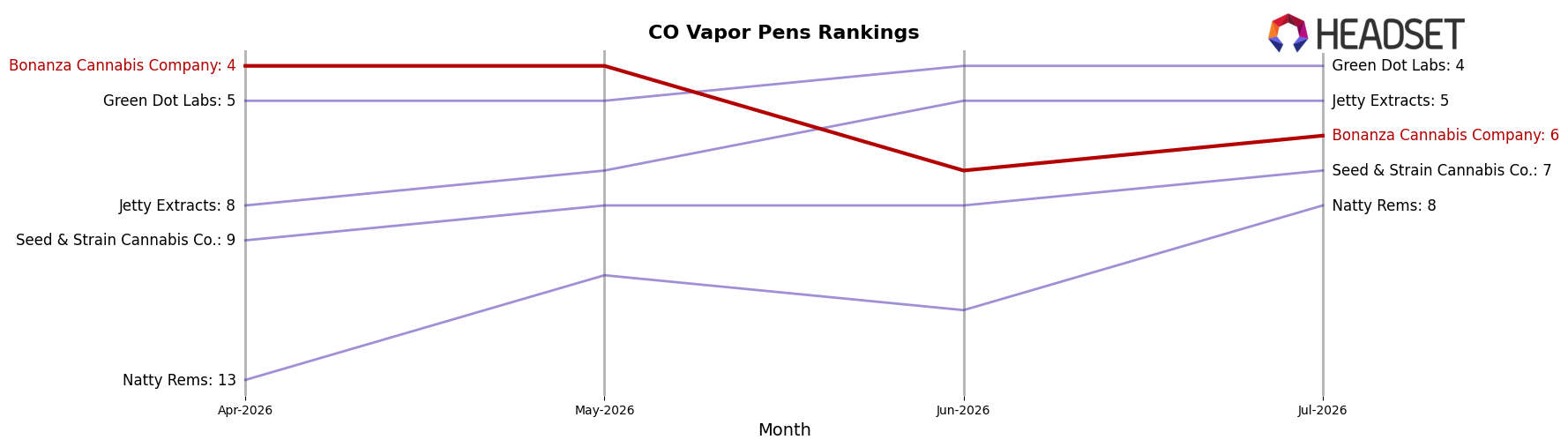

Bonanza Cannabis Company sits at rank #6 in Colorado Vapor Pens in July 2026, slipping 4 positions since April 2026 when it was #4, while its year-over-year rank moved from #2 to #6 for a 4-place decline. Competitors advanced over the same window: Spherex holds #1 with a 7.2% year-over-year sales increase and PAX is #2 with a 21.7% lift, whereas Jetty Extracts surged to #5 from #19 year over year amid 181.4% growth. Bonanza Cannabis Company peaked at #1 in February 2026 but is now 5 ranks below that peak and 2 below its April 2026 position, implying that recent share is consolidating with faster-growing rivals and that recovery would require reversing a two-quarter slide.

Notable Products

Blue Dream Distillate Cartridge (1g) posted the steepest movement in July 2026 with a -19.8% month-over-month decline and sat at rank 4, while Maui Wowie Distillate Cartridge (1g) rose 14.5% MoM to rank 2. Durban Dream Live Resin Cartridge (1g) held rank 1 with an estimated $67,474 in sales, and Tropicana Cherry Distillate Cartridge (1g) eased only -1.6% MoM at rank 8. With all top-10 slots concentrated in Vapor Pens and at least four of the ten being Distillate Cartridges, the mix points to a portfolio leaning into cartridge-led volume with selective strain momentum rather than broad-based gains.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.