Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Breez is stocked at 421 licensed dispensaries across California, Illinois, and Oklahoma, 332 of them in California, with the deepest coverage in Los Angeles, San Francisco, San Diego, North Hollywood, and Santa Rosa. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

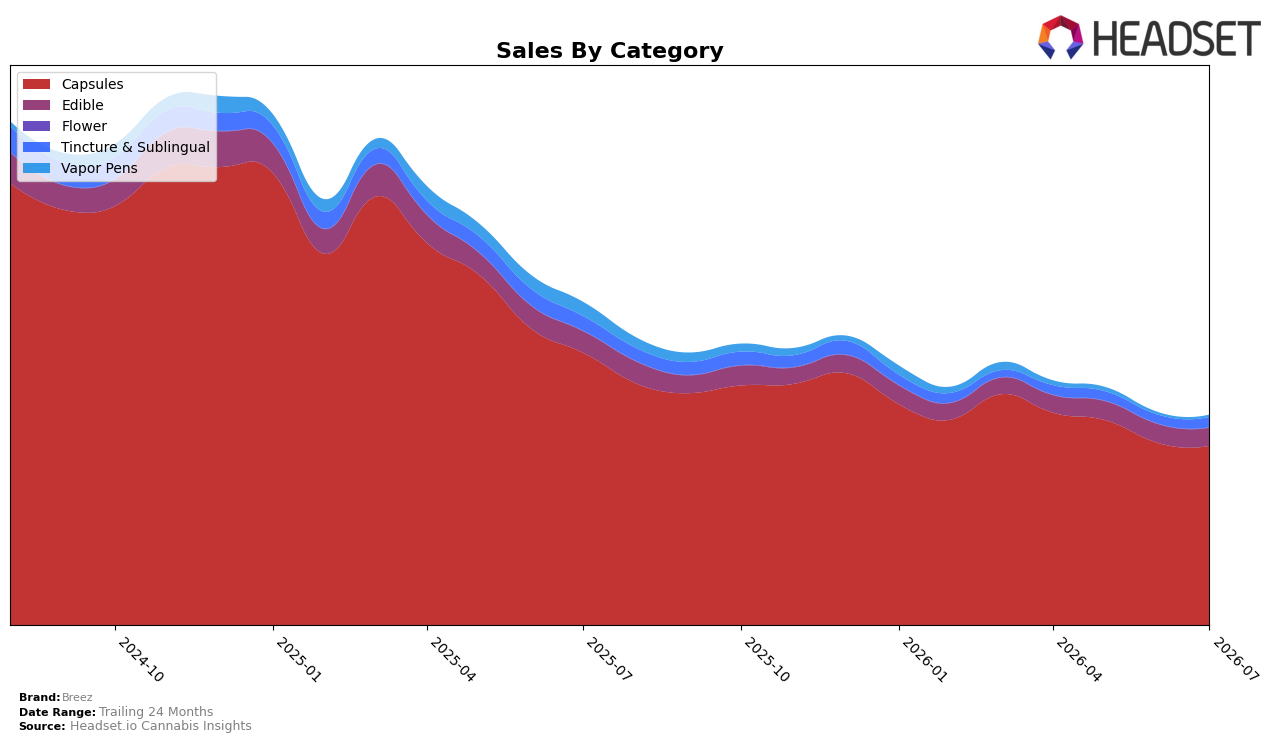

In July 2026, Breez remained highly concentrated in Capsules at 85.85% share while Edible held 8.50% and Tincture & Sublingual 4.72%, indicating a narrow mix as Capsules declined 34.22% year over year and 1.59% month over month. Edible contracted 16.45% YoY and 3.92% MoM, while Tincture & Sublingual dropped 30.88% YoY but grew 15.24% MoM, and Vapor Pens eroded 86.04% YoY and 12.97% MoM to a 0.92% share; combined with an 8.37% YoY rise in average price and a brand-level sales decline of 35.13% YoY, the data implies Breez is absorbing demand pressure in its core while testing recovery pockets in smaller formats.

The mix tilt toward Capsules at 85.85% alongside a category rank of 1 in California signals defensible placement, yet the 34.22% YoY contraction in that core and an overall 57.96% decline over 24 months suggest over-exposure risk if Capsules continue to compress. The 15.24% MoM lift in Tincture & Sublingual from a 4.72% base, paired with Edible’s 3.92% MoM pullback and Vapor Pens’ 12.97% MoM slide, points to a rebalancing path where modest share shifts into Tincture & Sublingual could stabilize mix without heavy price cuts; the thesis is that sustaining rank in Capsules while nudging 1–3 points of share toward faster-rebounding sublinguals can mitigate the 35.13% YoY brand decline without diluting positioning.

Competitive Landscape

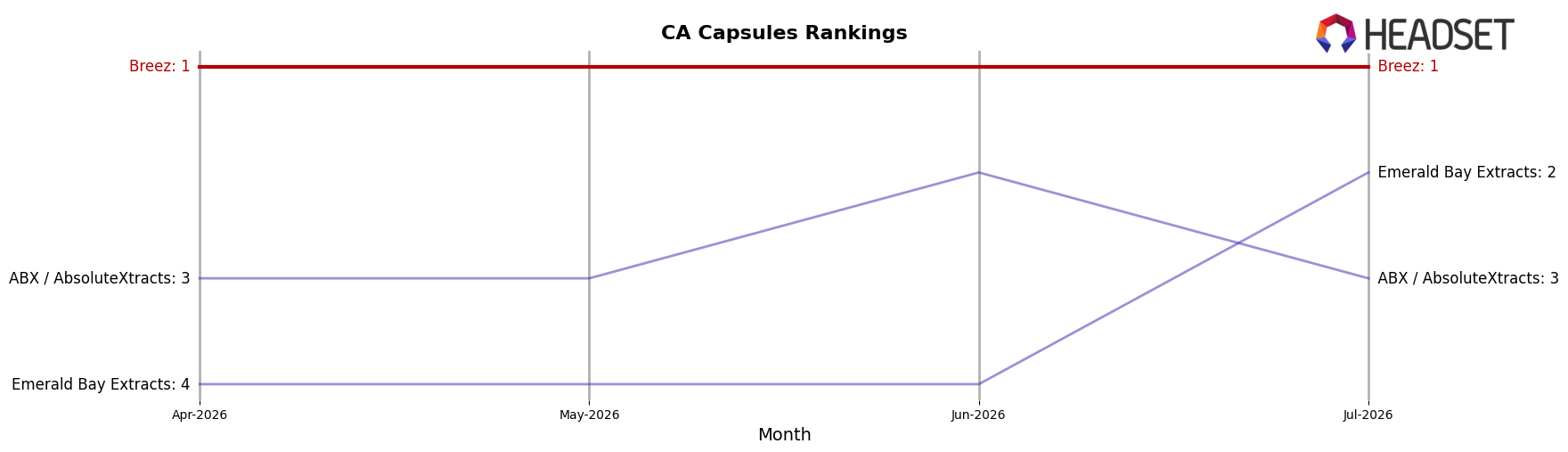

Breez ranks #1 in California Capsules in July 2026 after rising 1 position year over year from #2, and it held #1 three months ago as well, indicating stability at the peak while moving up from a lower YoY base; meanwhile, Emerald Bay Extracts advanced from #5 to #2 with 40.6% YoY sales growth, and ABX / AbsoluteXtracts stayed at #3 with a -7.0% YoY sales change, together suggesting Breez’s top position is defended not by absolute acceleration but by outperforming rivals that are either climbing from behind or contracting, which implies the rank trajectory points to durable category leadership that must counter a fast-closing #2.

Notable Products

Original Mint Tin 20-Pack (100mg) posted the steepest decline in July 2026 at -44.9% and slid to rank 6, while CBD/THC 1:1 Relief Cinnamon Mints 20-Pack (100mg CBD, 100mg THC) rose 10.5% to rank 5, signaling a shift within Edibles toward functional formulations. At the top, Indica Extra Strength Tablet 50-Pack (1000mg) held rank 1 despite a -7.0% dip and Sativa Extra Strength Tablet 50-Pack (1000mg) stayed at rank 3 with a -4.2% change, whereas Hybrid Extra-Strength Tablet 50-Pack (1000mg) gained 6.4% at rank 2, indicating Capsules leadership remains intact even with mixed momentum. Four of the top ten are Edible SKUs but the top three are all Capsules, and CBD Extra Strength Recovery Tablet 50-Pack (1000mg CBD) fell -13.6% at rank 9 against the Nighttime 2:1:1 Tablets’ -7.7% at rank 7, implying wellness-oriented Capsules need SKU-specific positioning rather than category lift. The product mix points to Breez leaning into high-dose Capsules for volume while selectively refreshing Edibles to stabilize volatility and capture functional demand.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.