Market Insights Snapshot

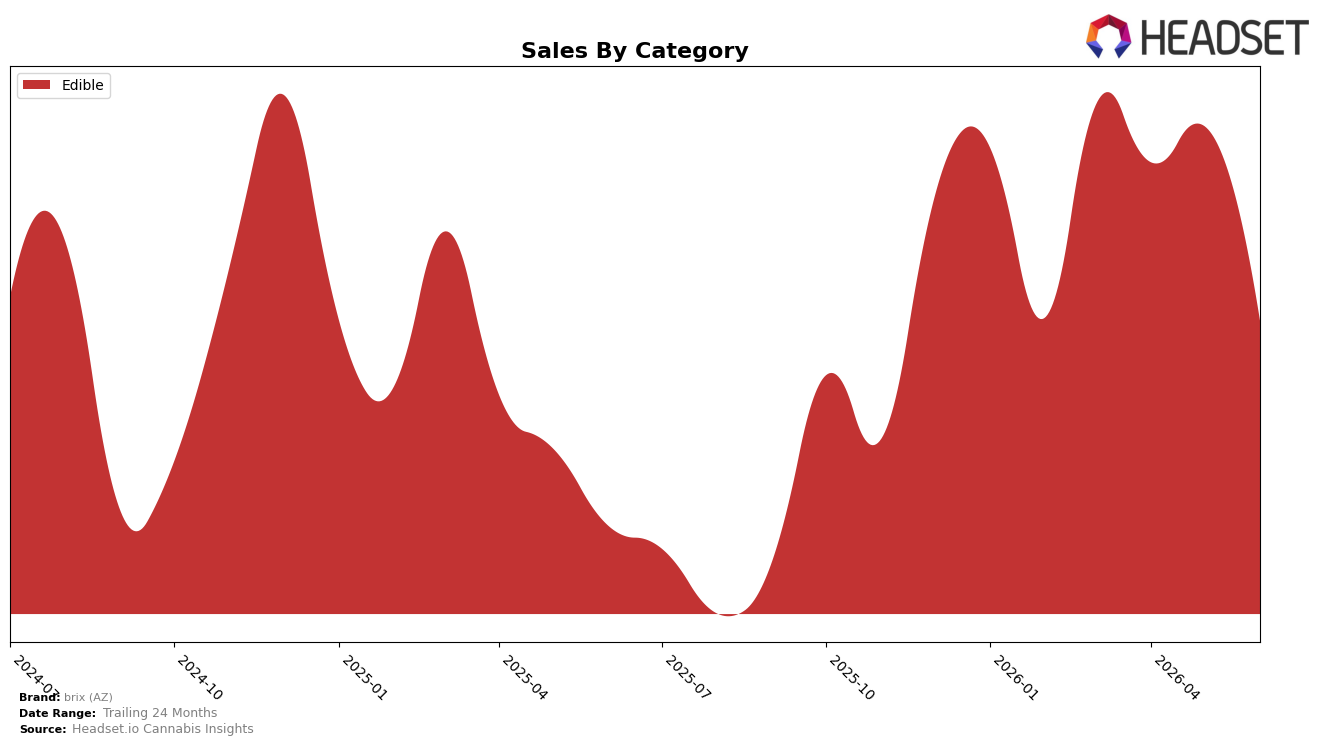

In June 2026, brix (AZ) concentrated entirely in Edible with a 100.0% category share, pairing year-over-year sales growth of 18.7% with a month-over-month decline of 13.0%. Average price fell 7.7% YoY to $6.99 while sales rose, and within Edible the brand held rank 8 in Arizona; the combination of double-digit YoY growth and a double-digit MoM pullback implies demand is expanding on an annual basis but is price-sensitive and susceptible to short-cycle volatility.

The shift toward a single-category footprint at 100.0% share, alongside an 18.7% YoY increase but a 13.0% MoM contraction, positions brix (AZ) as a scale player in value-leaning Edibles where price moves matter more than mix changes. Holding rank 8 in Arizona while cutting average price 7.7% YoY suggests the brand is trading price for velocity, which implies near-term gains are likely to come from deeper penetration and repeat in Edibles rather than premiumization or cross-category expansion.

Competitive Landscape

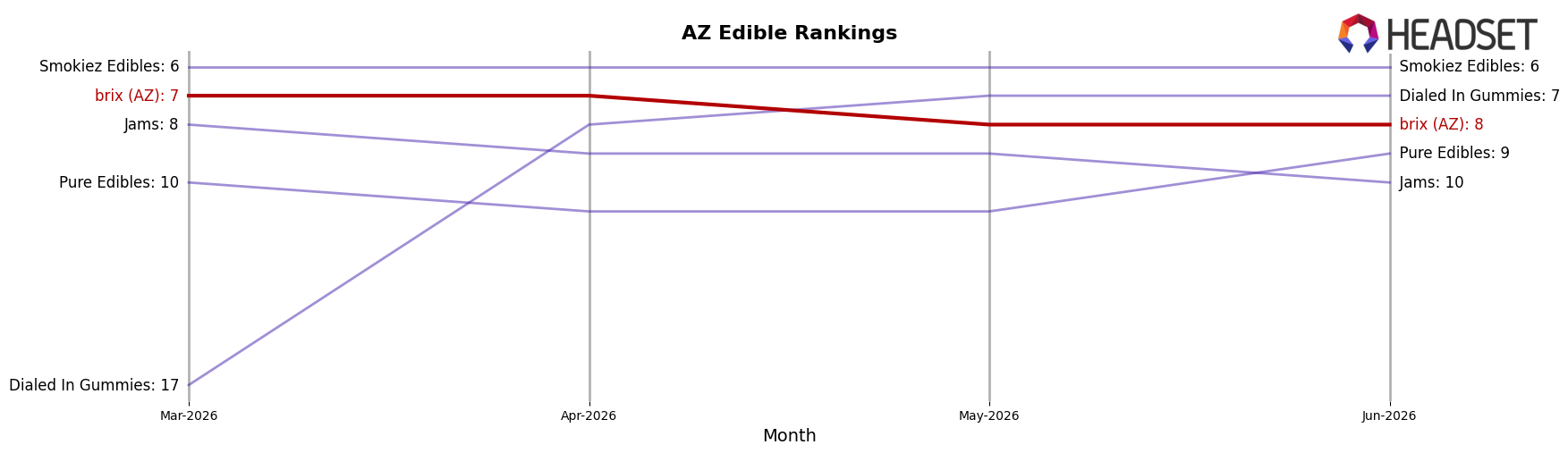

brix (AZ) is currently ranked #8 in AZ Edible, improving 2 positions from #10 year over year, but slipping 1 position from #7 in April 2026 to #8 in June 2026; this places the brand 1 rank below its peak of #7 and 1 rank behind its three-month position of #7. In contrast, Wyld held at #1 year over year while its sales declined 15.3%, and Baked Bros climbed from #4 to #3 with 30.9% YoY sales growth, indicating competitors are either defending or gaining share even as brix (AZ) edges up the table. The pattern implies brix (AZ) has achieved incremental rank recovery year over year but is losing short-term momentum versus upward-moving peers, pointing to a need to convert its brief April 2026 peak into sustained gains.

Notable Products

Blackberry Raspberry Big Dose Gummies 2-Pack (1000mg) posted the steepest decline at -31.1% month over month and fell to rank 5, while Blueberry Pomegranate Big Dose Gummies 2-Pack (1000mg) dropped -33.0% to rank 7; this tandem slide in high-dose formats implies waning pull for bulk-potency SKUs as price-sensitive or dosage-moderate buyers set the pace. Strawberry Watermelon Gummy (100mg) retained rank 1 but fell -14.8% MoM, and Blackberry Raspberry Gummy (100mg) at rank 3 slid -13.1%, signaling that even core 100mg leaders are cooling as category velocity resets. Four of the top ten are 100mg gummies and four are 1000mg two-packs, yet the 100mg cohort limited declines to a range of -1.9% to -14.8% versus -31% to -33% for 1000mg, indicating a mix shift back toward standard-dose units rather than value-size potency. With June 2026 overall ranks still concentrated in Edible gummies and a top SKU generating $76,597, the pattern points to prioritizing breadth and promotional support in 100mg flavors while reevaluating pricing or pack architecture for 1000mg two-packs.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.