Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

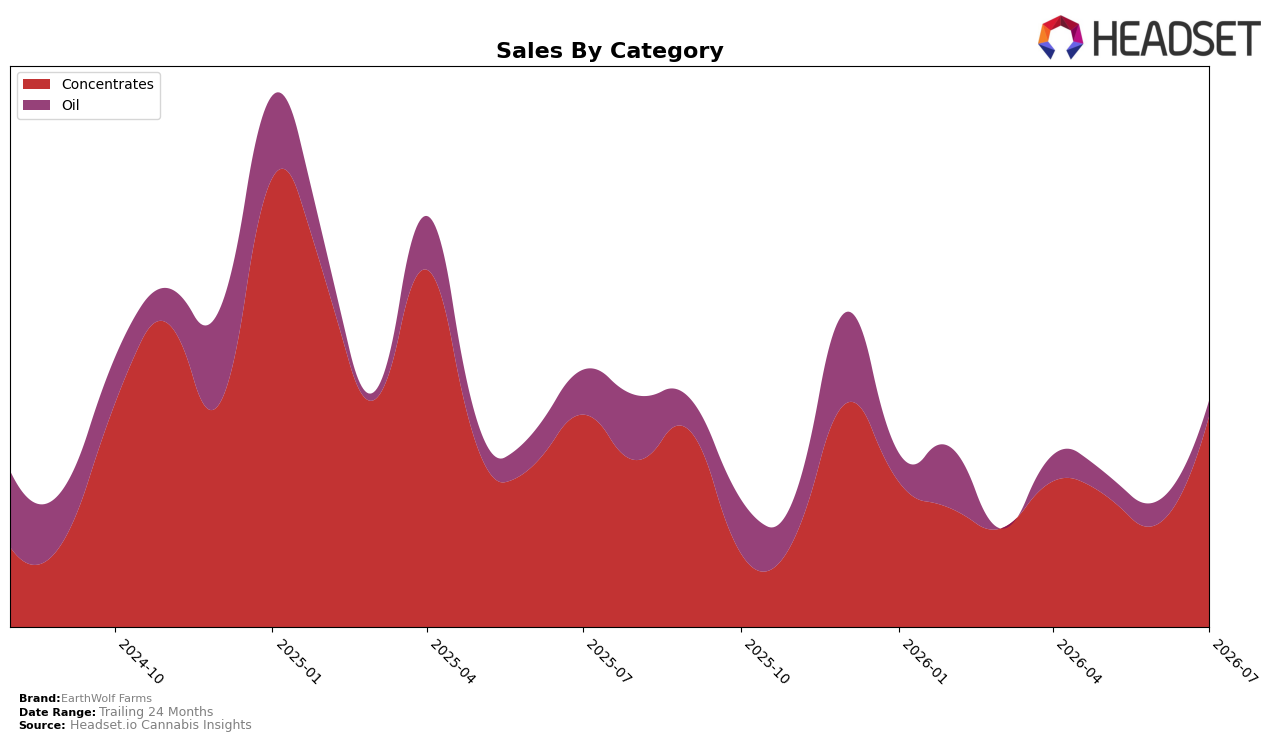

In July 2026, EarthWolf Farms concentrated 88.84% of sales in Concentrates while Oil held 11.16%, with Concentrates up 93.71% month over month but down 0.73% year over year, and Oil down 21.04% MoM and down 51.00% YoY. The brand’s average price rose 3.52% YoY to $45.22 even as total brand sales fell 10.93% YoY, and within the lead category the average price stood at 46.62, implying a price mix tilt toward higher-value SKUs. With Concentrates ranked 22 in British Columbia and commanding a dominant internal share alongside a contracting Oil line, the pattern implies a deliberate reallocation toward the higher-velocity Concentrates portfolio despite broader brand-level contraction.

The surge of 93.71% MoM in Concentrates against a 21.04% MoM decline in Oil, paired with a 0.73% YoY dip in Concentrates versus a 51.00% YoY collapse in Oil, indicates EarthWolf Farms is leaning into category resilience rather than chasing breadth; this concentrates the brand’s risk but also clarifies positioning around extract-led value. The 3.52% YoY price increase and a Concentrates-heavy mix suggest pricing power is being tested to support margin even as brand sales are down 10.93% YoY, and holding rank 22 in British Columbia for Concentrates implies the path to share recovery runs through deeper penetration and assortment refinement within that category rather than reviving Oil.

Competitive Landscape

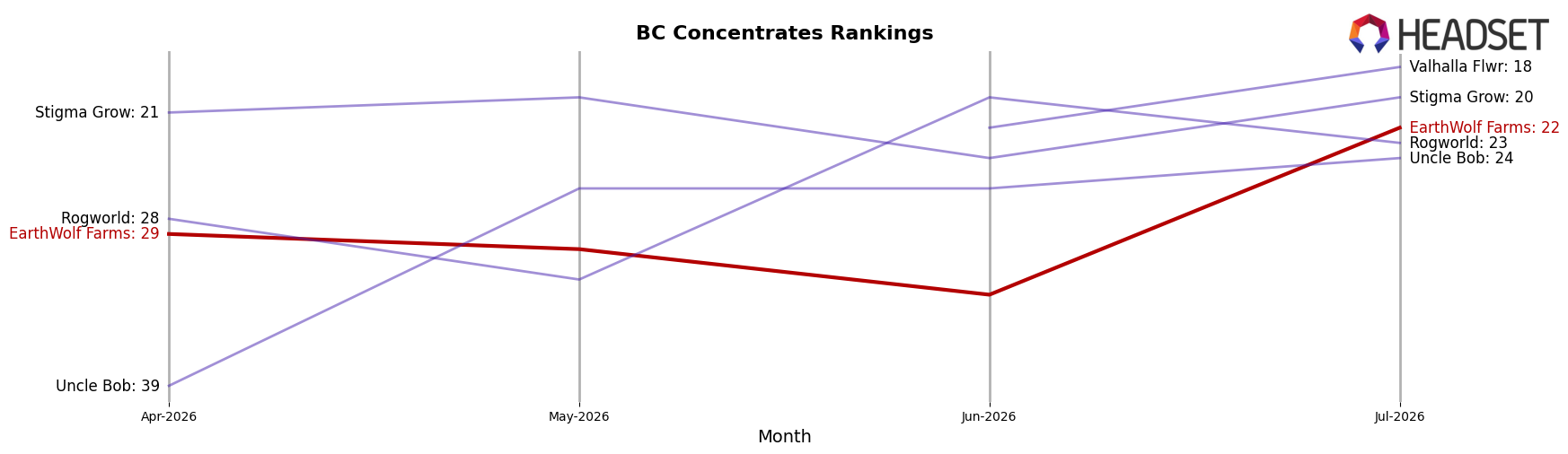

EarthWolf Farms is ranked #22 in BC Concentrates in July 2026, improving 3 positions year over year from #25 and climbing 7 ranks versus April 2026 from #29, while still 9 spots below its January 2025 peak at #13; in contrast, BoxHot rose from #8 to #3 with 98.6% YoY sales growth and Vortex Cannabis Inc. stayed at #2 despite a 27.5% YoY sales decline, indicating that EarthWolf Farms’ steady rank gains amid mixed competitor momentum suggest a gradual move toward mid-tier relevance if it can convert rank stability into higher share.

Notable Products

Grapefruit Mac Live Rosin (1g) posted the largest move in July 2026 with +160.7% month over month and reached rank 2, while Zen Oil (30ml) fell -21.1% to rank 4, indicating demand is tilting toward solventless formats over ingestible oils. Northern Apple Jaxx Live Rosin (1g) grew +77.8% and secured rank 1, whereas Acapulco Gold Live Rosin (1g) declined -43.7% at rank 6, and five of the top six products are Concentrates, signaling a concentrated basket within the Live Rosin family. With Afghan Hash (2g) slipping -9.5% at rank 5 alongside the single oil SKU’s -21.1% drop and Northern Apple Jaxx Live Rosin (1g) leading unit velocity on $17,180 in sales, the mix points to a portfolio pull toward premium rosin formats and away from oils.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.