Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

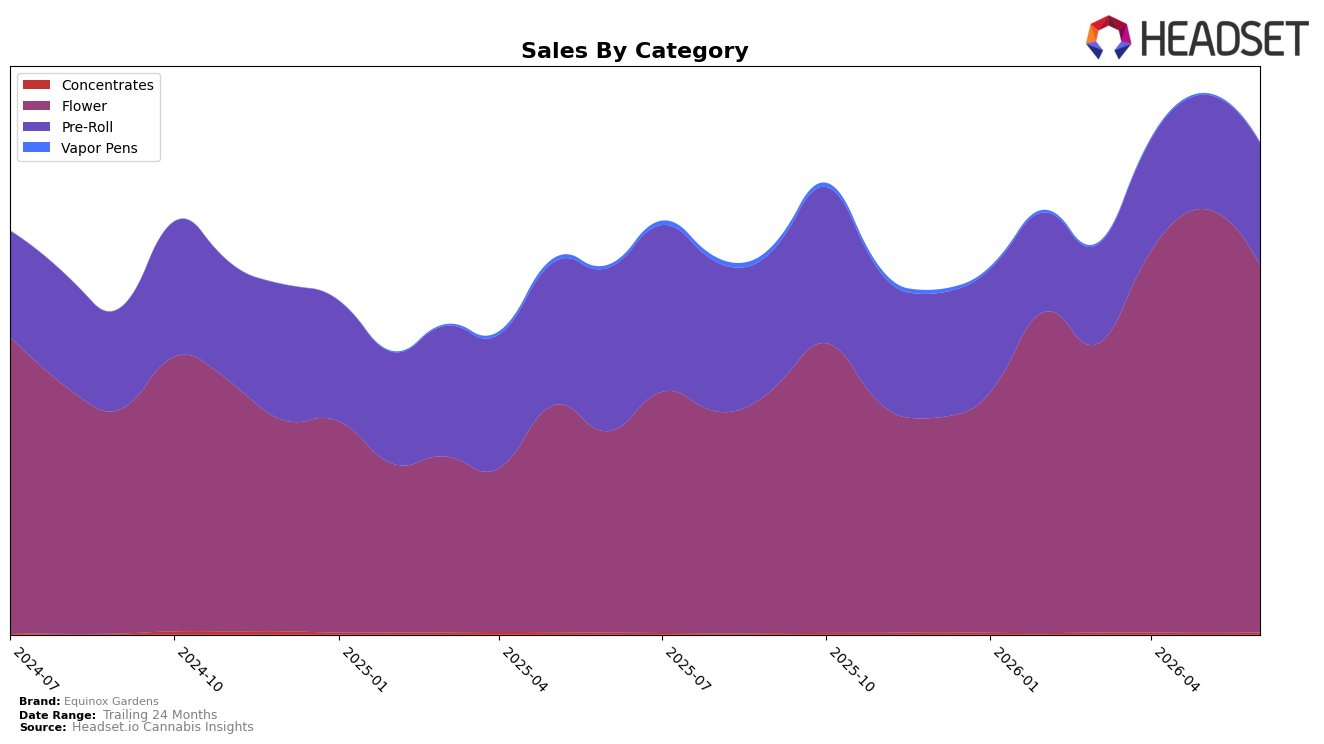

Equinox Gardens is concentrated in Flower at 74.61% share with year-over-year growth of 82.43% but a month-over-month decline of 13.38%, while Pre-Roll holds 24.84% share with a year-over-year drop of 25.08% and a month-over-month rise of 7.12%; smaller lines moved unevenly as Concentrates grew 26.28% MoM and 5.67% YoY to 0.39% share, and Vapor Pens fell 41.21% MoM and 71.60% YoY to 0.16% share. The brand’s average price rose 11.04% YoY to $26.20 as category mix tilted further toward higher-priced Flower and away from Vapor Pens, implying a volume-led uplift in core formats despite near-term pullback within Flower; the thesis is that June 2026 mix shifts consolidate revenue around Flower while leaving measured optionality in Pre-Roll.

The pattern implies Equinox Gardens is prioritizing depth in Flower over breadth across inhalables, consistent with a Colorado Flower rank of 7 and a 33.37% brand-level sales increase YoY even as Flower contracted MoM by 13.38% and Pre-Roll expanded MoM by 7.12%. With Vapor Pens contracting 71.60% YoY and Concentrates advancing 26.28% MoM off a 0.39% base, the portfolio is de-risking from volatile ancillary formats and leaning into categories where price power can support the 11.04% YoY ASP lift; the thesis is that this positioning trades category breadth for higher share-of-wallet in Flower while using Pre-Roll momentum as a hedge against Flower’s monthly variability.

Competitive Landscape

Equinox Gardens ranks #7 in CO Flower in June 2026, improving 7 positions from #14 year over year and jumping 6 spots from #13 in March 2026, while still sitting 2 places below its April 2026 peak at #5; in contrast, Seed & Strain Cannabis Co. climbed from #2 to #1 with 62.8% YoY sales growth and Good Chemistry Nurseries slipped from #1 to #3 with a -2.8% YoY sales change, and Natty Rems surged from #28 to #5 on 221.0% YoY growth, indicating that Equinox Gardens’ upward shift is outpacing legacy leaders but lagging behind the most aggressive movers; the pattern implies Equinox Gardens is transitioning from mid-tier volatility toward upper-tier stability, with the next test being whether it can convert the April 2026 peak into a sustained top-5 position.

Notable Products

Caked Up Kandy (14g) posted the standout move in June 2026 with a +70.6% month-over-month surge to $119,401 while taking rank 1, as Gelato Cake (14g) slid -19.8% and sat at rank 6. Mile High Mousse (3.5g) fell -11.4% and ranked 2, creating a split where the leader accelerated while a key smaller-size SKU contracted, and seven of the top ten are Flower formats in 14g packs. The pattern implies Equinox Gardens is tilting toward higher-volume 14g Flower winners even as select 3.5g and mid-pack offerings lose momentum, signaling a product mix that prioritizes bulk Flower velocity over breadth in smaller sizes.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.