Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Fifty Fold is stocked at 99 licensed dispensaries across Washington, with the deepest coverage in Seattle, Spokane, Bellevue, Bellingham, and Everett. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

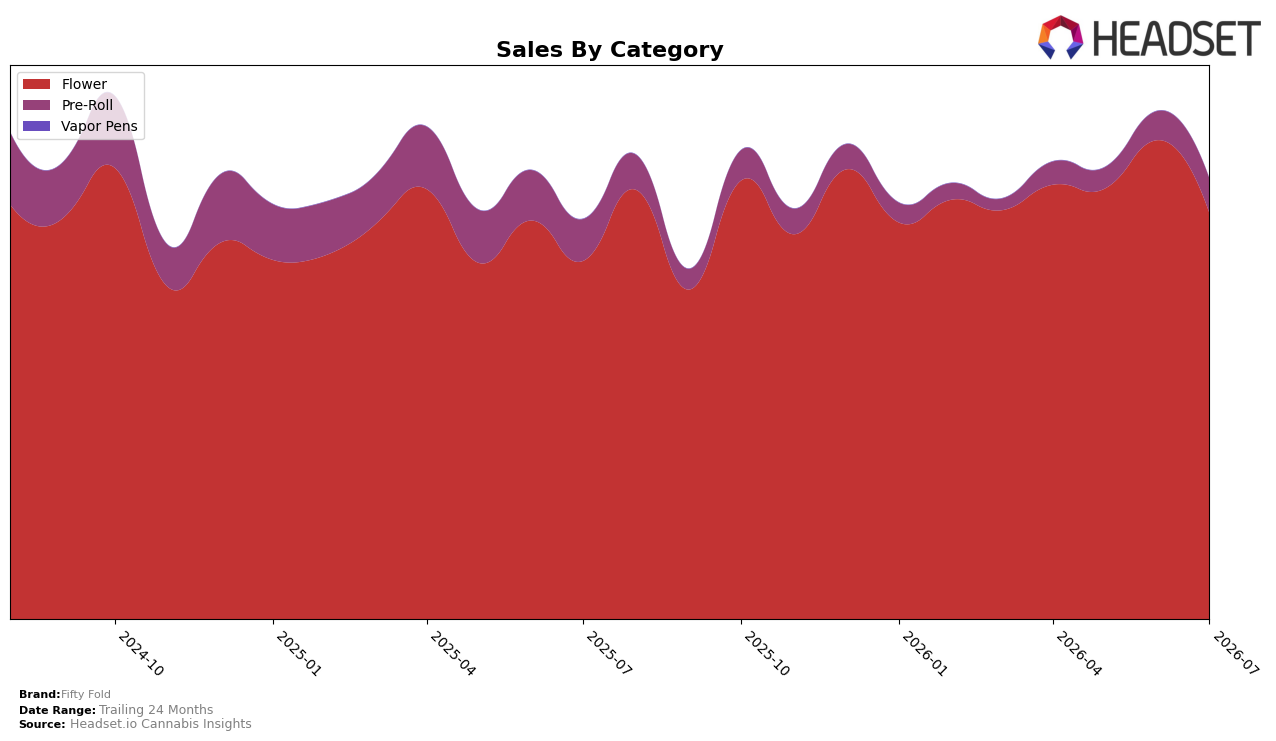

Fifty Fold’s mix in July 2026 concentrated 92.20% of sales in Flower with Pre-Roll at 7.80%, while Flower grew 13.32% year over year but fell 15.27% month over month; in contrast, Pre-Roll declined 17.27% year over year but rose 18.81% month over month. Overall brand sales were up 10.13% year over year even as the 24‑month trend sat at -6.54%, and the average price rose 17.43% year over year to $16.36. With Flower ranked 9th in Washington and accounting for over nine-tenths of mix, the pattern implies the brand is leaning into a high‑price Flower-led strategy that is lifting annual comps while exposing monthly volatility when Flower softens.

The juxtaposition of a 15.27% month-over-month Flower dip and an 18.81% month-over-month Pre-Roll lift indicates substitution at the edges of the portfolio, and the 17.43% year-over-year price increase alongside a 13.32% year-over-year Flower gain suggests pricing power anchored in core Flower rather than Pre-Roll, which was down 17.27% year over year. Given the 92.20% mix in Flower and a 9th-place category rank in Washington, the implication is that short‑term stability will depend on smoothing Flower’s monthly swings and selectively expanding Pre-Roll to 9–12% share so that the brand can preserve the 10.13% year-over-year sales lift while reducing exposure to one category’s month-to-month shock.

Competitive Landscape

Fifty Fold sits at rank #9 in WA Flower in July 2026, improving 3 positions year over year from #12 and slipping 2 positions since April 2026 when it was #7; the brand also came off a peak of #4 in June 2026 before the current 5-place retreat month over month. In contrast, Phat Panda held at #1 with a 18.6% YoY sales increase while Lifted Cannabis Co climbed from #8 to #3, and Sweetwater Farms advanced from #14 to #5 with a 48.2% YoY gain, indicating that Fifty Fold’s brief surge to #4 in June 2026 followed by a drop to #9 in July 2026 points to momentum volatility rather than sustained share capture.

Notable Products

Funky Oranges (3.5g) posted the largest month-over-month movement in July 2026 at +43.7% while climbing to rank 3, whereas Lemon Cherry Gelato (3.5g) declined -6.6% at rank 10. Snickerdoobie - Nite Nite Kief Rosin Infused Pre-Roll 2-Pack (1.5g) led the board at rank 1 with +34.3% MoM, signaling that the lone Pre-Roll is outpacing Flower peers despite lower absolute sales of $11,799. With eight of the top ten positioned in the Flower category and two Flower SKUs in the top three, the mix points to a portfolio where Flower breadth anchors volume but targeted innovation in Pre-Rolls is winning rank share. The pattern implies Fifty Fold is tilting toward a two-pillar strategy: scale Flower variants for shelf coverage while using an infused Pre-Roll hero to capture velocity at the top of the chart.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.