Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

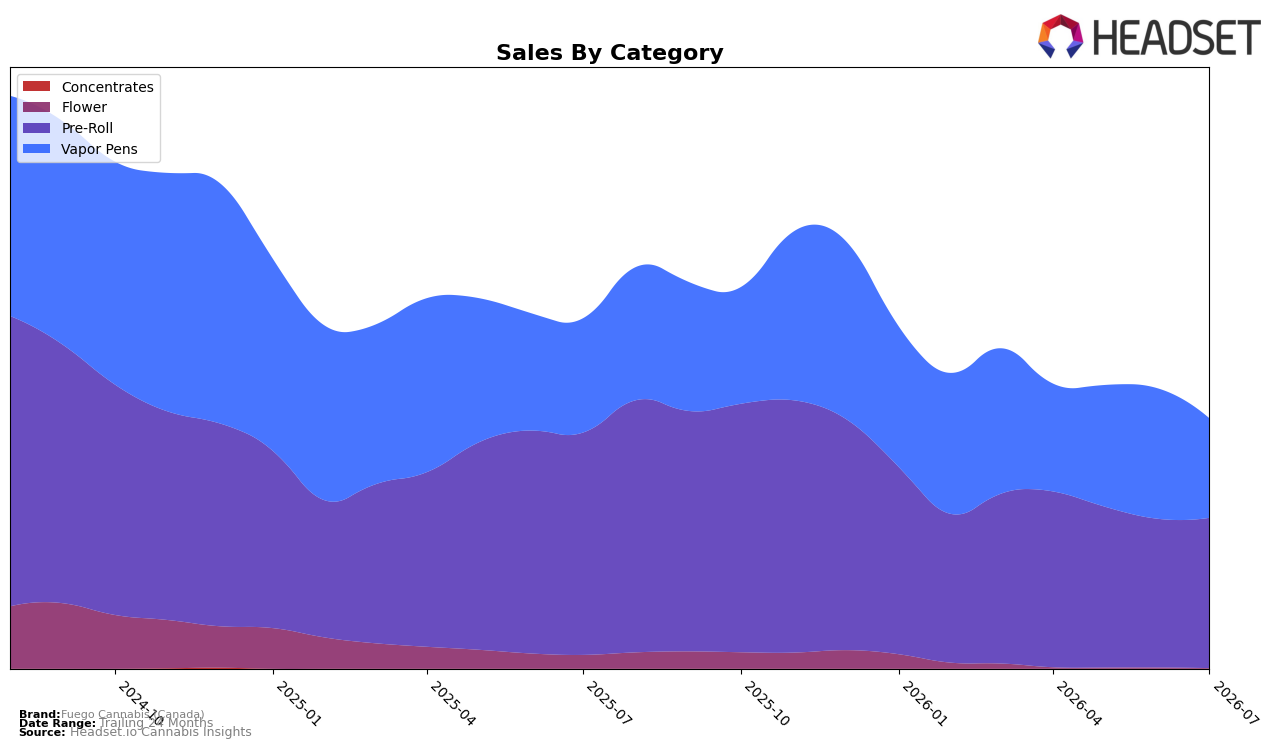

In July 2026, Fuego Cannabis (Canada) concentrated 60.09% of sales in Pre-Roll with a year-over-year decline of 32.46% but a month-over-month uptick of 1.09%, while Vapor Pens held 39.75% share with a 12.99% YoY drop and a 23.73% MoM slide; Flower shrank to 0.16% share with a 97.13% YoY and 61.99% MoM decline. Against a brand-level sales change of -28.62% YoY and an average price up 11.18% YoY to $13.34, the category mix skews toward lower-priced Pre-Roll (average price $9.69) and away from higher-priced Vapor Pens (average price $30.86), implying July 2026 revenue was cushioned more by volume resilience in Pre-Roll than in premium-priced formats.

With Pre-Roll ranked 18th in Ontario and lifting slightly MoM (+1.09%) while Vapor Pens contracted sharply MoM (-23.73%), Fuego Cannabis (Canada) is tilting toward a value-led, Pre-Roll-centric position rather than margin-rich Vapor Pens. The simultaneous price inflation (+11.18% YoY) and mix shift toward a 60.09% Pre-Roll share suggest competitive pressure is pushing the brand to prioritize accessible ticket sizes over premiumization, which implies near-term share defense in Pre-Roll at the expense of Vapor Pen momentum and overall rank advancement.

Competitive Landscape

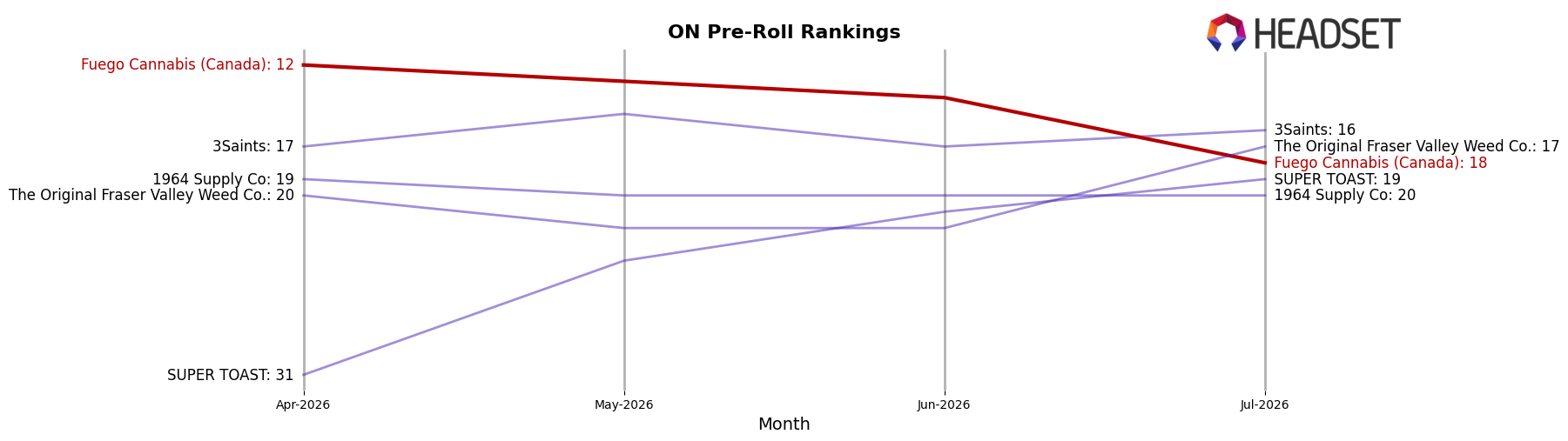

Fuego Cannabis (Canada) sits at rank #18 in Ontario Pre-Roll for July 2026, down 6 spots year over year from #12, and also down 6 positions versus three months ago at #12; this follows a longer slide from a peak of #6 in August 2024 to outside the top 15, indicating share redistribution rather than a temporary dip. Competitively, Back Forty / Back 40 Cannabis moved up from #2 to #1 with a 67.4% year-over-year sales lift, while General Admission fell from #1 to #2 alongside a 23.2% year-over-year decline, showing that leadership churn is active at the very top as Fuego Cannabis (Canada) moves the other direction. The implication is that Fuego Cannabis (Canada)’s downward rank trajectory—6 ranks off year over year and 12 ranks below its August 2024 peak—suggests a need to counter competitors gaining momentum at the top end.

Notable Products

Sunny Daze Pre-Roll (1g) posted the steepest decline at -20.8% month over month while dropping to rank 4, and Night Rider Pre-Roll (1g) fell -10.0% at rank 3, signaling pressure on single-stick formats even as Sunny Daze Pre-Roll 2-Pack (2g) held rank 1 with a -2.3% dip. In contrast, Dream Weaver Pre-Roll (1g) rose 37.2% at rank 5 and Dream Weaver Pre-Roll 2-Pack (2g) climbed 28.1% at rank 9, indicating mix shift toward a few rising strains despite broader softness.

Pre-Rolls occupied nine of the top ten slots, with two-pack formats at ranks 1, 2, and 6 moving -2.3% to +6.0% while the lone Vapor Pens entry, Red Maui Wowie Liquid Diamonds Cartridge (1g), slid -14.4% at rank 10 off $143,101. Night Rider Pre-Roll 2-Pack (2g) grew +6.0% at rank 2 versus Galactic Fire Pre-Roll 2-Pack (2g) at rank 6 with -2.3%, implying consumer trade-up within multipacks toward specific strain equity rather than the broader family.

Within branded families, Sunny Daze split sharply with -2.3% for the 2-Pack at rank 1 versus -7.3% for the 4-Pack at rank 7, and Night Rider split with +6.0% for the 2-Pack at rank 2 versus -10.0% for the 1g at rank 3. Four of the top ten are single-stick 1g SKUs and five are 2-Pack SKUs, pointing to a polarized basket where trial-sized singles coexist with value two-packs, suggesting Fuego Cannabis (Canada) is consolidating around multipack-led velocity while pruning underperforming single-stick variants.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.