Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

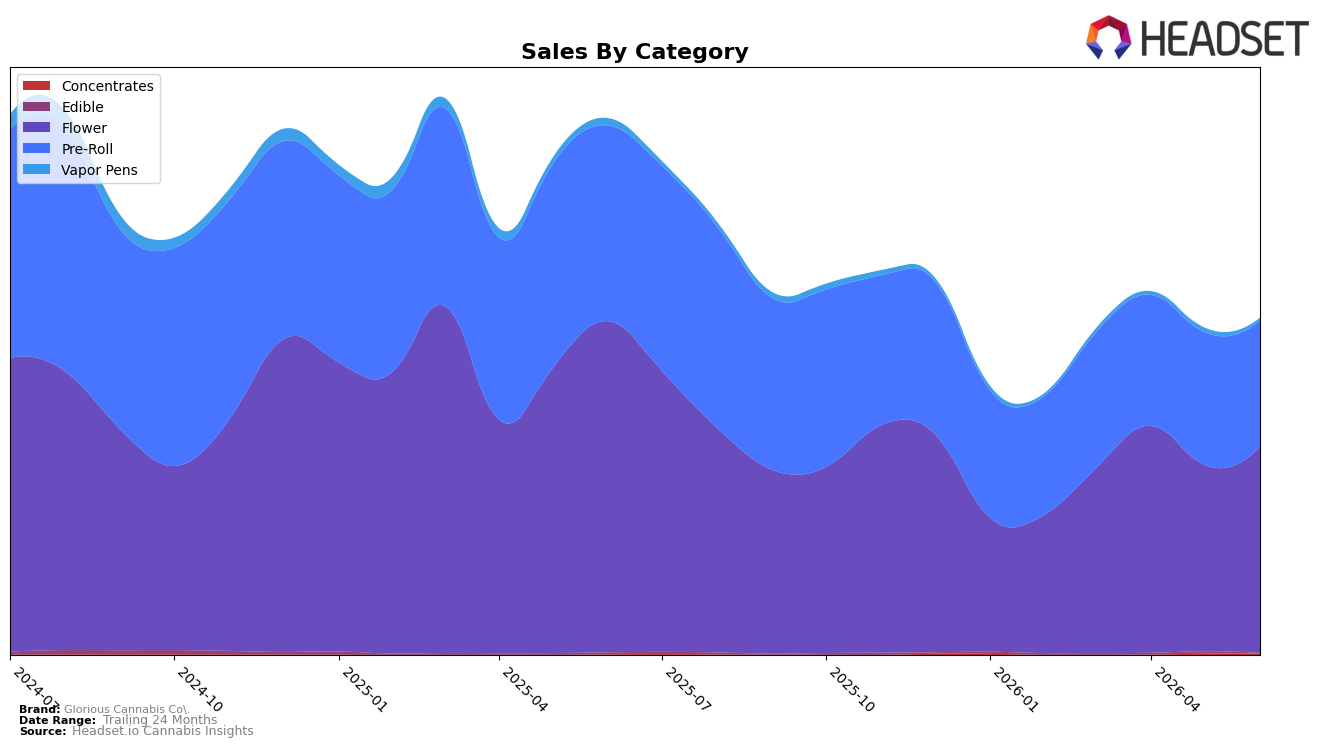

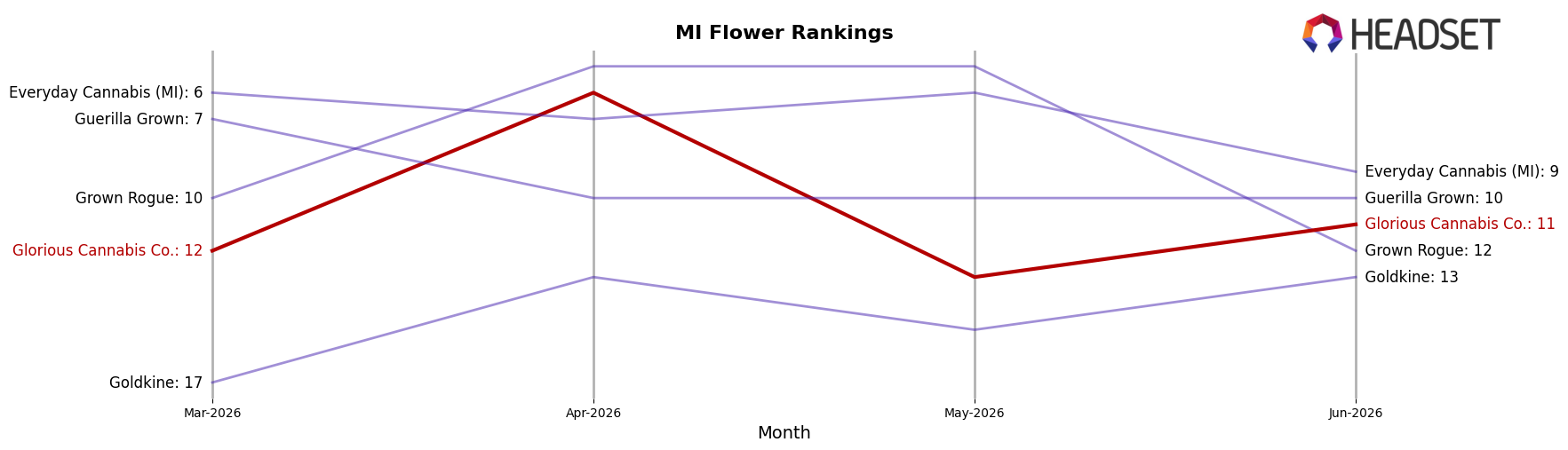

Glorious Cannabis Co. concentrated 61.39% of June 2026 sales in Flower with a 10.76% month-over-month increase but a 37.66% year-over-year decline, while Pre-Roll held 37.42% share with a 4.99% MoM decline and a 35.65% YoY decline; the remaining mix was minimal, with Vapor Pens at 0.72% share and down 42.22% MoM and 65.79% YoY, and Edible at 0.12% share and down 81.12% MoM and 76.84% YoY. Despite Concentrates growing 3.03% MoM and 159.16% YoY, the category represented just 0.35% of sales, leaving overall brand sales down 37.26% YoY even as average price fell 12.08% YoY; in Michigan Flower specifically, the brand stood at rank 11. The pattern implies the brand’s volume is tethered to Flower and Pre-Roll swings, with June’s Flower rebound insufficient to offset double-digit YoY declines across core inhalables.

Given Flower’s 61.39% share and Pre-Roll’s 37.42% share, Glorious Cannabis Co. is positioned as a value-forward inhalables player, evidenced by a 12.08% YoY decline in average price alongside a June Flower MoM lift of 10.76% but a Pre-Roll MoM contraction of 4.99%. With Vapor Pens collapsing 42.22% MoM and 65.79% YoY and Edible collapsing 81.12% MoM and 76.84% YoY, the portfolio breadth is narrowing rather than diversifying; even a 159.16% YoY gain in Concentrates at just 0.35% share cannot reshape mix. The implication is a need to defend Flower rank 11 in Michigan while stabilizing Pre-Roll, because June 2026 momentum depends more on maintaining share in these two categories than on expanding low-base segments.

Competitive Landscape

Glorious Cannabis Co. sits at rank #11 in June 2026, down 5 positions from #6 in June 2025, while its 3-month position edged from #12 to #11 and remains 6 spots off its peak at #5 in March 2025; meanwhile, High Minded held #1 year over year despite a -13.7% sales change and Goodlyfe Farms advanced from #5 to #2 on +44.1% sales, indicating Glorious Cannabis Co.’s downward YoY rank shift contrasts with competitors that either retained leadership or accelerated upward and implies the brand’s trajectory is one of relative share loss unless rank momentum turns from a -5 YoY slide into sustained quarterly gains.

Notable Products

Fire Styxx - Grape Escape Infused Pre-Roll (1g) posted the steepest movement in June 2026 with a -28.1% month-over-month drop while holding rank 4, contrasting with Fire Styxx - Green Fury THCA Infused Pre-Roll (1g) up 19.4% at rank 9; this bifurcation implies flavor-specific volatility rather than a category-wide slump. Fire Styxx - Unicorn Tears THCA Infused Pre-Roll (1g) slid -10.5% to rank 2 even as Fire Styxx - Royal Punch Infused Pre-Roll (1g) in rank 1 grew 5.1%, indicating share is consolidating at the very top while mid-pack THCA SKUs retrench. Eight of the top ten are Pre-Roll variants under the Fire Styxx family, and with only one SKU showing double-digit growth against three with double-digit declines, the mix points to a need to rebalance toward the few flavors gaining velocity rather than expanding breadth. The pattern signals Glorious Cannabis Co. is leaning on a concentrated Pre-Roll lineup where selective SKU pruning and targeted pushes on the highest-momentum flavors could drive steadier rank retention and margin, especially around the $130,842 leader.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.