Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

In June 2026, Good Tide remained a single-category brand with 100.0% of sales in Edible, holding that mix while Edible sales grew 28.3% year over year and slipped 1.8% month over month. The average price rose 8.8% YoY to $18.62, even as MoM sales contracted, implying volume softness concurrent with pricing. With brand sales up 28.3% YoY and a 24‑month gain of 88.7%, the one-category concentration amplified YoY upside but left no offset during the MoM dip; the pattern implies that June 2026 outcomes were driven more by pricing and Edible demand timing than by portfolio breadth.

Positioning in Edible is reinforced by a category rank of 4 in Oregon, pairing a top‑five slot with 100.0% category exposure and an 8.8% YoY price lift. The combination of a 28.3% YoY sales increase and a −1.8% MoM change suggests Good Tide is trading up within Edible while absorbing short‑cycle volatility, and rank 4 signals sufficient scale to influence price without cross‑category spillover. The pattern implies that Good Tide’s near‑term leverage comes from price and rank within Edible rather than mix diversification, concentrating both upside and risk in a single demand curve.

Competitive Landscape

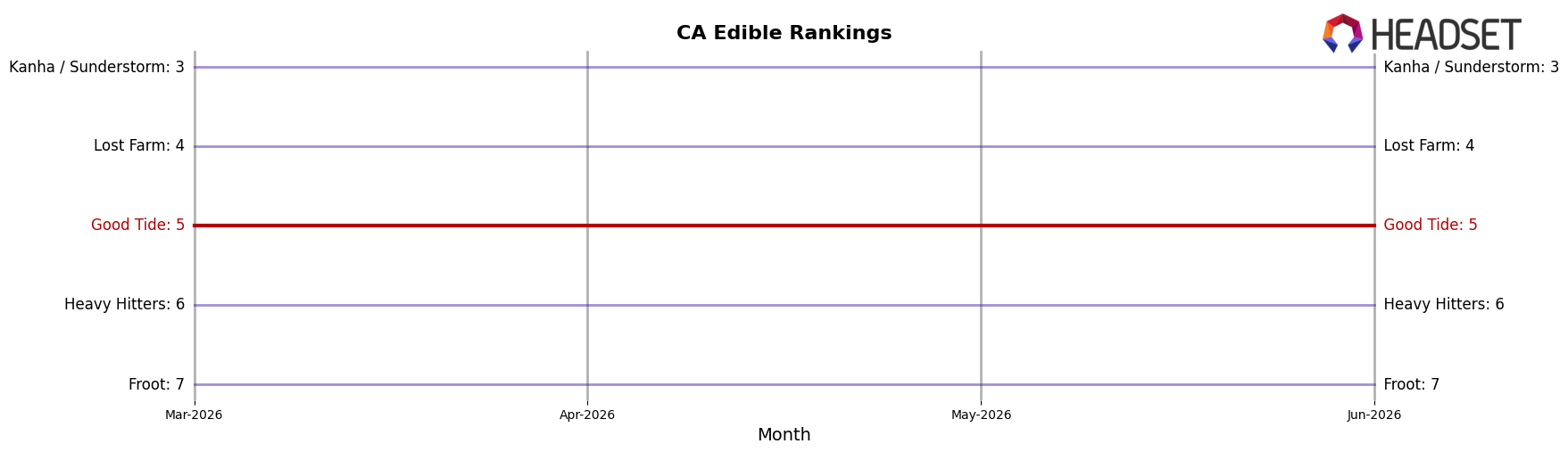

Good Tide holds rank #5 in CA Edible in June 2026, unchanged from #5 in June 2025, and stable at #5 since March 2026, while the category leader Wyld remains at #1 year over year despite a -1.9% sales change and Camino stays at #2 with a +12.9% sales change; additionally, Kanha / Sunderstorm sits at #3 with +10.9% and Lost Farm at #4 with +7.2%, indicating that Good Tide’s flat rank at its peak (#5) coexists with upward sales momentum among immediate rivals. The pattern implies Good Tide’s share is capped by faster-growing competitors just above it, so without a relative acceleration that outpaces the +7% to +13% gains among ranks #2–#4, the brand is likely to remain anchored at #5 rather than convert stability into upward mobility.

Notable Products

Hybrid Guava Solventless Hash Rosin High Dose Gummies 10-Pack (200mg) posted the standout move with a 24.97% month-over-month gain into rank 9, while the flagship Uplifting Sativa Pineapple Solventless Hash Rosin Gummies 10-Pack (100mg) slipped 3.76% yet held rank 1. June 2026 saw the top three skus—ranks 1, 2, and 3—each down between 0.02% and 3.76%, and six of the top ten were down month over month, signaling that growth concentrated in smaller base, high-dose formats rather than the core 100mg lineup. With four of the top ten belonging to the Pineapple, Passionfruit, Kiwi Strawberry, and Guava families under Edibles and two high-dose variants sitting in ranks 7 and 9, the mix points to a pivot where potency-led extensions are absorbing incremental demand even as flagship 100mg offerings consolidate share.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.