Mar-2026

Sales

Trend

6-Month

Product Count

SKUs

Overview

Market Insights Snapshot

Grassroots has shown a notable presence in the Flower category across various states, with some impressive movements in rankings. In Arizona, the brand jumped from 15th in January 2026 to 5th in February 2026, although it slightly declined to 7th by March. This indicates a strong surge in popularity, likely driven by strategic market positioning or product offerings. In Connecticut, Grassroots achieved a remarkable rise from being outside the top 30 in December 2025 to reaching 3rd place by March 2026, showcasing an impressive growth trajectory. Meanwhile, in Illinois, the brand maintained a consistent presence, peaking at 4th place in February 2026, before dropping to 10th in March. However, in Nevada, the brand experienced a downward trend, moving from 8th place in December 2025 to 16th by March 2026, which could suggest increased competition or market challenges.

In the Concentrates category, Grassroots has demonstrated strong performance in Maryland, consistently holding the top two positions from December 2025 to March 2026, even reaching the number one spot in February. This consistent performance highlights the brand's solid foothold in the state. In contrast, their presence in the Pre-Roll category has been less consistent. For example, in Illinois, Grassroots entered the top 30 in February 2026 at 10th place, but did not maintain a ranking in the subsequent month. Similarly, in Maryland, they appeared at 11th place in February and slipped to 13th by March. These fluctuations suggest potential areas for improvement in their Pre-Roll offerings or marketing strategies.

Competitive Landscape

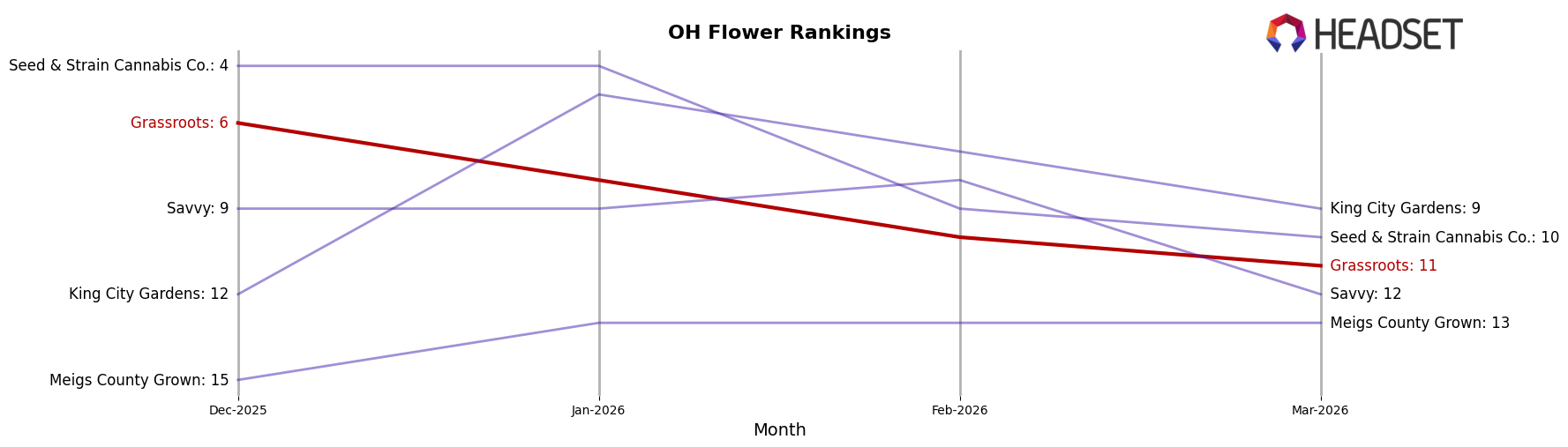

In the competitive landscape of the Flower category in Ohio, Grassroots has experienced a decline in rank from 6th in December 2025 to 11th by March 2026. This downward trend in rank is accompanied by a decrease in sales, reflecting a challenging period for Grassroots. Notably, Seed & Strain Cannabis Co. maintained a strong position, consistently ranking higher than Grassroots, despite a brief dip to 10th in February 2026. Meanwhile, King City Gardens showed significant improvement, climbing from 12th in December 2025 to 9th in March 2026, indicating a potential threat to Grassroots' market share. Additionally, Savvy and Meigs County Grown have shown varied performance, with Savvy's rank fluctuating and Meigs County Grown maintaining a steady position outside the top 10. These dynamics suggest that Grassroots may need to reassess its strategies to regain its competitive edge in the Ohio Flower market.

Notable Products

In March 2026, the top-performing product for Grassroots was Titan Express (3.5g) in the Flower category, maintaining its number one rank consistently from December 2025 through March 2026 with sales of 18,059 units. Grassroots x Dark Heart - Foreign Kush Mints (3.5g) secured the second position, showing a steady performance with increasing sales each month. Grassroots x Dark Heart - Triple Stack (3.5g) held the third spot, demonstrating stable rankings over the months. Pillow Mints (3.5g) emerged as a notable newcomer in the fourth position, while Grassroots x Dark Heart - Titan Express Pre-Roll (1g) consistently ranked fifth since January 2026. The consistent performance of these products highlights Grassroots' strong presence in the Flower category, with notable improvements in sales figures over the months.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.