Mar-2025

Sales

Trend

6-Month

Product Count

SKUs

Overview

Market Insights Snapshot

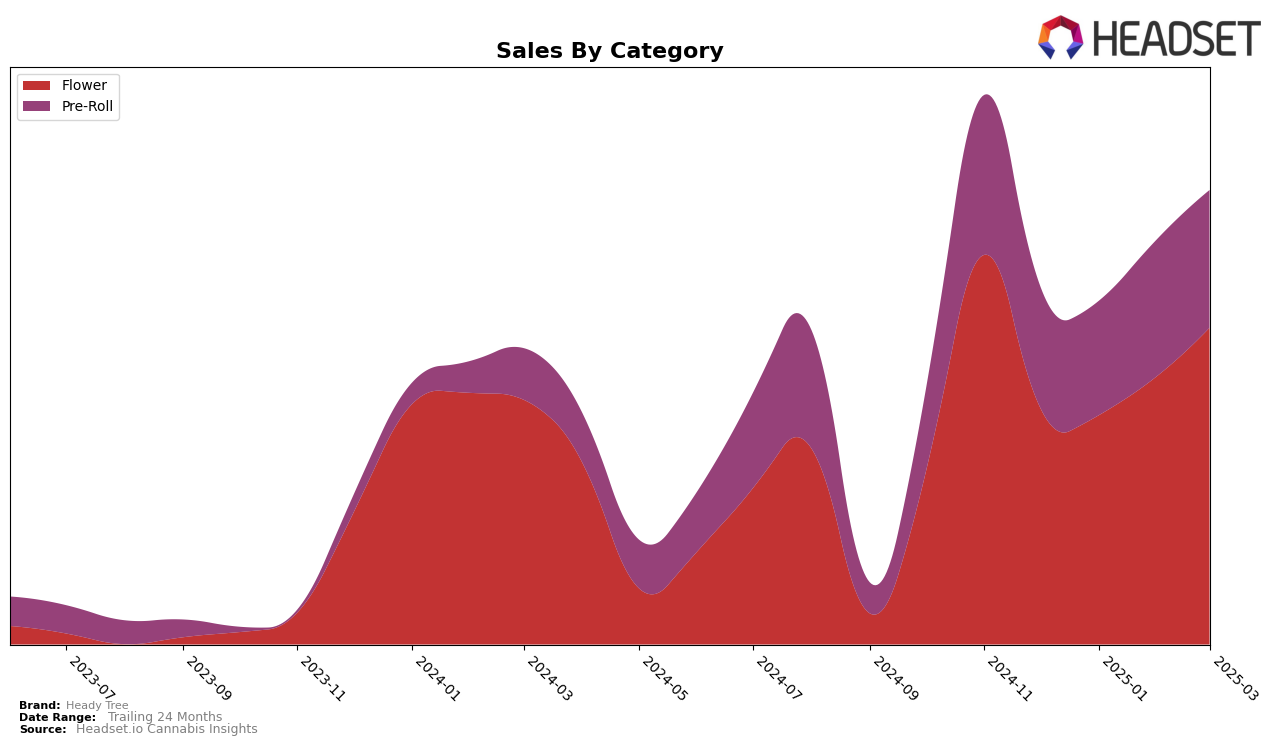

Heady Tree has demonstrated a consistent presence in the New York market, particularly within the Flower category. Over the four-month period, their rank has remained steady at 13th position, except for a slight dip to 15th in January 2025. This stability is underscored by a significant upward trend in sales, with March 2025 figures reaching $880,825, indicating a strong recovery and growth after a lower sales period in January. Such consistency in ranking, despite the competitive nature of the Flower category, suggests that Heady Tree is maintaining a robust market share in New York.

In contrast, Heady Tree's performance in the Pre-Roll category in New York has shown more fluctuation. Starting at 11th place in December 2024, they experienced a slight drop to 12th in January, before climbing back to 10th in February, only to return to 12th in March. Despite these shifts in rank, the sales figures reveal a positive trajectory, with March sales slightly increasing compared to February. This dynamic movement in rankings, while maintaining a position within the top 15, highlights both the competitive pressures and the brand's resilience in the Pre-Roll sector.

Competitive Landscape

In the competitive landscape of the New York flower category, Heady Tree has maintained a consistent performance, holding the 13th rank in December 2024, February 2025, and March 2025, with a slight dip to 15th in January 2025. This stability in ranking is noteworthy, especially when compared to competitors like Leal, which consistently held a higher rank at 11th throughout the same period, and Back Home Cannabis Co., which maintained the 12th rank. Heady Tree's sales trajectory shows a positive trend, with a significant increase from January to March 2025, indicating strong market demand and effective sales strategies. Meanwhile, Smokes (Canada) entered the top 20 in February 2025 and improved its rank to 14th by March, suggesting a growing competitive pressure. The surge in sales for The Botanist, which jumped to 15th rank in March 2025, further highlights the dynamic nature of this market, emphasizing the need for Heady Tree to continue innovating and adapting to maintain its market position.

Notable Products

In March 2025, the top-performing product from Heady Tree was Blue Zushi Pre-Roll (1g) in the Pre-Roll category, maintaining its first-place rank consistently from December 2024. It achieved sales of 5401 units, showing a slight decline from previous months. Candy Fumez Pre-Roll (1g) held steady in second place since January 2025, with a slight increase in sales to 4595 units. Da Yayo Pre-Roll (1g) remained in third place from February 2025, with a minimal decrease in sales to 4453 units. Notably, Pineapple Slushee Pre-Roll (1g) emerged as a new contender, securing the fourth rank with its entry into the market.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.