Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Hepworth is stocked at 153 licensed dispensaries across New York, with the deepest coverage in New York, Buffalo, Queens, Flushing, and Newburgh. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

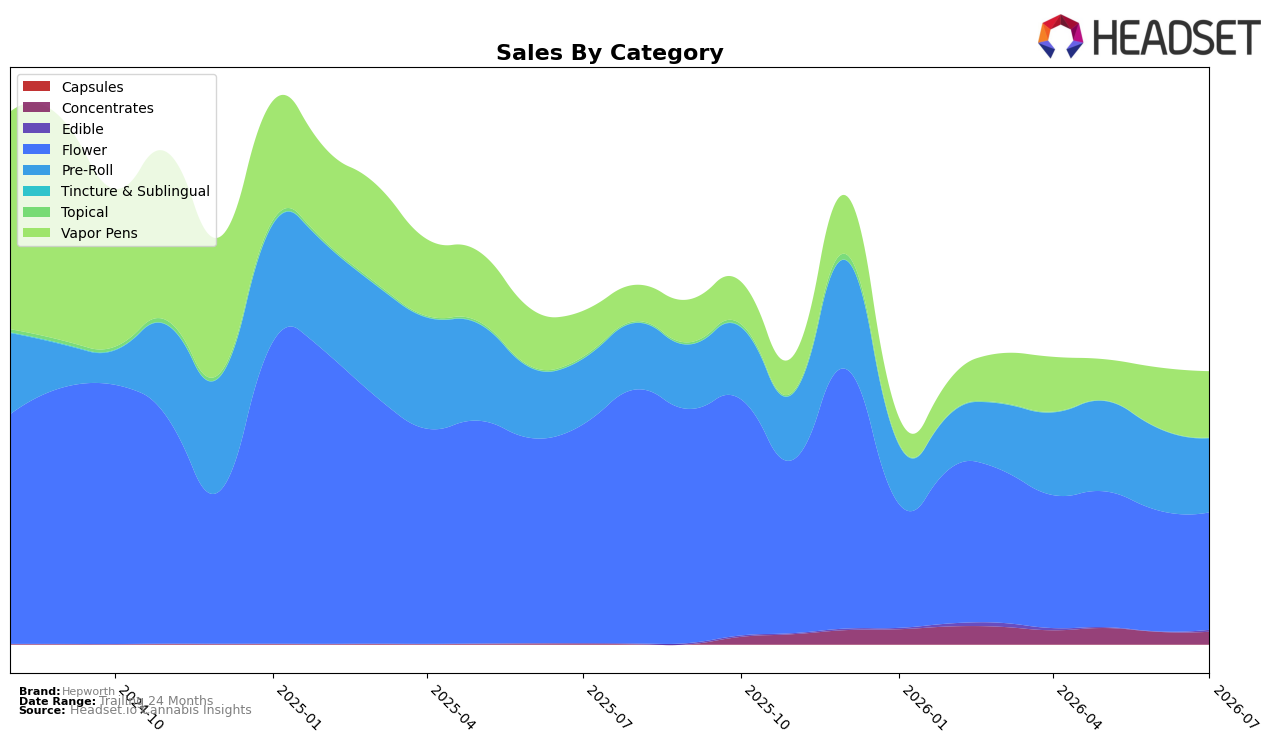

Hepworth’s category mix in July 2026 pivoted away from Flower, where sales fell 46.38% year over year and 3.01% month over month, cutting the category to 43.17% share, while Pre-Roll held 27.21% share on 13.18% year-over-year growth but declined 9.74% month over month. Vapor Pens expanded to 24.34% share with 45.11% year-over-year growth and a 10.04% month-over-month increase, and Concentrates, though only 4.63% share, surged 2084.42% year over year alongside a 0.65% month-over-month uptick; Edible remained just 0.62% share despite 326.34% year-over-year growth and a 994.29% month-over-month jump. The combined effect is a reweighting toward inhalables and niche formats even as overall brand sales fell 18.21% year over year and average price dropped 29.32%, implying a deliberate move down-price and away from the declining Flower core.

This reshuffle implies a positioning shift: dependence on Flower is easing as the brand leans into Vapor Pens’ 10.04% month-over-month momentum and Pre-Roll’s 27.21% share despite its 9.74% month-over-month pullback, using lower average prices in these formats ($19.88 for Vapor Pens and $20.18 for Pre-Roll) compared with $27.72 in Flower to defend volume. With a 41 rank in Flower in New York and a 24-month sales decline of 41.71%, the path forward is clearer: accelerate growth pockets like Vapor Pens (+45.11% year over year) while treating the outsized but thin Edible spike (+994.29% month over month at 0.62% share) and Concentrates surge (+2084.42% year over year at 4.63% share) as test beds for incremental penetration rather than core pillars.

Competitive Landscape

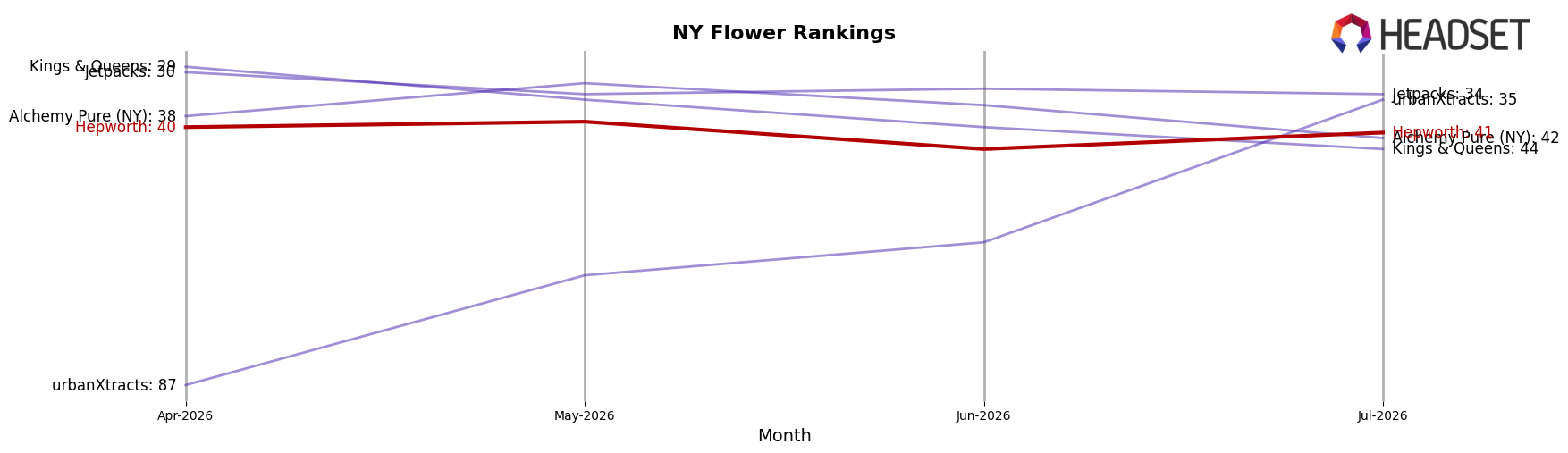

Hepworth sits at rank #41 in NY Flower for July 2026, down 21 positions year over year from #20, and 1 spot lower than April 2026’s #40, while its prior peak was #10 in July 2024. Against that slide, Find. rose from #8 to #1 with a 46.7% YoY sales increase, and Grassroots moved from #15 to #5 alongside 79.8% YoY sales growth, indicating share is consolidating at the top as Hepworth cedes rank; the pattern implies Hepworth’s trajectory is one of continued relative decline unless it reverses share losses that have widened between April 2026 and July 2026.

Notable Products

Mango Dog x White Runtz (3.5g) posted the steepest decline in July 2026 at -46.5% MoM while sliding to rank 2, and Durban Poison x Cherry Tart (3.5g) also contracted by -33.0% at rank 3; this tandem drop contrasts with Super Sour Diesel Sauce Cartridge (1g) at rank 1 falling a lesser -12.0%, implying a product mix pivot away from formerly higher-velocity Flower SKUs. With four of the top ten in Flower, the category’s concentration is paired with stress as Kush Mintz x Gelato 41 (3.5g) fell -42.4% at rank 8 and Skunk #1 (3.5g) held rank 5 without a reported MoM rate, suggesting demand is consolidating into fewer winners rather than lifting the whole segment. Vapor Pens show relative stability as Do Si Do Distillate Cartridge (1g) declined -15.3% at rank 6 against the category leader’s -12.0% at rank 1, while Original Z Distillate Cartridge (0.5g) held rank 7 without a MoM figure, indicating cartridges are eroding slower than Flower in July 2026. Overall, the pattern points to Hepworth reallocating emphasis toward Vapor Pens and selective Flower survivors to protect rank leadership and stabilize month-to-month volatility.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.