Market Insights Snapshot

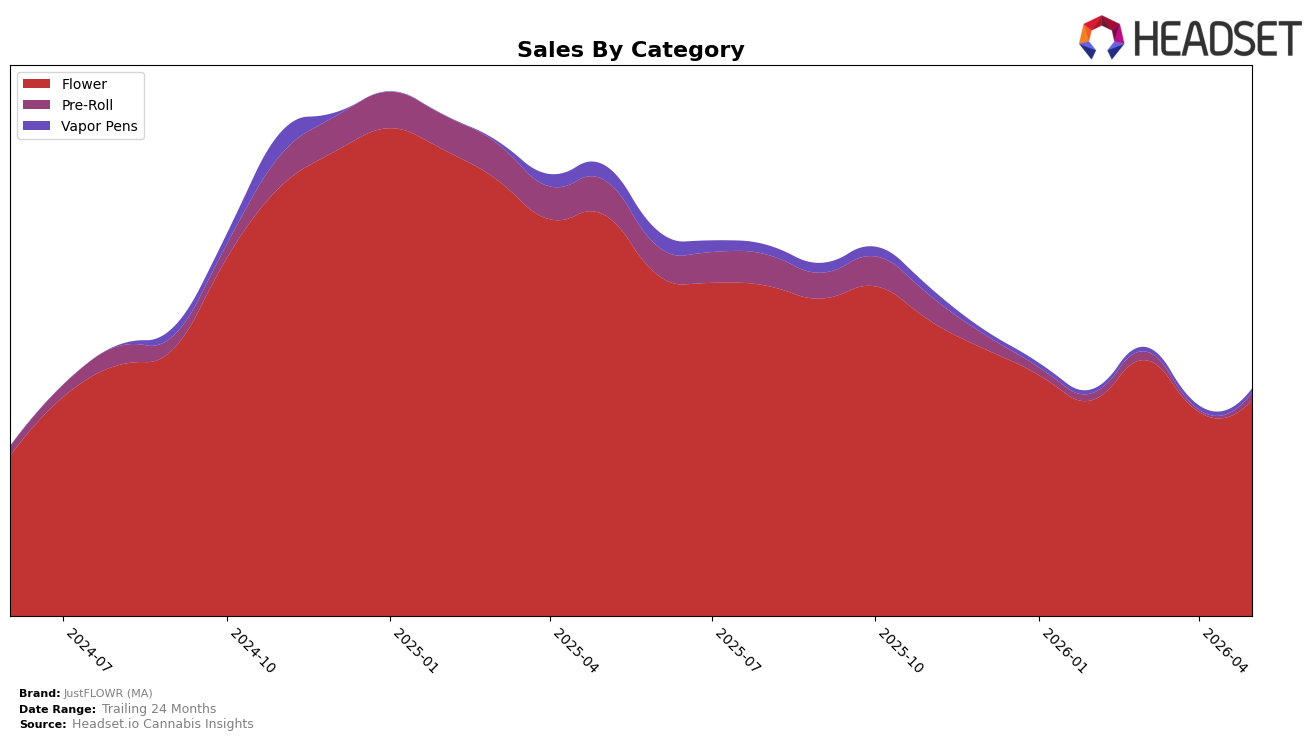

In May 2026, Flower concentrated 95.14% share for JustFLOWR (MA), with category sales down 46.33% year over year but up 5.66% month over month, while Pre-Roll held 3.25% share with a 78.63% year-over-year decline and a 301.50% month-over-month surge. Vapor Pens represented 1.61% share with a 74.86% year-over-year drop and an 8.13% month-over-month decline, and the brand’s average price rose 18.20% year over year as Flower’s average price sat at $27.54. The pattern implies a deliberate pullback to a Flower-led mix paired with selective Pre-Roll reactivation, while Vapor Pens remain deprioritized.

These shifts point to a positioning anchored in Flower leadership—reinforced by a category rank of 1 in Arizona—using Pre-Roll volatility (301.50% month-over-month on 3.25% share) as a tactical trial rather than a core pillar, and accepting a smaller, 1.61% Vapor Pens presence. With brand sales down 49.72% year over year but up 26.96% on a 24‑month basis, the mix suggests prioritizing margin via an 18.20% year-over-year price elevation and defending Flower share over breadth, implying the brand is trading short-term volume for category authority and price integrity.

Competitive Landscape

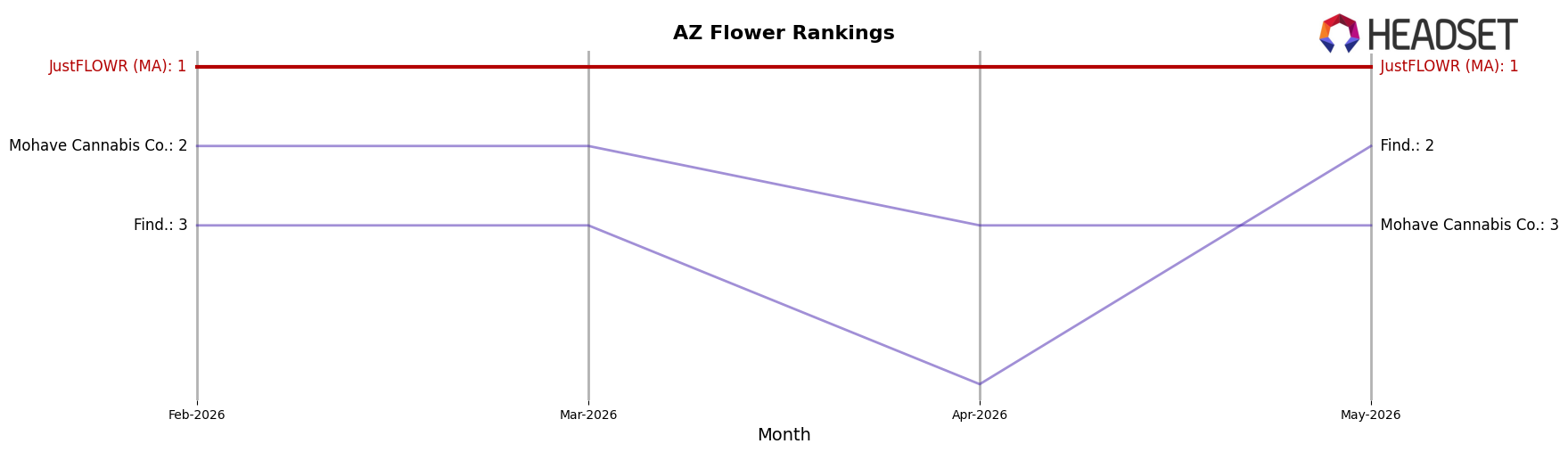

JustFLOWR (MA) sits at rank #1 in AZ Flower in May 2026 and is unchanged YoY from #1, while holding #1 over the last 3 months and marking its peak at #1 in May 2026; in contrast, Find. remains at #2 with a -25.3% YoY sales decline and Mohave Cannabis Co. holds #3 with a -5.9% YoY drop, indicating the distance between the leader and immediate followers widened. Further down, Just Flower / Just Vape surged from #51 to #4 with +2,749.9% YoY sales growth and Brown Bag improved from #14 to #5 with +142.9% YoY sales, creating pressure from fast risers even as the #2 and #3 positions deteriorate; the pattern implies JustFLOWR (MA)’s flat #1-to-#1 trajectory is durable against incumbent slippage but must anticipate volatility from accelerating challengers.

Notable Products

Jon Woo (14g) delivered the standout movement with an 81.5% month-over-month surge to rank 1 in May 2026, while Ice Cream Cake #3 (3.5g) slid 18.2% to rank 10, creating a widening gap at both ends of the chart. White RTZ (14g) also accelerated by 54.0% to rank 3, and with Flower SKUs occupying nine of the top ten positions, the assortment is consolidating around higher-weight Flower formats. The mix suggests JustFLOWR (MA) is concentrating demand into a few 14g winners at the top while allowing underperforming 3.5g entries to cycle down, indicating a tilt toward value-weight dominance and fewer small-pack bets.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.