Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

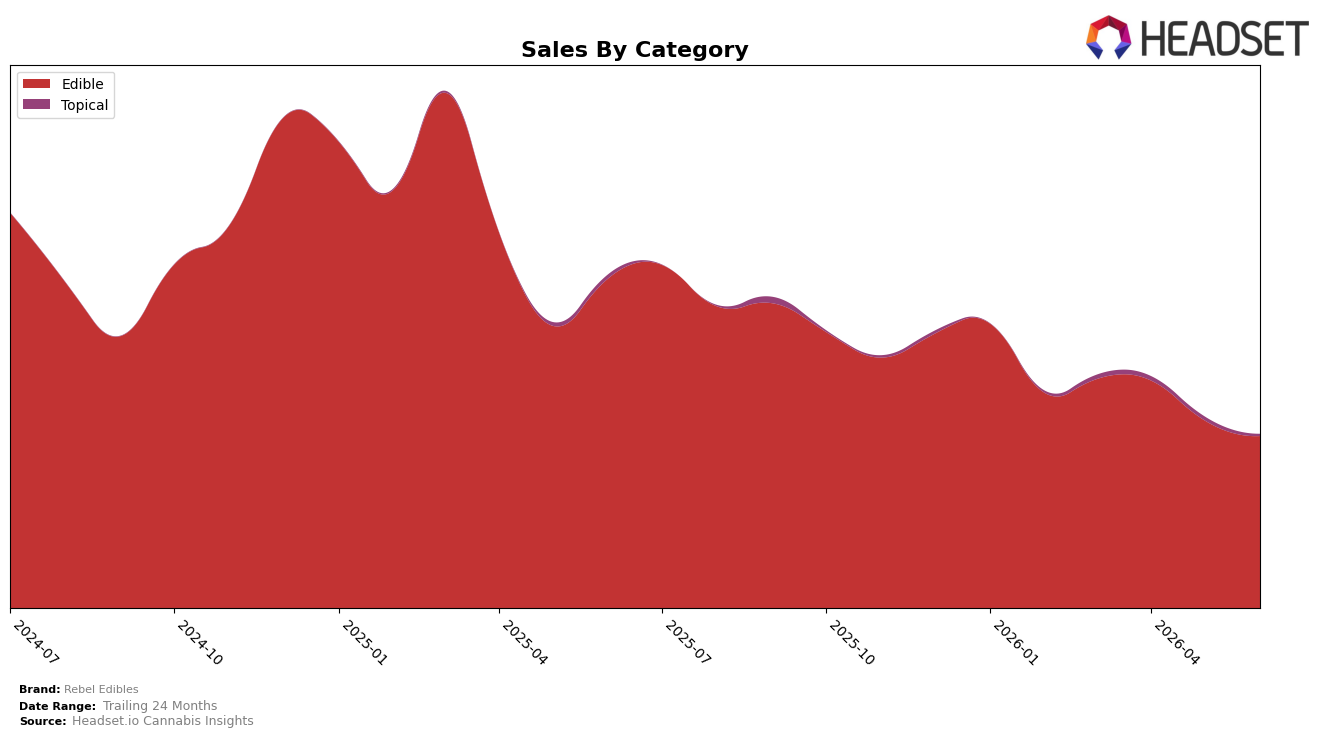

In June 2026, Rebel Edibles concentrated 98.97% of sales in Edible, with Topical at 1.03%, indicating an even tighter mix than typical multi-category peers. Edible declined 47.90% year over year and 8.35% month over month, while the much smaller Topical fell 52.19% year over year and 49.65% month over month, amplifying dependence on the core category. Average price rose 5.88% year over year to $11.79 alongside a 47.95% brand-level sales contraction and a June 2026 rank of 19 in Edible in Colorado, implying the brand is leaning on price while volume recedes and rank sits in the lower teens.

The mix shift toward Edible at 98.97% coupled with a 49.65% month-over-month drop in Topical and an 8.35% month-over-month decline in Edible implies portfolio concentration is increasing as secondary formats underperform. With year-over-year sales down 47.95% and average price up 5.88%, the positioning skews toward maintaining price integrity over promotional depth, which likely elevates elasticity risk and constrains share recovery in rank position 19 within Colorado Edible. The combination of a 52.19% Topical year-over-year decline against a 47.90% Edible year-over-year decline suggests resource allocation should prioritize defending Edible velocities rather than propping up Topical, as the current trajectory points to further rank pressure if volume doesn’t stabilize.

Competitive Landscape

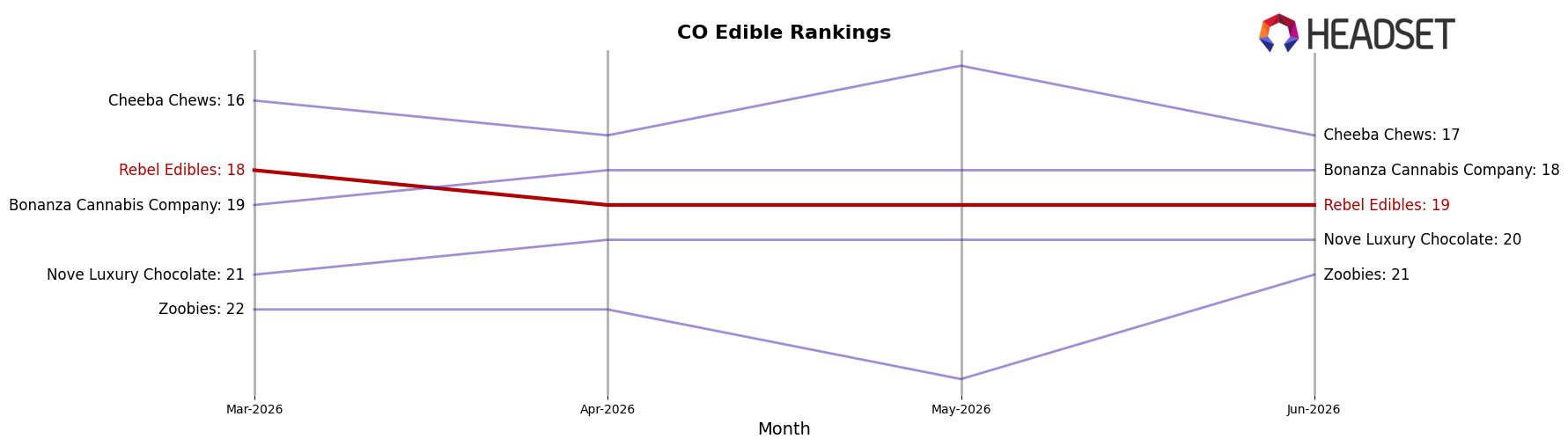

Rebel Edibles sits at rank #19 in CO Edible in June 2026, slipping 3 positions year over year from #16 while edging down 1 place versus March 2026’s #18; against a longer arc, it remains 8 spots below its January 2025 peak at #11 and 18 positions behind Wyld at #1, even as Wyld’s sales declined 16.6% year over year and Good Tide held #5 despite a 25.5% year-over-year drop, indicating Rebel’s rank erosion is more about share loss than category contraction and implying that, without a near-term mix or pricing pivot, the trajectory points to continued mid-pack drift rather than re-entry into the top 15.

Notable Products

Rozzies - Orange Pineapple Pebble Coated Rosin Fruit Chews 10-Pack (100mg) posted the steepest move in June 2026 with a -54.99% MoM drop while sitting at rank 9, and Rozzies - Mixed Berry Live Rosin Chews 10-Pack (100mg) fell -53.87% at rank 8, indicating concentrated weakness in rosin chews despite broader category stability. Indica Blue Raspberry Pebbles Gummies 10-Pack (100mg) remained at rank 1 but contracted -21.51% MoM, whereas Sativa Strawberry Orange Pebble Bites Gummies 10-Pack (100mg) surged +60.78% to rank 2, suggesting a shift in demand from indica-leading pebbles toward sativa-forward fruit profiles. Four of the top ten SKUs are Rozzies-branded rosin chews with three logging MoM declines between -5.18% and -54.99%, while the mixed Hybrid Strawberry, Green Apple, Blue Raspberry, and Mango Coated Gummies 10-Pack (100mg) held rank 3 on a flat +0.28% MoM and CBD/CBN/THC 1:1:2 Sweet Dreams Honey Lavender Caramels 20-Pack (50mg CBD, 50mg CBN, 100mg THC) at rank 4 grew +7.45%, implying consumer preference is consolidating around classic sugar-coated gummies and functional nighttime sets rather than premium rosin formats. With only $23,597 tied to the leading SKU and multiple mid-pack declines of -17.65% and -35.44%, the mix points to a portfolio reweighting opportunity toward sativa and functional caramels while rationalizing underperforming rosin variants.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.