Market Insights Snapshot

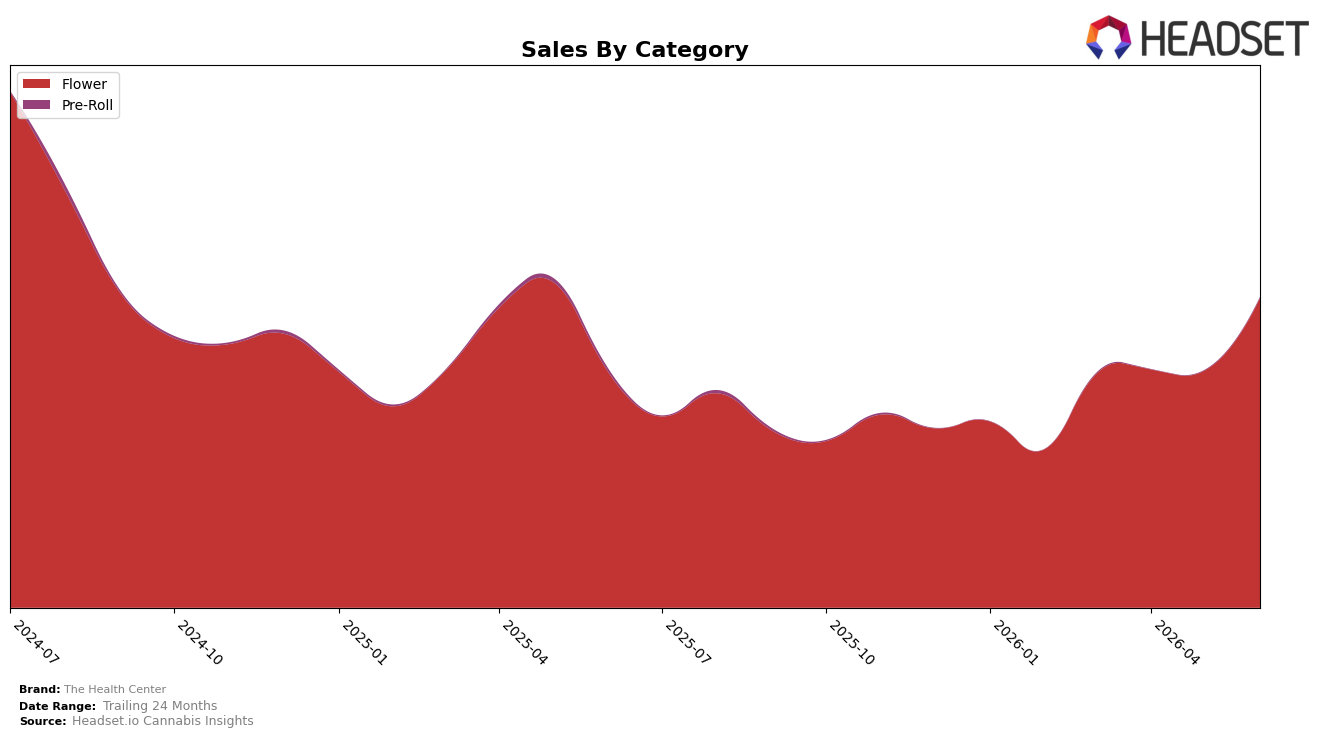

The Health Center concentrated 99.75% of June 2026 sales in Flower, with Flower up 31.44% year over year and 30.61% month over month, while Pre-Roll held 0.25% share with a -76.04% year-over-year change but a 157.50% month-over-month rebound. Average price rose 3.97% year over year to $17.04, as Flower averaged $17.06 and Pre-Roll averaged $11.87, and the Flower rank in Colorado sat at 20. The pattern implies a single-category dependency where short-term momentum in Flower and a tactical Pre-Roll bounce coexist with long-term mix risk if the Pre-Roll contraction persists.

With overall brand sales up 30.00% year over year but down 35.53% versus 24 months, the 31.44% Flower lift and rank 20 in Colorado indicate gains tied to Flower depth rather than diversified demand, while the 157.50% Pre-Roll month-over-month jump from a 0.25% base signals limited spillover potential. The combination of a 3.97% price increase and a 30.61% month-over-month Flower surge suggests current velocity is volume-led with manageable pricing, implying positioning as a Flower specialist where sustaining share likely relies more on maintaining product breadth within Flower than on cross-category expansion.

Competitive Landscape

The Health Center sits at rank #20 in Colorado Flower for June 2026, improving 6 positions from #26 year over year, and climbing 10 spots from #30 over the last three months, yet it remains below its peak of #9 in July 2024. Against this backdrop, Seed & Strain Cannabis Co. moved up from #2 to #1 while growing sales by 62.8%, and Natty Rems surged from #28 to #5 with 221.0% YoY sales growth, indicating that share is consolidating at the top as faster risers compress mid-tier mobility; the trajectory implies The Health Center’s recent rank gains are real but risk stalling unless it accelerates relative to leaders capturing outsized momentum.

Notable Products

Honeymoon Diesel (7g) posted the largest month-over-month surge at 92.5% to rank 2 in June 2026, while Strawberry Nightmare Popcorn (7g) fell 51.9% to rank 7, indicating a sharp reallocation of demand within adjacent strains. Chem Lemons Popcorn (7g) also advanced 54.6% to rank 5 as Strawberry Nightmare (7g) rose 27.0% to rank 3, and six of the top ten are Popcorn Flower SKUs, pointing to a pack-size and value-led tilt that is reshaping the leaderboard. The #1 Honeymoon Diesel Popcorn (7g) held its position as the top SKU on $74,708 while Durban Poison (7g) was essentially flat at +0.5% at rank 8, suggesting stability at the long tail as momentum concentrates at the top. Together these moves imply The Health Center is consolidating share around higher-velocity Diesel and value-oriented Popcorn variants, signaling an assortment strategy geared toward volume retention over breadth.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.