Market Insights Snapshot

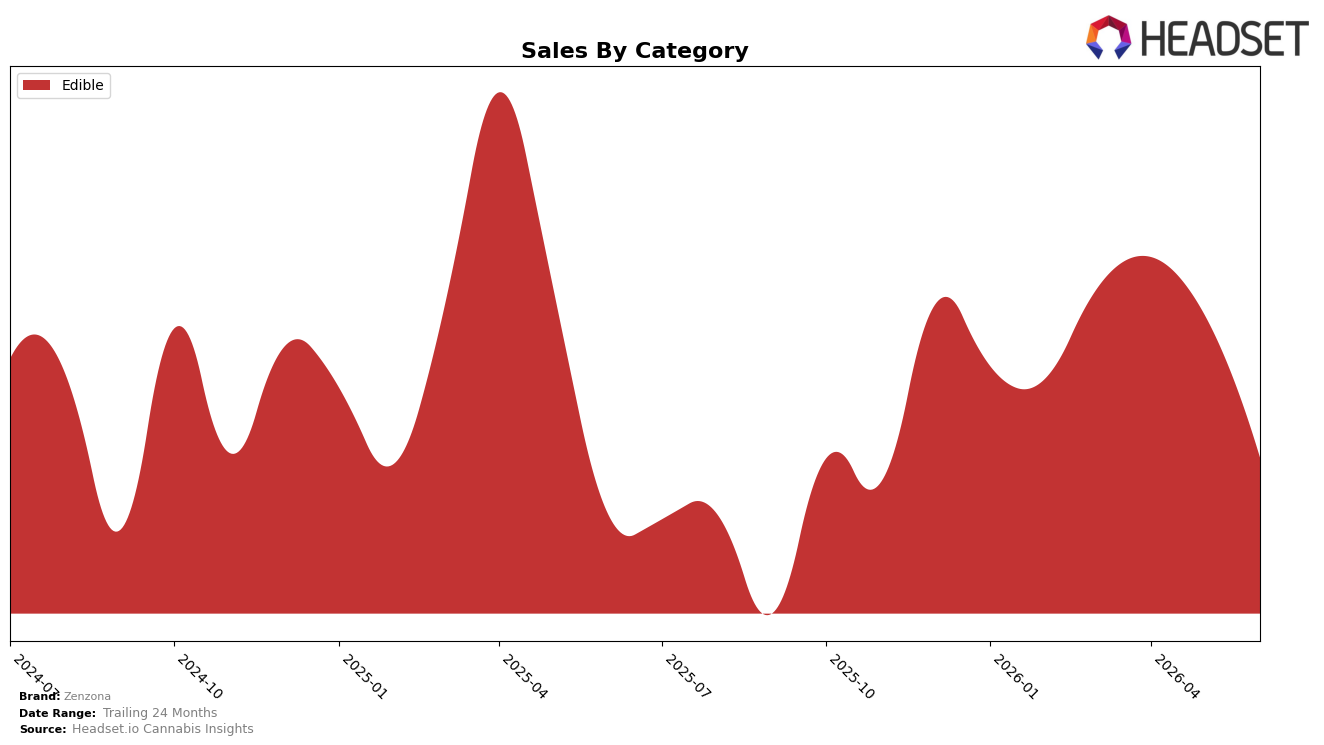

In June 2026, Zenzona operated as a single-category brand with Edible accounting for 100.0% of sales, posting 5.95% year-over-year growth alongside a -12.34% month-over-month decline. Average price rose 13.64% YoY to $9.16 while brand sales over 24 months were down -14.46%, indicating mix stability but volume sensitivity within Edible. With a state-category rank of 15 in Arizona Edible, the combination of positive YoY sales at 5.95% and a double-digit MoM pullback at -12.34% implies demand is concentrated in repeatable occasions but vulnerable to short-cycle fluctuations, and that pricing at +13.64% YoY is carrying revenue more than units.

The consolidation into 100.0% Edible and a rank of 15 in Arizona suggest Zenzona is positioned as a focused player whose pricing power (+13.64% YoY) supports value capture during slower unit turns (-12.34% MoM) while maintaining annual momentum (+5.95% YoY). This pattern implies the path to improving rank from 15 hinges on stabilizing month-to-month variability in Edible while preserving the price lift, because the divergence between +5.95% YoY sales and -14.46% over 24 months indicates recent traction that could slip if MoM softness persists.

Competitive Landscape

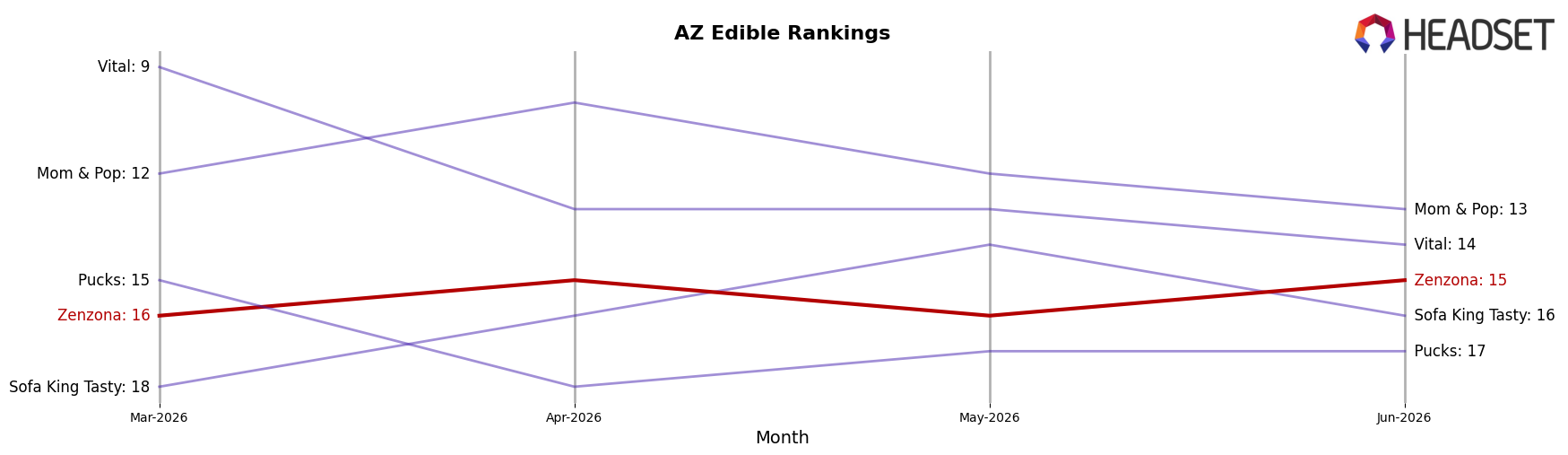

Zenzona sits at rank #15 in June 2026 in AZ Edible, slipping 1 spot year over year from #14 while improving 1 position from #16 over the last three months; against this middle-tier stability, Baked Bros climbed from #4 to #3 with a 30.9% YoY sales increase and Gron / Grön eased from #3 to #4 despite a 7.6% YoY gain, indicating share is consolidating near the top as Zenzona remains 3 ranks below its April 2025 peak of #12; this trajectory implies Zenzona’s path back into the top 12 will require outpacing at least 2–3 competitors whose upward rank changes and double-digit growth rates are compressing available ladder space.

Notable Products

Indica Watermelon Vegan Gummies 10-Pack (100mg) posted the steepest decline at -23.6% MoM while sliding to rank 7, and Italian Zorbet RSO Vegan Gummies 10-Pack (100mg) fell -14.9% at rank 2. Pineberry Vegan RSO Gummies 10-Pack (100mg) held rank 1 despite an -8.7% MoM dip, indicating leadership is coming from a shrinking top SKU rather than a rising challenger. With eight of the top ten SKUs in June 2026 concentrated in Edible gummies, the pattern implies Zenzona is over-indexed in a single format, leaving growth contingent on stabilizing declines in core fruit profiles rather than diversification.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.