Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

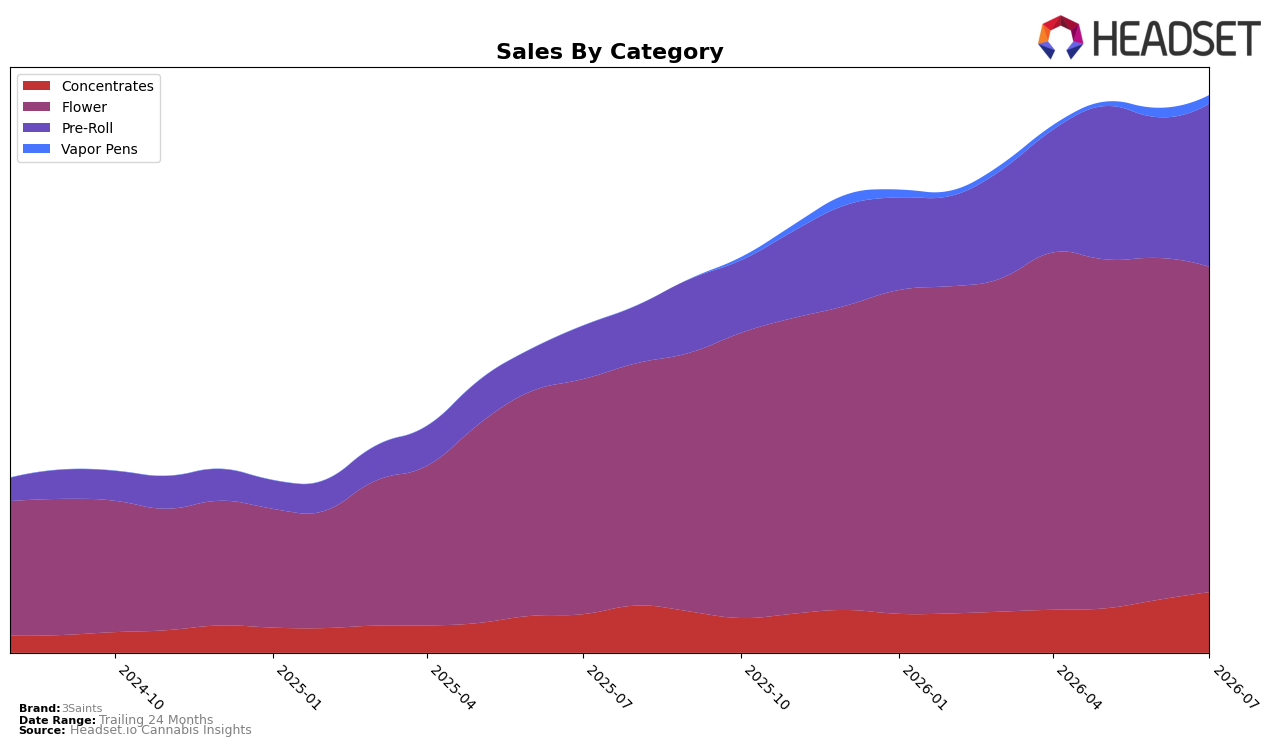

In July 2026, 3Saints concentrated 58.38% of sales in Flower with year-over-year growth of 38.38% but a month-over-month decline of 4.87%, while Pre-Roll expanded to 29.28% share on 207.23% YoY and 16.04% MoM gains. Concentrates reached 10.85% share with 57.37% YoY and 14.73% MoM growth, whereas Vapor Pens held 1.49% share with an 8.66% MoM decline and no YoY basis. With average price up 15.69% YoY to $22.82 alongside a Flower rank of 8 in Ontario, the pattern implies a deliberate tilt toward accessible, faster-turn formats (Pre-Roll, Concentrates) to offset Flower’s MoM softness while maintaining core scale.

The mix shift—Pre-Roll adding share at 29.28% amid 16.04% MoM growth and Concentrates rising 14.73% MoM—suggests portfolio headroom outside Flower even as Flower, at 58.38% share, anchors the brand with an 8th-place category rank in Ontario. With overall brand sales up 70.61% YoY and 221.98% over 24 months, plus price up 15.69% YoY, the implication is pricing power sustained by non-Flower velocity: leaning further into Pre-Roll and Concentrates can compound share without overexposing the brand to Flower’s 4.87% MoM contraction.

Competitive Landscape

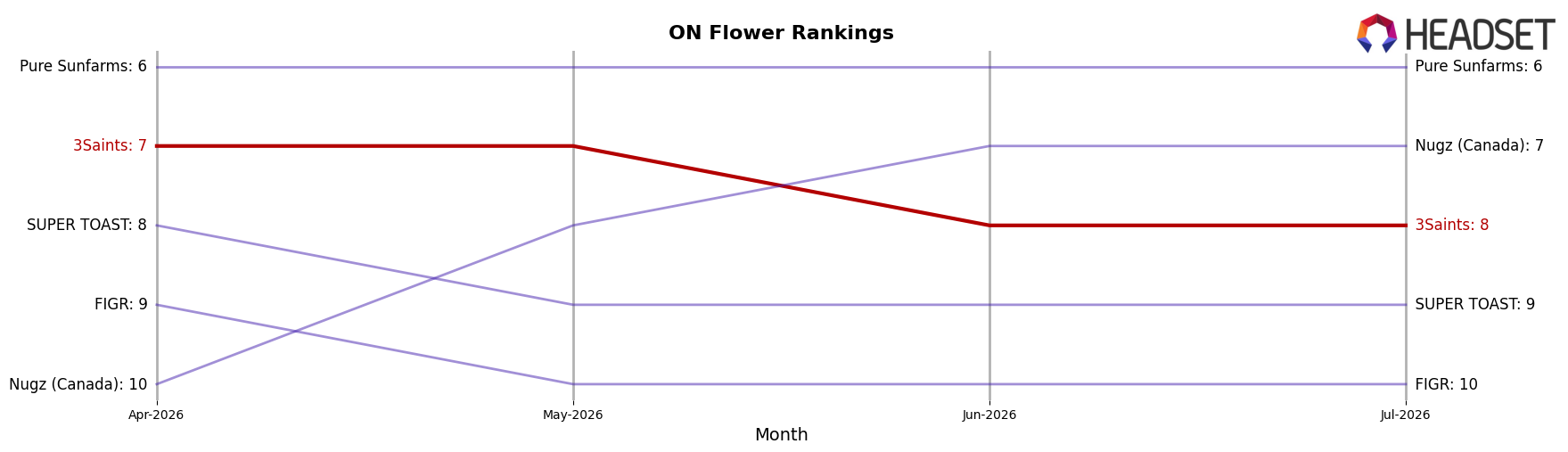

3Saints sits at rank #8 in ON Flower in July 2026, up 3 positions from #11 year over year but down 1 place from #7 in April 2026 to July 2026, indicating a modest retreat from its peak in May 2026 at #7; meanwhile, Shred held #1 while improving from #2 year over year and growing sales by 17.2%, and Spinach climbed from #4 to #2 with a 31.1% YoY sales increase, widening the gap over mid-pack brands as Back Forty / Back 40 Cannabis slipped from #1 to #4 with a 5.4% sales decline; this pattern implies 3Saints’ rank trajectory is stabilizing in the upper-mid tier, requiring share capture from #7–#4 to reattain momentum while leaders consolidate gains.

Notable Products

Kush Cookies (1g) posted the steepest decline in July 2026, down 17.3% MoM while sitting at rank 10, whereas Kush Cookies (3.5g) slid 6.5% MoM but held rank 1. In contrast, Black Afghan Hash (2g) at rank 4 grew 14.2% MoM and the Kush Cookies (14g) format at rank 8 inched up 2.5% MoM, indicating demand migrating toward larger Flower sizes and value Concentrates rather than the smallest Flower pack.

Pre-Rolls accounted for four of the top ten in July 2026, with growth clustered between 4.7% and 13.4% MoM across ranks 2, 3, 5, and 6, while the leading Flower SKU at rank 1 declined 6.5% MoM. With rank 2 up 13.4% MoM and rank 3 up 5.5% MoM alongside a Concentrates gain of 14.2% at rank 4, the mix implies momentum toward repeatable, sessionable formats and hash-led trade-ups at the expense of single-gram Flower.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.