Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

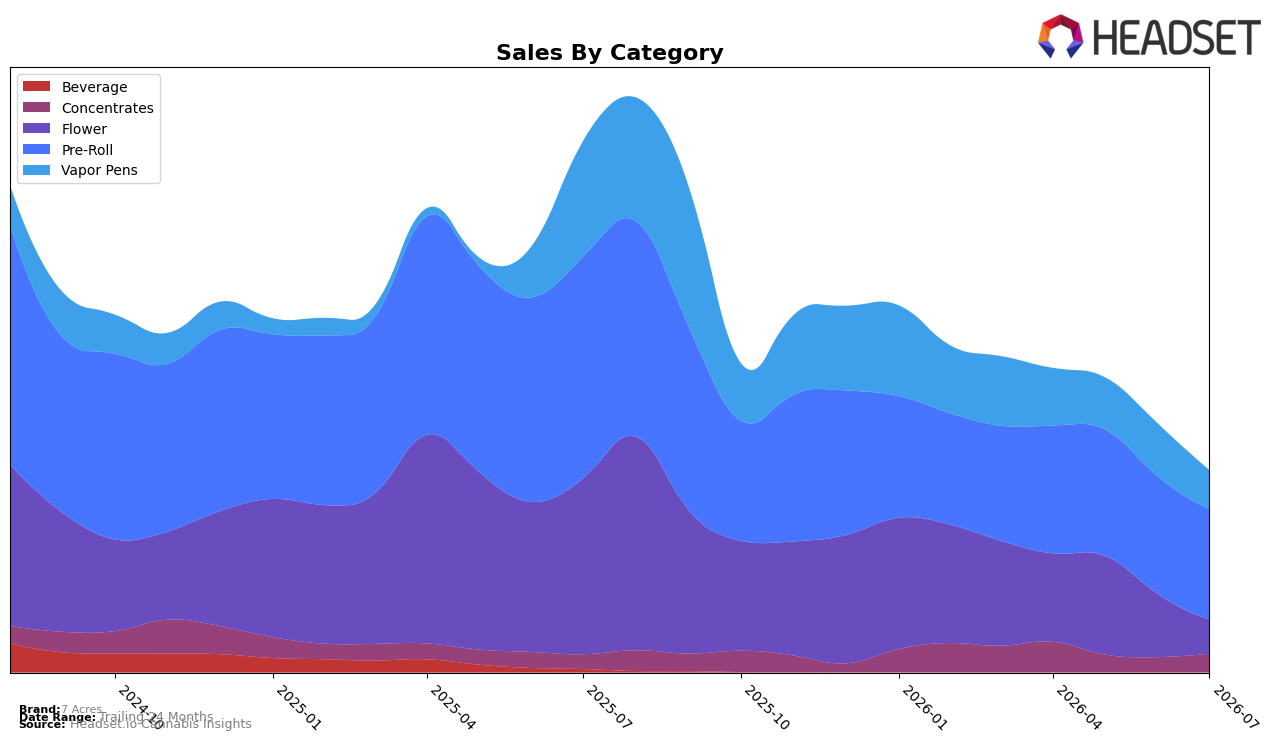

In July 2026, 7 Acres concentrated 55.01% of sales in Pre-Roll, where year-over-year declined 49.94% and month-over-month slipped 5.43%, while Vapor Pens held 18.94% share with a 66.96% YoY drop and a 27.64% MoM decline. Flower accounted for 16.86% share but contracted 80.71% YoY and 46.13% MoM, whereas Concentrates rose 26.45% YoY and 22.94% MoM to 9.17% share; Beverage was negligible at 0.03% share with a 98.38% YoY fall. With the brand’s average price down 29.49% YoY and Pre-Roll ranked 56 in British Columbia, the pattern implies a pivot away from legacy Flower and Vapor Pens toward stabilizing volume in Pre-Roll and emergent growth in Concentrates to preserve share.

The mix shift—Pre-Roll at 55.01% alongside Concentrates growing 26.45% YoY and 22.94% MoM—signals a need to lean into lower-ticket, higher-velocity formats while using Concentrates as a margin counterweight to a 29.49% YoY price compression. Given Flower’s 80.71% YoY and 46.13% MoM declines and Vapor Pens’ 66.96% YoY and 27.64% MoM declines, maintaining Pre-Roll scale while laddering shoppers into Concentrates provides a defensible route to improve category rank from 56 in British Columbia by converting at-risk Flower and Vapor Pen customers rather than chasing shrinking segments.

Competitive Landscape

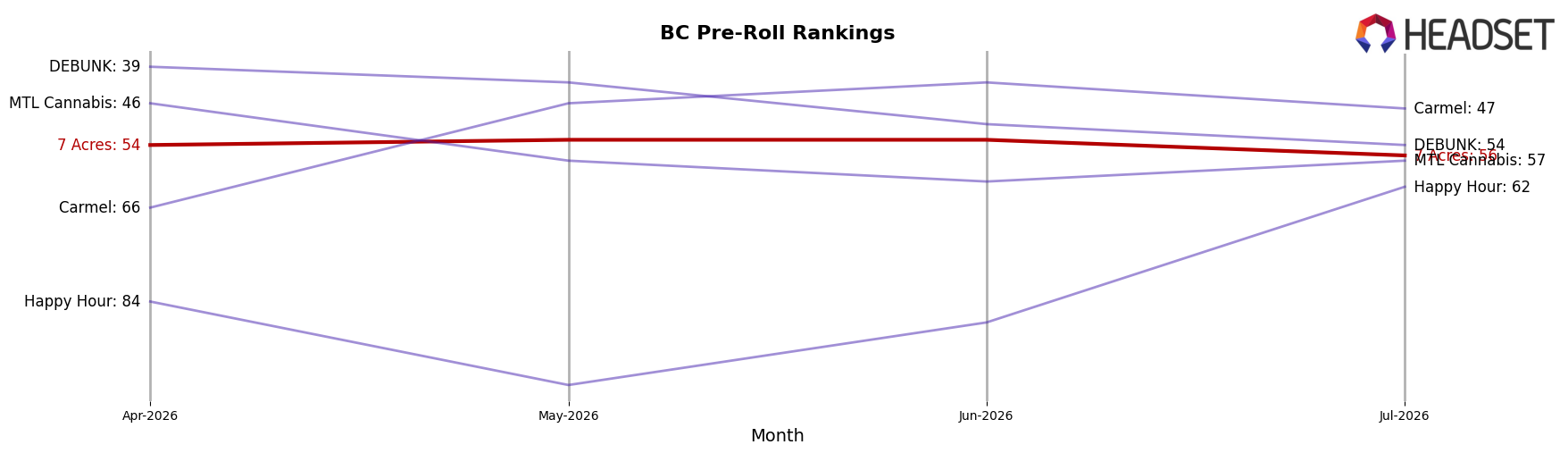

7 Acres sits at rank #56 in BC Pre-Roll in July 2026, down 11 positions year over year from #45 and slipping 2 spots from #54 over the last three months, while the brand’s historical peak of #19 in July 2024 underscores the depth of the pullback. In contrast, Back Forty / Back 40 Cannabis climbed from #17 to #2 with a 215.25% YoY sales increase, and General Admission held #1 despite a 22.34% YoY sales decline, indicating that market share is consolidating at the top even as leaders see contraction. This divergence—declining rank for 7 Acres alongside upward mobility for faster-growing peers—implies that without a mix refresh or channel reallocation, the rank trajectory points to continued share erosion against top-tier incumbents and fast risers.

Notable Products

Ultra Jack Pre-Roll 2-Pack (1g) posted the steepest decline in July 2026 at -76.4% MoM, sliding to rank 9, while Jack Haze Pre-Roll 2-Pack (1g) held rank 1 with a -1.4% MoM dip and approximately $209,668 in sales. Cafe Dublin Delight Live Resin (1g) delivered the largest MoM gain at +75.9%, reaching rank 3, as Blue Dream Live Resin Liquid Diamonds Disposable (0.95g) fell -29.8% to rank 2. Three of the top ten are Pre-Roll SKUs, but with one anchor at rank 1 and two steep drops at ranks 9 and 10 (-76.4% and -50.0%), the mix points to volatility in legacy pre-rolls while momentum shifts toward premium extracts. The pattern implies 7 Acres is leaning into higher-velocity concentrates to offset weakening tails in smaller pre-roll formats.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.