Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

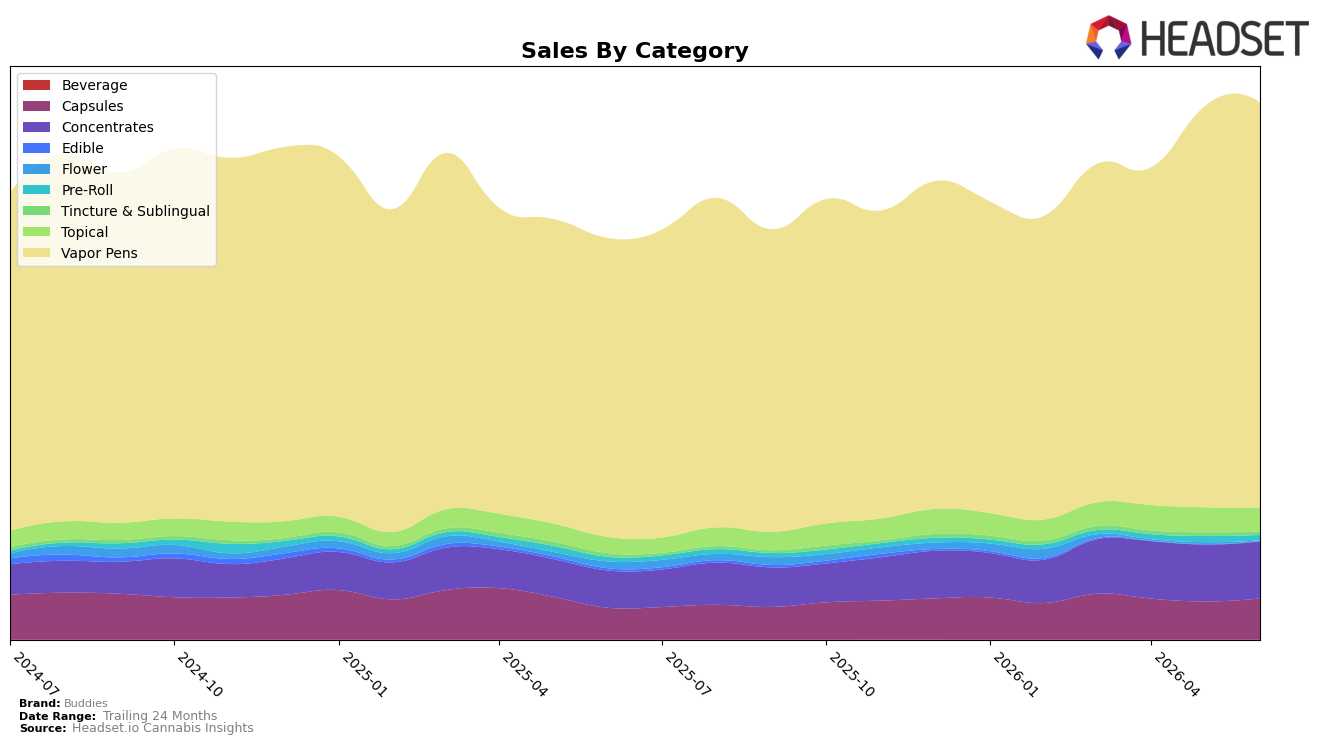

Buddies in June 2026 concentrated 75.80% of sales in Vapor Pens with year-over-year growth of 35.58% and month-over-month growth of 1.05%, while Concentrates held 10.61% share with 53.48% YoY and 0.18% MoM growth. Capsules expanded to 7.64% share with 29.83% YoY and 7.90% MoM, whereas Topical reached 4.46% share on 50.61% YoY but fell −3.28% MoM. Peripheral categories contracted: Pre-Roll at 0.92% share declined −15.08% MoM despite 17.44% YoY, Tincture & Sublingual at 0.51% dropped −16.71% MoM and −15.58% YoY, and Flower and Edible collapsed to 0.05% and 0.004% share with −95.45% and −98.93% YoY respectively (−79.36% and −74.50% MoM). With brand sales up 34.04% YoY and average price up 5.12% to $19.77, the mix shift indicates Buddies is concentrating volume in high-velocity inhalables while intentionally exiting low-share formats.

The category pattern implies Buddies is reinforcing a Vapor Pens-led identity while using Capsules and Concentrates as secondary growth levers, as evidenced by Capsules’ 7.90% MoM against Vapor Pens’ 1.05% and Concentrates’ 53.48% YoY against Topical’s 50.61% YoY. The near-elimination of Flower (−95.45% YoY) and Edible (−98.93% YoY) alongside Pre-Roll’s −15.08% MoM suggests portfolio pruning to reduce operational drag, which supports price stability as Vapor Pens’ $21.07 average anchors mix above the $11.66 Concentrates average. Given Oregon leadership in Vapor Pens at rank 1 and the 10.61% Concentrates share, the positioning signals focus on inhalable convenience with selective retention of wellness-adjacent forms (Capsules, Topical), implying resource allocation should prioritize pen innovation and targeted capsule placement over re-entry into low-yield combustibles.

Competitive Landscape

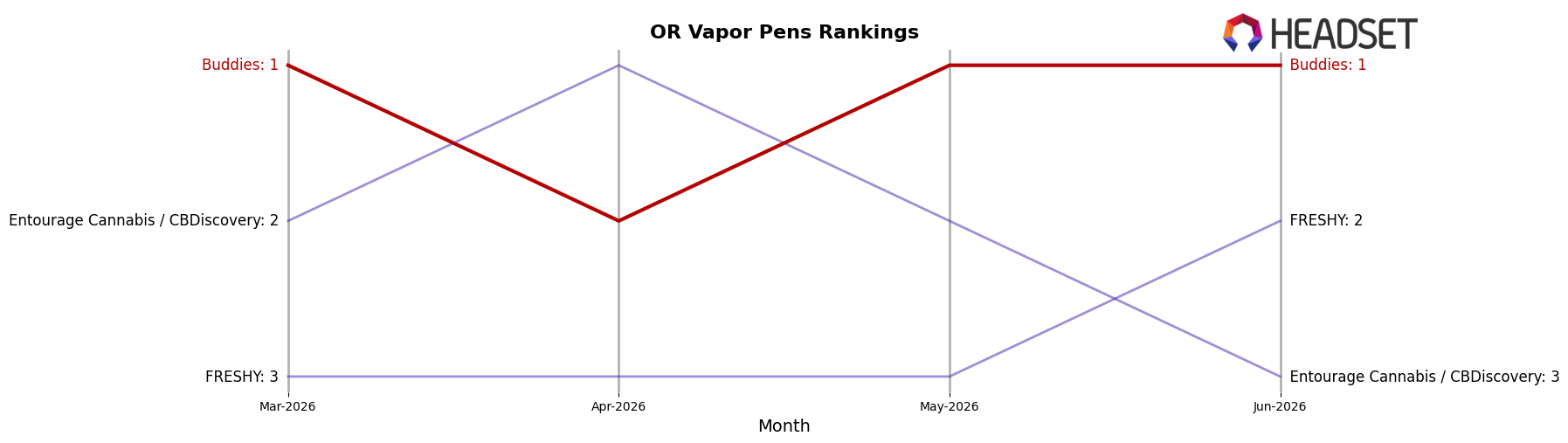

Buddies is ranked #1 in OR Vapor Pens in June 2026, improving 1 position from #2 year over year, and holding #1 since March-to-June with a 0-place change over the last three months; meanwhile, FRESHY climbed from #5 to #2 with an 81.5% YoY sales increase and Entourage Cannabis / CBDiscovery fell from #1 to #3 with a 38.9% YoY sales decline, creating a gap where Buddies’ stability at #1 contrasts with upward pressure from a faster-rising #2 and relief from a contracting former leader. With Hellavated inching from #3 to #4 despite a 1.2% YoY sales lift and Oregrown surging from #11 to #5 on 57.4% YoY growth, the pattern implies Buddies’ top rank is secure near term but will require defending against high-velocity chasers rather than the prior incumbent.

Notable Products

Tropical Blast Flavors Distillate Cartridge (1g) delivered the standout move in June 2026 with a 91.9% month-over-month surge to rank 1, while Grape Ape Distillate Cartridge (1g) fell 30.0% to rank 8, signaling a sharp bifurcation in flavor momentum. Blue Ox Distillate Cartridge (1g) rose 12.6% to rank 2 and Blueberry Muffin Distillate Cartridge (1g) gained 9.5% to rank 3, and six of the top ten are flavored distillate cartridges, indicating a concentration in sweet, familiar profiles. Despite Blueberry Muffin Palm Distillate Disposable (1g) holding rank 6 with a 9.1% lift and $90,797 in sales, the new Pink Lemonade Flavored Distillate Disposable (1g) entered at rank 10, pointing to expanding disposable interest alongside cartridge dominance. The pattern implies Buddies is consolidating leadership around flavor-driven cartridges while selectively seeding disposables, using flavor wins to offset underperforming legacy SKUs and tilt the mix toward higher-velocity formats.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.