Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

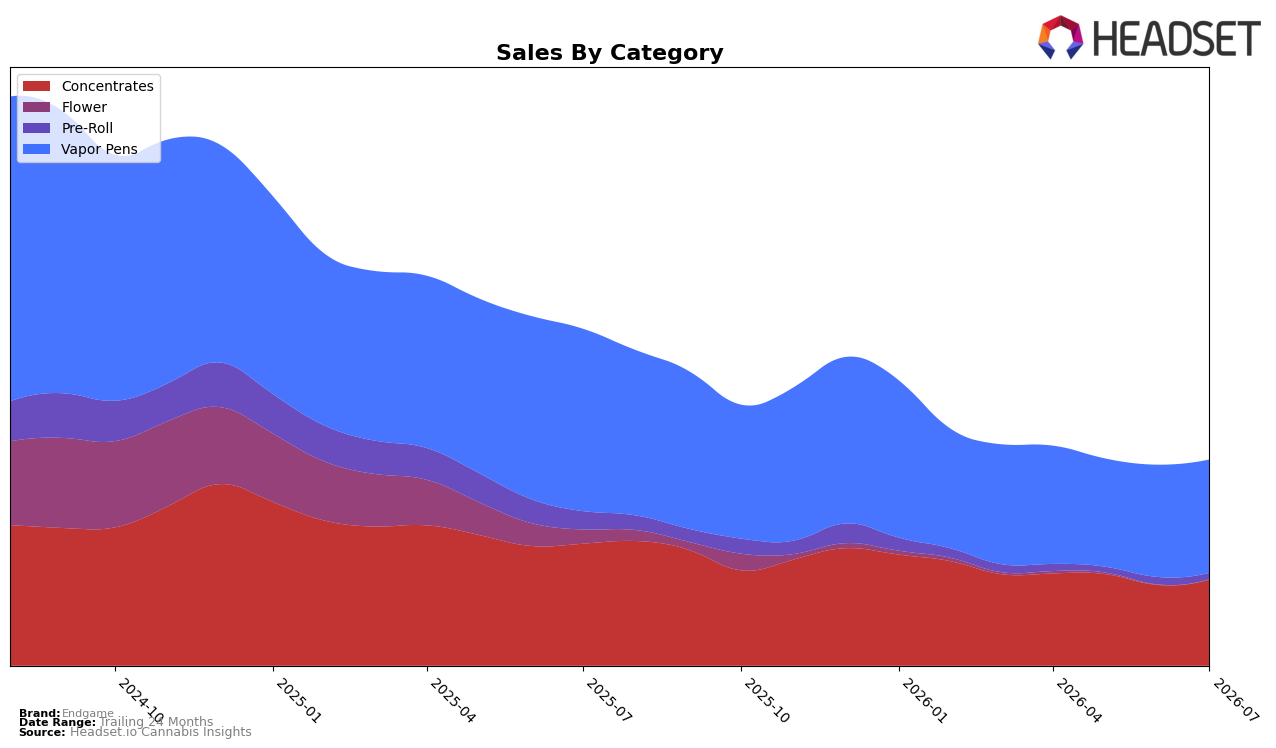

In July 2026, Endgame’s mix concentrated even further into Vapor Pens at 54.84% share (ranked 13 in Vapor Pens in Saskatchewan) with a marginal month-over-month lift of 0.90% despite a year-over-year decline of 37.82%, while Concentrates held 41.80% share with a 6.77% MoM increase against a 29.25% YoY drop. Smaller lines retreated: Pre-Roll fell 14.59% MoM and 64.81% YoY to 3.14% share, and Flower contracted 28.88% MoM and 96.91% YoY to 0.21% share. With brand sales down 38.71% YoY and the average price down 7.04% YoY, the pattern implies Endgame is consolidating demand into two inhalable formats—Vapor Pens and Concentrates—while exiting or deprioritizing Flower and Pre-Roll, trading breadth for depth within core categories.

The combined 1.80 percentage-point gap between Vapor Pens’ 0.90% MoM uptick and Pre-Roll’s 14.59% MoM decline, alongside Concentrates’ 6.77% MoM rise, implies a positioning that favors higher-frequency, device-based and dab-oriented use occasions over casual, shareable formats. Given Endgame’s average price at $27.61 and Vapor Pens’ category-specific average price of $29.59, the 7.04% YoY brand price decrease paired with a 37.82% YoY decline in Vapor Pens suggests elasticity is not restoring volume, so the intended positioning is less about price play and more about anchoring in the two categories where the brand still commands over 96.64% of mix.

Competitive Landscape

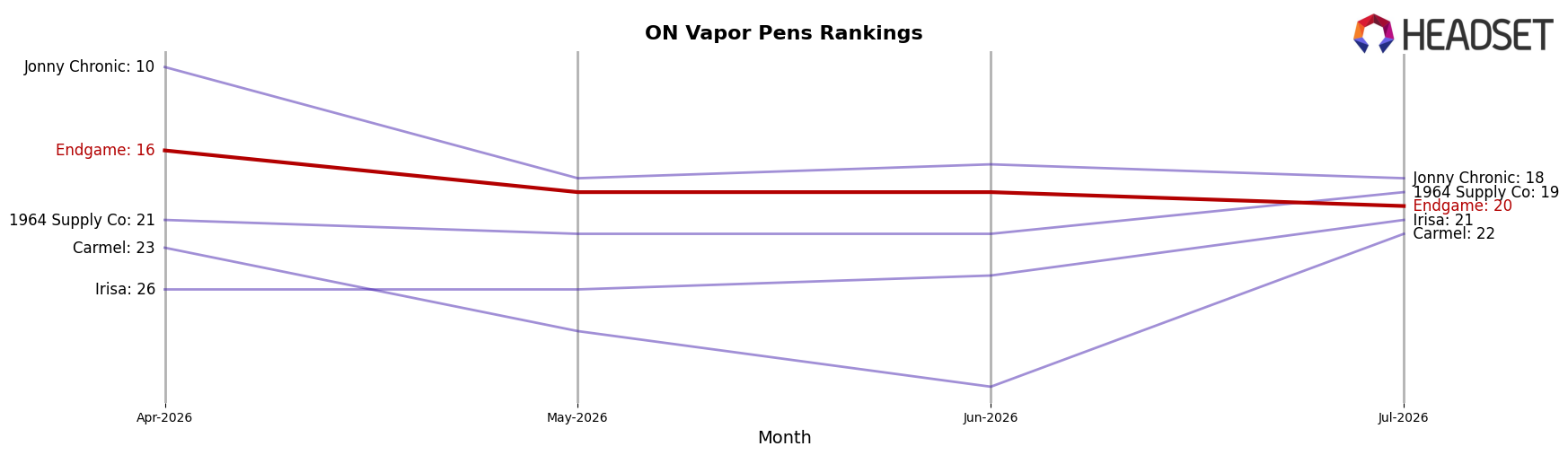

Endgame sits at rank #20 in ON Vapor Pens in July 2026, down 9 positions year over year from #11, and 4 spots below its April 2026 mark of #16, while still well off its peak of #6 from August 2024; meanwhile, Spinach climbed from #4 to #1 with 144.7% YoY sales growth and BoxHot advanced from #2 to #3 with 4.6% YoY growth, indicating Endgame’s relative share is compressing as leaders consolidate higher ranks. With Back Forty / Back 40 Cannabis moving from #1 to #2 and General Admission sliding from #3 to #4 alongside a -19.0% YoY sales change, Endgame’s 3-month rank slip of 4 positions and 9-position YoY drop signal a drift toward the category’s middle tier as faster-moving competitors expand their foothold.

Notable Products

Cheetah Stomper Shatter (1g) posted the steepest move in July 2026 with a -16.2% month-over-month drop at rank 8, contrasting with rank 1 Mimosa x Blood Orange Distillate Cartridge (1g) up 12.3% and rank 5 Pineapple OG Shatter (1g) up 23.9%. Vapor Pens hold ranks 1-2 and 4, while Concentrates occupy six of the top ten, indicating a split where pen leaders are steady but the broader list tilts toward extracts. The $263,516 taken by Mimosa x Blood Orange Distillate Cartridge (1g) at rank 1 alongside Astro Pink THCA Isolate (1g) up 41.2% at rank 7 signals mix volatility inside Concentrates even as top Vapor Pens consolidate share. The pattern implies Endgame’s commercial direction is leaning into a two-tier portfolio: stable flagships in Vapor Pens paired with opportunistic, higher-variance pushes in Concentrates to drive incremental growth and defend breadth.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.