Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

The Fresh Canna is stocked at 334 licensed dispensaries across Michigan, with the deepest coverage in New Buffalo, Detroit, Monroe, Grand Rapids, and Kalamazoo. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

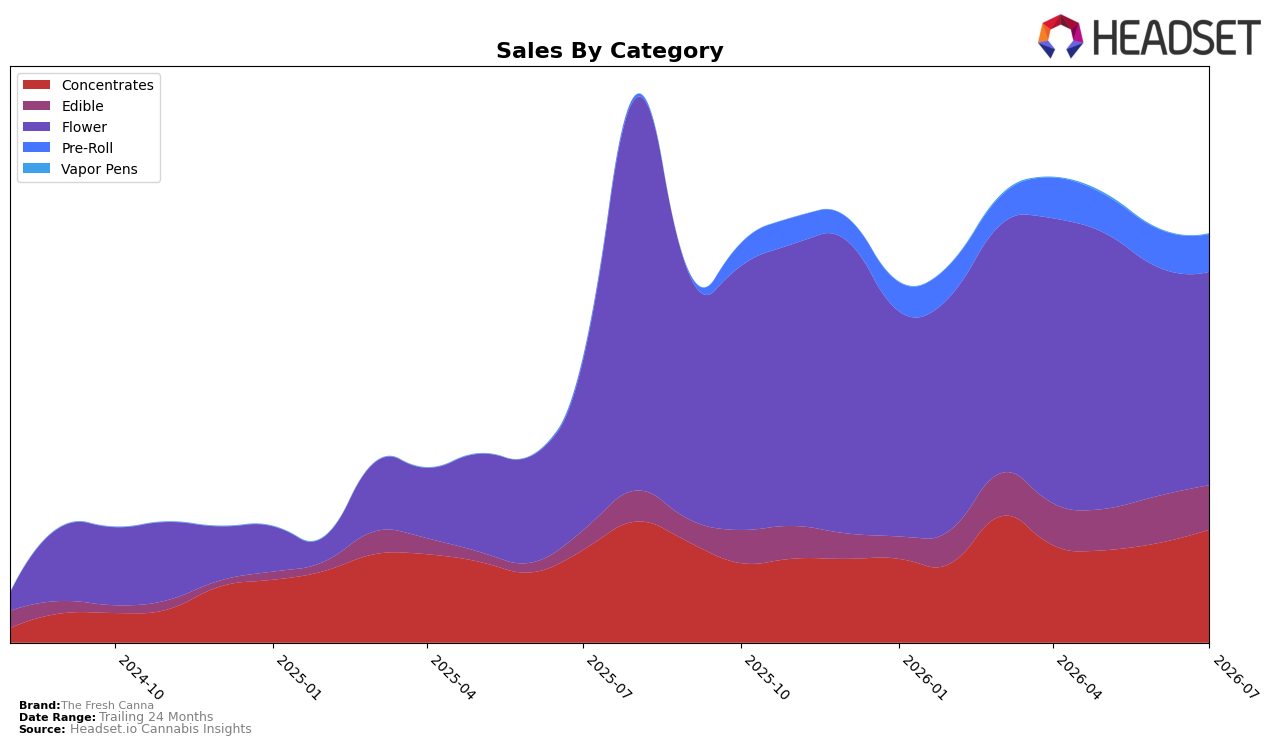

The Fresh Canna’s July 2026 mix leans on Flower at 52.23% share with 25.41% YoY growth but a -6.76% MoM dip, while Concentrates climbed to 27.66% share on 22.02% YoY and 13.64% MoM. Edible holds 10.78% share with 127.20% YoY but -5.89% MoM, and Pre-Roll sits at 9.19% share with 1132.11% YoY and -1.58% MoM; Vapor Pens remain marginal at 0.14% share with 7.01% MoM. With brand-level sales up 43.25% YoY and average price up 5.76% YoY, the pattern implies a pivot from a single-category engine toward a multi-pronged base where Concentrates and Pre-Roll provide incremental growth ballast as Flower softens month over month.

These shifts suggest a positioning tilt toward value-access and trial across inhalable formats: Flower’s -6.76% MoM against Concentrates’ 13.64% MoM points to substitution within inhalables, while Pre-Roll’s 1132.11% YoY alongside Edible’s 127.20% YoY indicates basket diversification rather than pure uptrade. In Michigan Flower, a rank of 24 combined with a 25.41% YoY in the lead category and 9.19% Pre-Roll share implies headroom to defend Flower while using faster-growing Pre-Roll and Concentrates to ladder into higher-velocity placements; the implication is a barbell strategy that maintains Flower scale as a traffic anchor while reallocating near-term promo and assortment depth toward categories with double-digit MoM or triple-digit YoY momentum.

Competitive Landscape

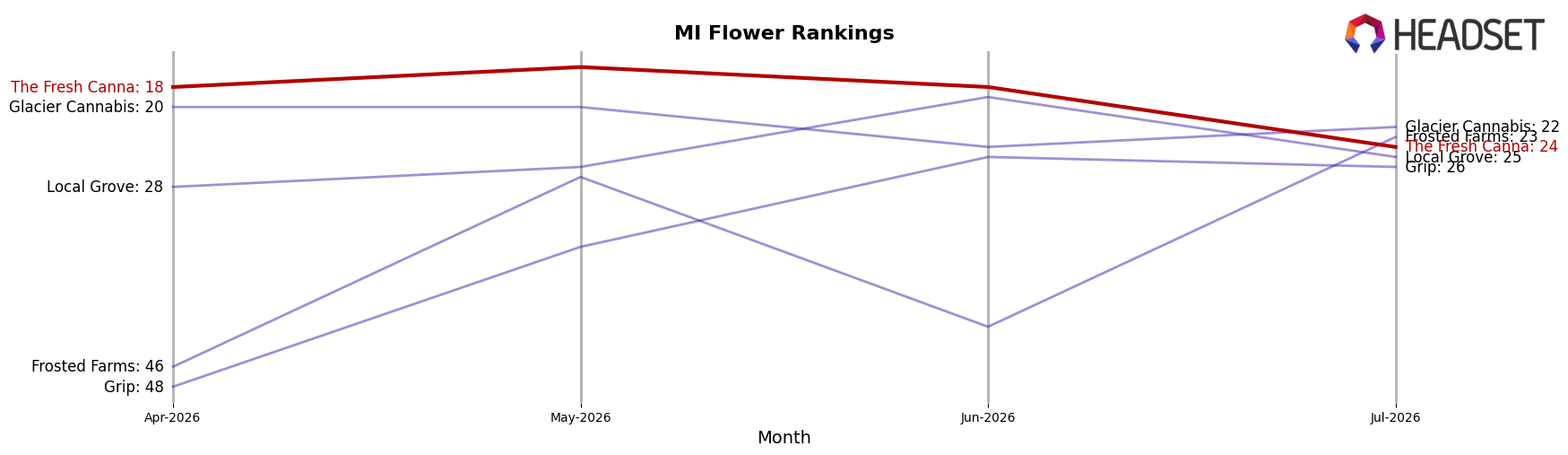

The Fresh Canna sits at rank #24 in July 2026, improving 9 positions from #33 year over year, but sliding 6 spots from #18 in April 2026, and well off its peak of #13 in August 2025; meanwhile, Mischief advanced from #10 to #4 as its sales grew 59.4% year over year and Goodlyfe Farms moved from #5 to #3 with 36.8% growth, while top-ranked High Minded stayed at #1 despite a 12.5% sales decline. Against this backdrop, The Fresh Canna’s +9 YoY rank gain alongside a 6-place quarter-over-quarter dip implies mid-pack volatility: momentum has returned versus last year, but faster-climbing rivals at #4 and #3 are compressing headroom unless recent slippage reverses.

Notable Products

Strawberry Cough Live Resin Gummies 5-Pack (200mg) posted the steepest decline in July 2026 at -18.3% MoM while sliding at least four rank positions behind the leader, and Strawberry Lemonade Live Rosin Gummies 5-Pack (200mg) also fell -12.5% as it sat in rank 3. Red Raspberry Live Resin Gummies 5-Pack (200mg) contracted -15.7% yet held rank 1, indicating price or distribution support may be offsetting velocity losses. With eight of the top ten SKUs in the Edible family and Grape Ape Live Rosin Gummies 10-Pack (200mg) down -7.2% at rank 2, the category concentration is high even as most gummies retrench, suggesting assortment relies on breadth rather than breakout innovation.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.