Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Happy Valley (MA) is stocked at 121 licensed dispensaries across Massachusetts and Alaska, 120 of them in Massachusetts, with the deepest coverage in Boston, Fall River, Worcester, Easthampton, and Pittsfield. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

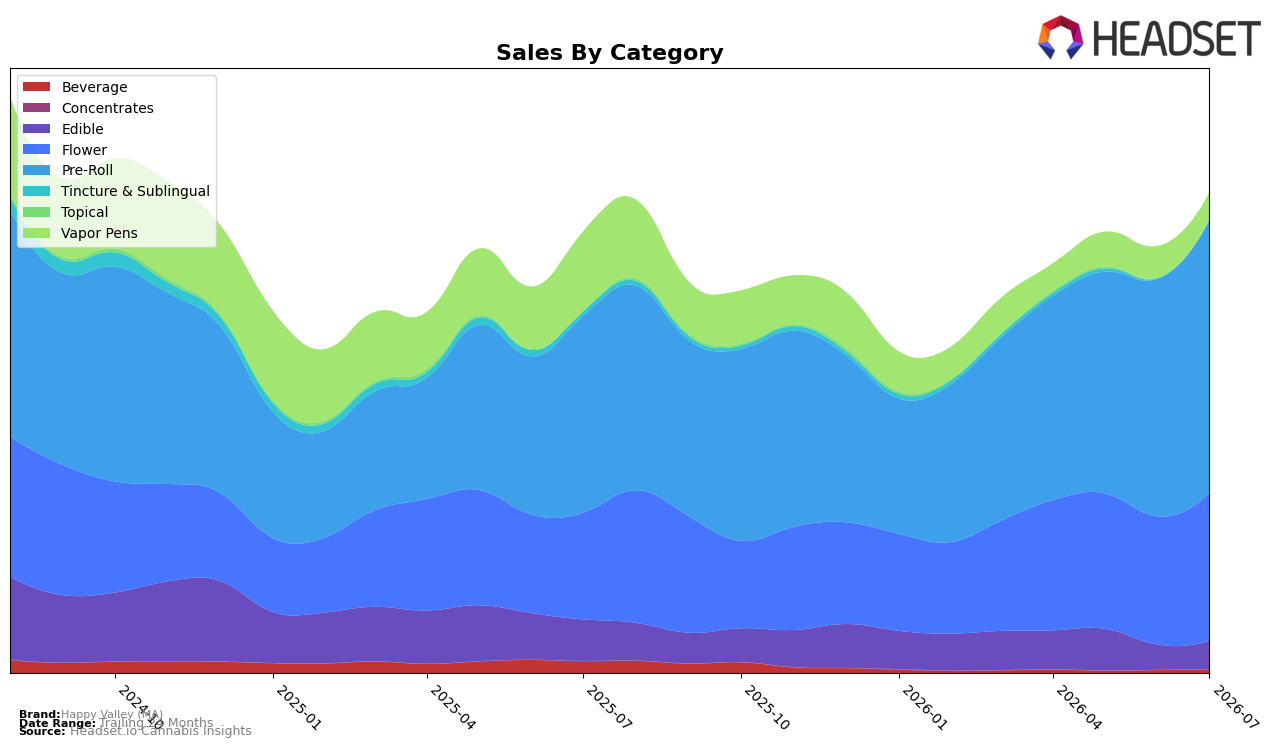

Happy Valley (MA) concentrated its July 2026 mix in Pre-Roll at 56.82% share, with Pre-Roll sales up 38.63% year over year and 14.59% month over month, while Flower held 30.88% share with parallel gains of 38.89% YoY and 15.54% MoM; together these two categories now account for 87.70% of sales in Massachusetts. At the same time, Edible contracted 31.70% YoY despite a 12.82% MoM lift to 5.89% share, and Vapor Pens declined 67.48% YoY and 17.49% MoM to 5.37% share, with Tincture & Sublingual falling 94.73% YoY and 43.72% MoM to just 0.05% share; against this, a small Topical line spiked 92.38% YoY and 189.59% MoM to 0.27% share. The pattern implies a pivot toward inhalable formats with scale, using price-adjusted momentum in Pre-Roll (average price $12.17) and Flower (average price $29.38) to offset contraction in Vapor Pens and Tincture & Sublingual, while niche bets like Topical provide optionality without diluting the core.

These shifts position Happy Valley (MA) to compete on depth within inhalables: a 7th-place rank in Pre-Roll in Massachusetts sets a clear near-term ladder, and the dual 38%+ YoY increases in both Pre-Roll and Flower suggest headroom to trade share from categories in retreat. With the brand’s overall average price down 17.25% YoY alongside Pre-Roll’s 14.59% MoM and Flower’s 15.54% MoM growth, the signal is that value-tier or promotional elasticity is working in high-velocity formats, while a 67.48% YoY decline in Vapor Pens and 94.73% YoY decline in Tincture & Sublingual argue against spreading assortment; the implication is to consolidate around the two leading pillars while using Topical’s 189.59% MoM burst as a controlled test rather than a scale candidate.

Competitive Landscape

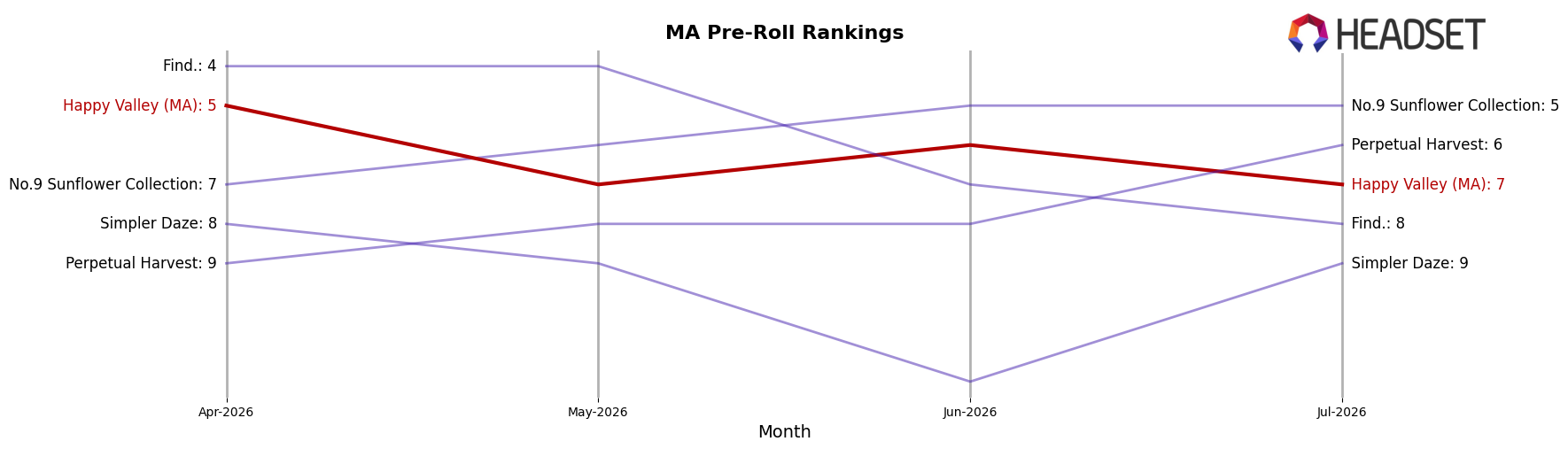

Happy Valley (MA) ranks #7 in MA Pre-Roll in July 2026, unchanged from #7 year over year, after slipping from #5 three months ago while sitting two spots below its historical peak of #4 in August 2024; in contrast, Jeeter held #1 both this year and last year and Cali-Blaze surged from #16 to #2, indicating competitors are climbing ranks faster than Happy Valley (MA) is defending them, so a flat YoY rank alongside recent quarter slippage implies share is being redistributed toward faster risers.

Notable Products

Banana Jealousy Pre-Roll (1g) delivered the standout move in July 2026 with a 65.1% month-over-month gain while holding rank 2, contrasting with Hash Burger Pre-Roll (1g) at rank 9, which fell 13.6% MoM. Super Lemon Haze Pre-Roll (1g) led the lineup at rank 1 with a 33.8% MoM increase, and White Wedding Pre-Roll (1g) at rank 3 climbed 27.7% MoM. Six of the top ten are Pre-Roll SKUs, and the only notable Flower entry, Super Lemon Haze (3.5g) at rank 6, rose 19.0% MoM with $135,845 in sales. The pattern points to a portfolio leaning into Pre-Rolls for velocity while keeping a single Flower anchor, implying a strategy centered on quick-turn SKUs with selective strain equity.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.