Mar-2025

Sales

Trend

6-Month

Product Count

SKUs

Overview

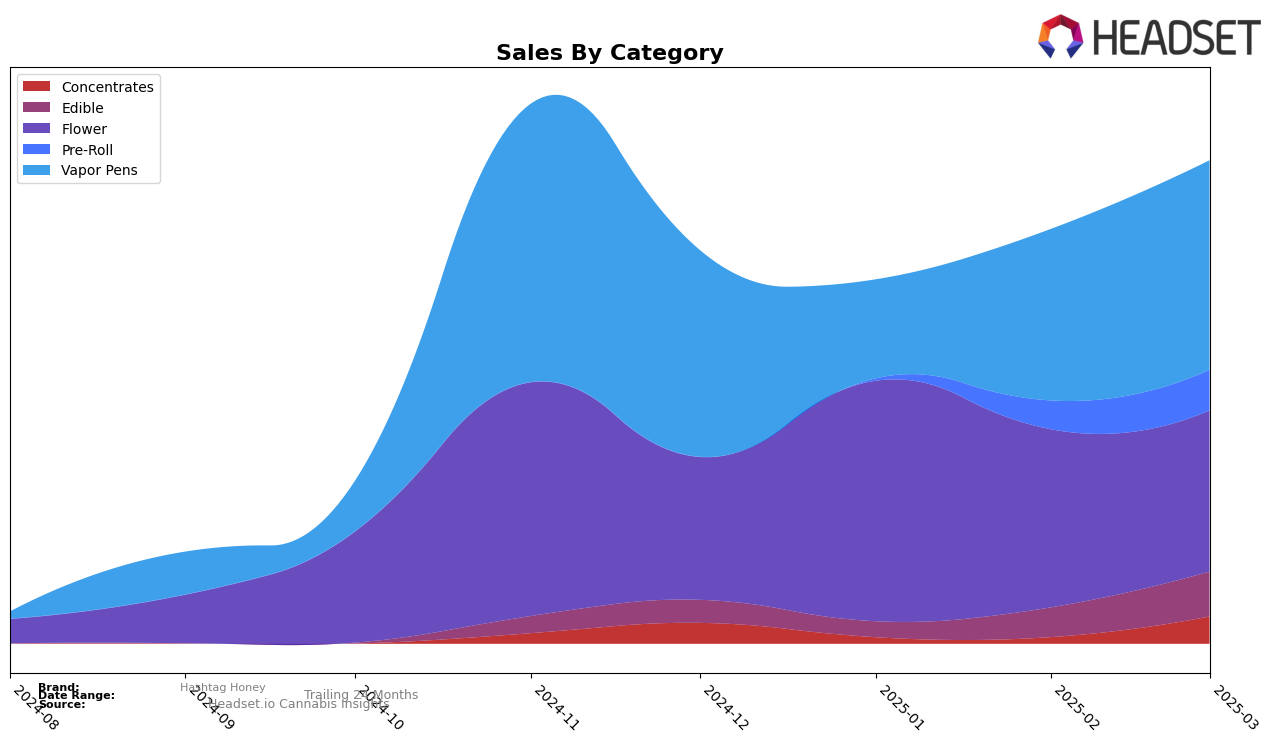

Market Insights Snapshot

Hashtag Honey has shown notable performance variations across different product categories in New York. In the Concentrates category, the brand was ranked 18th in December 2024 and reappeared in March 2025 at the 14th position, indicating a positive trend after a brief absence from the top 30. Conversely, the Edible category saw a more consistent presence, with Hashtag Honey climbing from 35th in December 2024 to 25th by March 2025, showcasing a steady improvement. The Flower category experienced some fluctuations, initially ranking 27th in December 2024, peaking at 21st in January, and then gradually descending back to 30th by March. This suggests potential challenges in maintaining a stable position in the highly competitive Flower market.

In terms of Vapor Pens, Hashtag Honey's performance was quite dynamic, with the brand starting at 22nd in December 2024, slipping to 33rd by January 2025, and then recovering to 26th by March. This indicates a recovery trend, suggesting potential strategic adjustments that might have been made to regain market position. Interestingly, the Pre-Roll category saw Hashtag Honey break into the top 30 for the first time in February 2025, ranking 62nd and then improving to 54th by March. This upward trajectory in Pre-Rolls could be a promising area for growth. The absence of Hashtag Honey in the top 30 for some months in certain categories highlights areas where the brand might focus its efforts to enhance market presence.

Competitive Landscape

In the competitive landscape of vapor pens in New York, Hashtag Honey has experienced fluctuating rankings and sales, indicating a dynamic market position. Starting with a rank of 22 in December 2024, Hashtag Honey saw a significant drop to 33 in January 2025, before recovering to 27 in February and slightly improving to 26 in March. This volatility contrasts with competitors like To The Moon, which maintained a relatively stable presence, ranking between 20 and 25 over the same period. Meanwhile, Jetty Extracts and Dime Industries showed upward trends in sales, with Dime Industries notably improving its rank from 28 to 23 by March 2025. Hashtag Honey's sales trajectory reflects a recovery from a low in January, suggesting potential for growth if the brand can stabilize its market position amidst these competitive pressures.

Notable Products

In March 2025, the top-performing product for Hashtag Honey was Blue Dream Distillate Disposable (1g) in the Vapor Pens category, climbing to the number one spot from its second-place position in February. Strawberry Diesel Distillate Disposable (1g) moved down to second place after leading in February, with notable sales of 1570 units. Superjack Distillate Disposable (1g) improved its ranking to third, up from fourth place in February. Grape Ape Distillate Disposable (1g) saw a consistent decline over the months, settling at fourth place from its initial first-place rank in December 2024. Lemon Cherry Gelato Distillate Disposable (1g) entered the rankings in March, debuting at fifth place.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.