Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

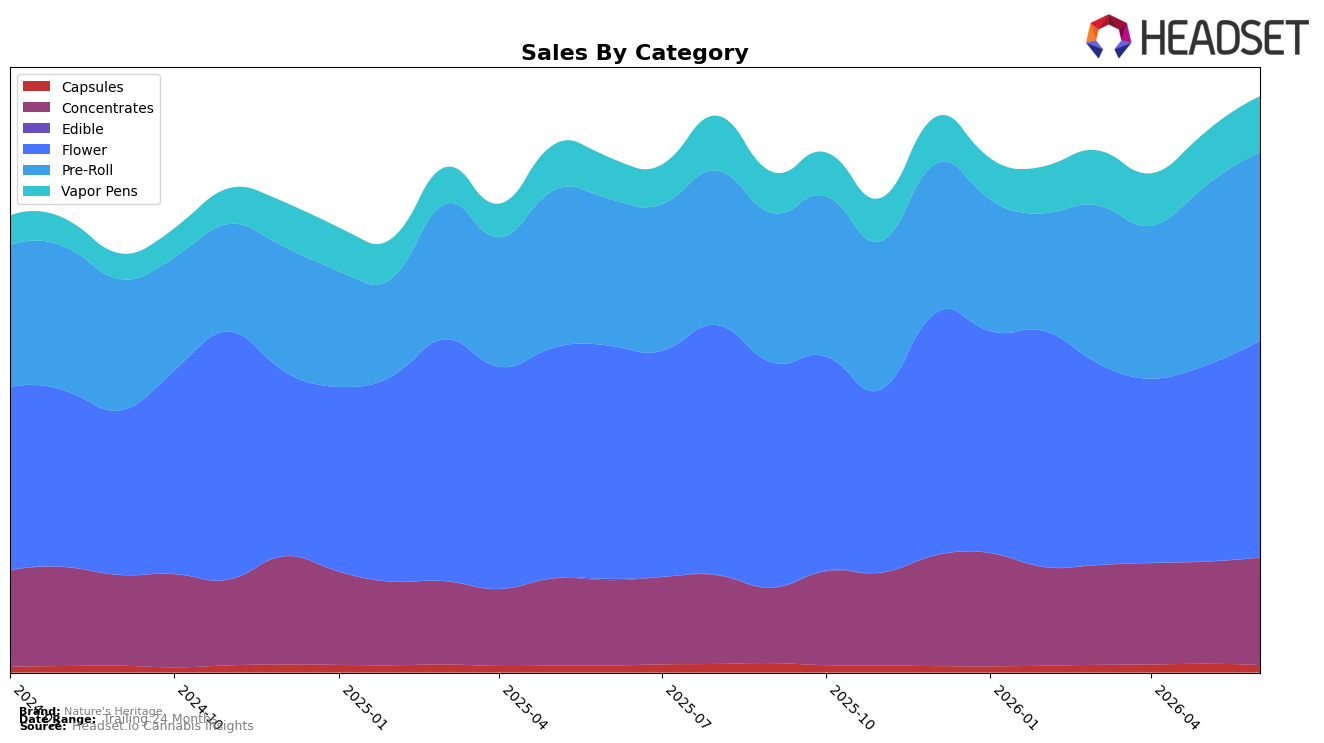

Nature's Heritage concentrated its June 2026 mix in Flower at 37.63% share and Pre-Roll at 32.75% share, with Flower down 7.15% year over year but up 10.73% month over month, while Pre-Roll rose 28.13% year over year and 5.25% month over month. Concentrates and Vapor Pens added 18.64% and 9.71% share respectively, expanding 25.78% and 35.37% year over year, alongside month-over-month gains of 5.34% and 3.85%; Capsules slipped to 1.27% share with a 15.62% month-over-month decline despite 7.75% year-over-year growth. Average price fell 13.40% year over year to $20.60 as sales grew 11.80% year over year, and Edible contracted to near-zero share with a 99.83% year-over-year decline and a 35.51% month-over-month drop. The pattern implies a pivot toward inhalable formats where momentum is concentrated, using price reductions to accelerate unit velocity while de-emphasizing micro-scale categories.

Nature's Heritage now competes in Massachusetts Pre-Roll at rank 3, pairing a 32.75% internal share with 5.25% month-over-month growth as Flower’s 10.73% month-over-month rebound supports basket breadth; together with Vapor Pens’ 35.37% year-over-year rise and 3.85% month-over-month lift, the inhalables trio signals depth rather than breadth. The coexistence of brand-level sales growth of 11.80% year over year and a 13.40% year-over-year average price decline indicates a volume-led stance, while Capsules’ 15.62% month-over-month pullback and Edible’s 99.83% year-over-year collapse show pruning of low-impact SKUs. The implication is positioning around inhalable leadership in Massachusetts with price-enabled velocity, using Flower and Pre-Roll to anchor market presence while Concentrates and Vapor Pens supply incremental share gains.

Competitive Landscape

Nature's Heritage ranks #3 in MA Pre-Roll in June 2026, improving 1 place from #4 year over year and holding steady versus March 2026 at #3; this puts the brand at its peak rank of #3 in June 2026 while still trailing Jeeter which held #1 both year over year and in June 2026, and being outpaced in upward mobility by Cali-Blaze which surged from #32 to #2 alongside a 472.5% YoY sales gain; meanwhile, Nature's Heritage sits ahead of Northern Grown, which climbed from #18 to #4 with 120.0% YoY growth and thus represents closer pressure from below—together these rank shifts imply Nature's Heritage has stabilized in the upper tier but must convert stability at #3 into incremental share capture to avoid being leapfrogged by faster climbers.

Notable Products

Guicy Banger Pre-Roll (1g) posted the largest move in June 2026 with a +51.3% month-over-month surge to rank 2, while Lilac Diesel Pre-Roll 2-Pack (1g) rose +32.9% to hold rank 1 and Lemon Cherry Gelato Pre-Roll (1g) slipped -4.0% at rank 9. Pre-Rolls account for nine of the top ten SKUs, concentrating mix and elevating rank stability at the top even as only one product crossed the +50% MoM threshold and one logged a decline under -10%. The balance of sharp acceleration at rank 2 alongside a near-flat dip at rank 9 implies Nature's Heritage is consolidating share around a premium Pre-Roll core rather than broadening into other categories.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.