Apr-2026

Sales

Trend

6-Month

Product Count

SKUs

Overview

Market Insights Snapshot

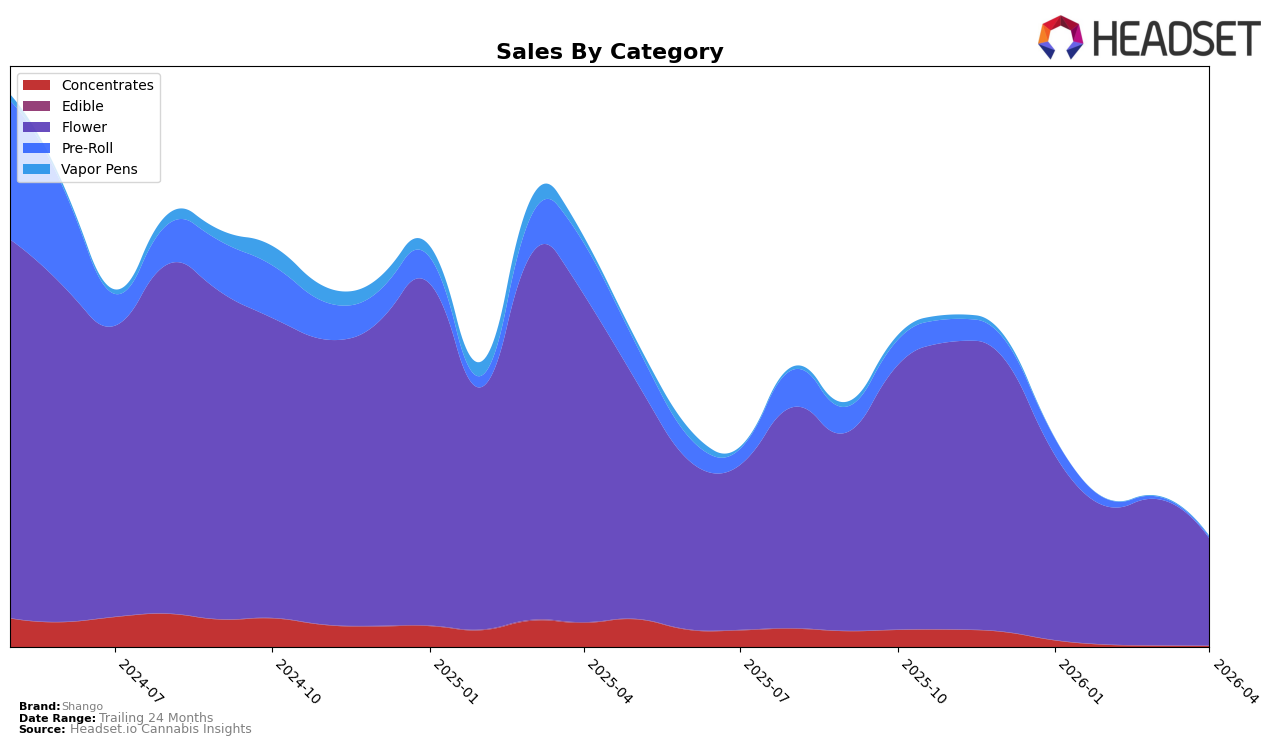

In the state of Arizona, Shango's performance across different categories has shown varying trends. In the Flower category, Shango started the year strong with an 11th place ranking in January but gradually declined to 23rd place by April. This downward trend was accompanied by a decrease in sales from $678,377 in January to $413,852 in April, indicating a potential shift in consumer preferences or increased competition. In the Concentrates category, Shango did not make it into the top 30 rankings at all, which could be a concern for the brand's market presence in this segment. Similarly, in the Pre-Roll category, Shango's ranking was outside the top 30 for most months, suggesting a need for strategic adjustments to enhance their visibility and sales in these categories.

In contrast, Shango's performance in Nevada paints a different picture. The brand did not make it into the top 30 in the Flower category for the months observed, which might reflect a challenging competitive landscape or a lack of brand penetration in this market. The absence of Shango in the rankings for other categories in Nevada further underscores the potential hurdles the brand faces in establishing a strong foothold across various product lines. These trends highlight the importance for Shango to reassess its market strategies and possibly innovate its product offerings to better capture consumer interest and improve its standings across both states.

Competitive Landscape

In the competitive landscape of the Flower category in Arizona, Shango has experienced a notable decline in its rank, dropping from 11th place in January 2026 to 23rd by April 2026. This downward trend in rank is accompanied by a decrease in sales, suggesting a potential loss of market share. Meanwhile, Curaleaf also saw fluctuations, initially ranking higher than Shango in January but eventually falling behind by April, despite a slight sales recovery in the last month. High Grade showed resilience, improving its rank to 14th in March, which may indicate a growing consumer preference. Riggs Family Farms and FENO also experienced rank volatility, with Riggs Family Farms dropping out of the top 20 by April. These dynamics highlight the competitive pressures Shango faces, emphasizing the need for strategic adjustments to regain its standing in the Arizona Flower market.

Notable Products

In April 2026, Dark Queen Shake (14g) emerged as the top-performing product for Shango, climbing from the third position in March to secure the number one spot with sales of 2430 units. Mule Fuel Shake (14g) also showed a notable rise, moving up from fifth place to second place this month. Cadillac Rainbows (3.5g) maintained a strong presence, ranking third in April after previously being second in January. Glitter Bomb (3.5g) entered the rankings in April at the fourth position, while Trop Cherry Shake (14g) rounded out the top five. The shifts in rankings highlight a dynamic market landscape with new entries and significant movements among the top products.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.