Mar-2026

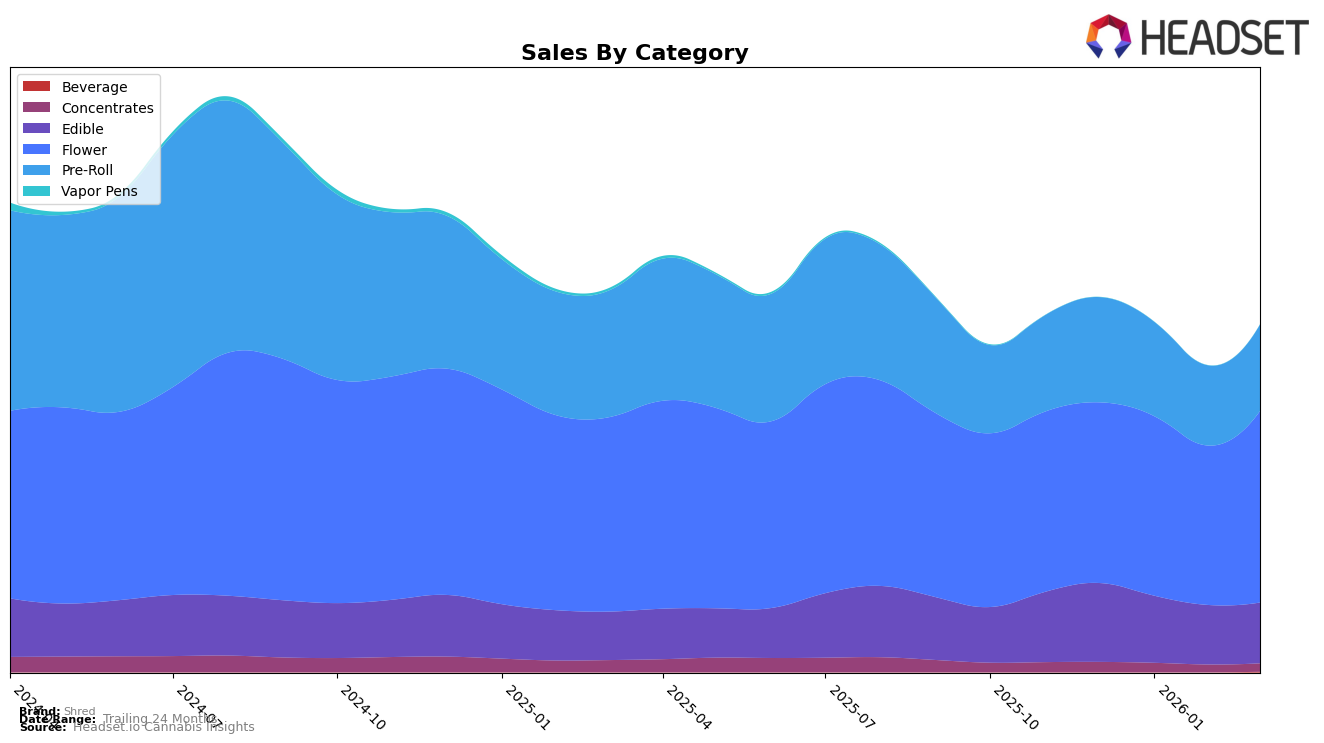

Sales

Trend

6-Month

Product Count

SKUs

Overview

Market Insights Snapshot

Shred's performance across various categories and regions has shown some interesting patterns in recent months. In Alberta, Shred has maintained a consistent presence in the Edible category, holding a steady rank of 3rd place from December 2025 to February 2026, before slipping to 6th in March. This decline in rank corresponds with a gradual decrease in sales figures over the same period. The Flower category in Alberta tells a different story, with Shred struggling to maintain a stable position, dropping from 16th to 25th place by March 2026. Meanwhile, Shred's Pre-Roll category in Alberta has shown some resilience, with a slight dip in rank from 12th to 15th, but a notable increase in sales in January 2026 suggests potential for recovery.

In British Columbia, Shred's presence in the Edible market remains robust, consistently holding the 5th position across the months from December 2025 to March 2026. This stability contrasts with their Flower category performance, where they failed to break into the top 30 until February 2026, eventually reaching 28th place before dropping to 31st. Interestingly, Shred's Pre-Roll category in British Columbia has seen a positive trajectory, improving from 10th to 8th place by March 2026. In Ontario, Shred's Flower category has been particularly strong, maintaining a top 3 position and even climbing to 2nd place in February and March 2026. However, their Concentrates category hasn't seen similar success, as they did not rank in the top 30 past December 2025. The data from Saskatchewan indicates a steady presence in the Edible category, although their absence from the March 2026 rankings suggests a potential decline in market presence.

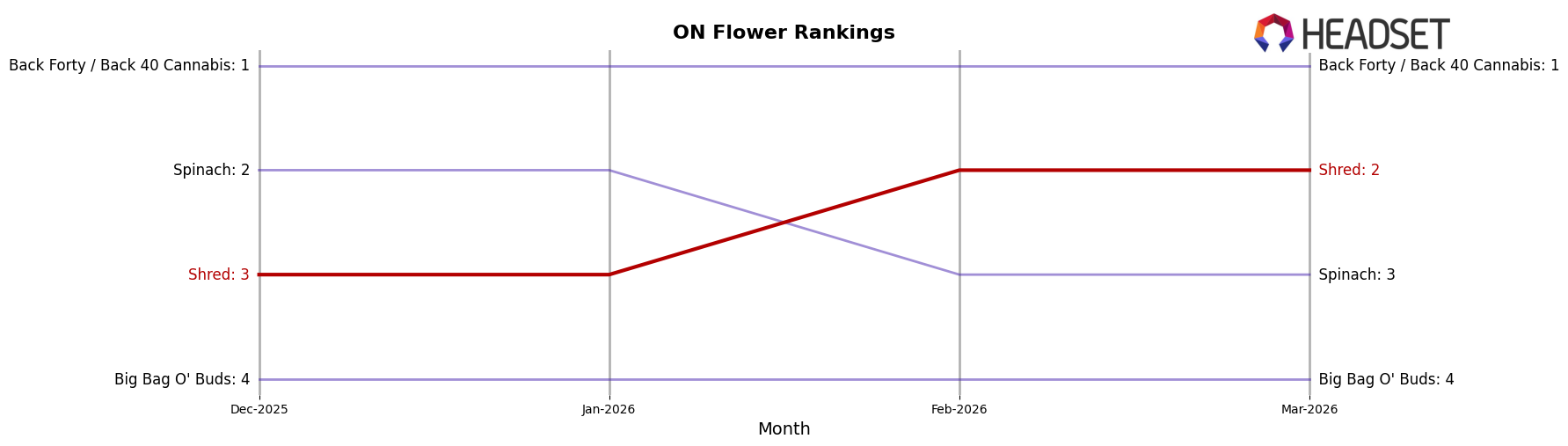

Competitive Landscape

In the competitive landscape of the Flower category in Ontario, Shred has demonstrated notable resilience and growth. As of March 2026, Shred has ascended to the second rank, overtaking Spinach, which dropped from second to third place. This shift highlights Shred's strategic positioning and appeal in the market. Despite Back Forty / Back 40 Cannabis maintaining a consistent lead at the top rank, Shred's upward trajectory in rank and sales, particularly from February to March 2026, indicates a strengthening brand presence. Meanwhile, Big Bag O' Buds remains stable at the fourth position, suggesting that Shred's competitive edge is more pronounced against brands that are not experiencing significant rank changes. This dynamic environment underscores the importance for Shred to continue leveraging its momentum to potentially challenge the leading position in the coming months.

Notable Products

In March 2026, the top-performing product from Shred was Shred'ems - CBD/THC 4:1 Wild Berry Blaze Gummy 4-Pack (40mg CBD, 10mg THC) in the Edible category, maintaining its number 1 rank consistently from December 2025. Gnarberry (7g) in the Flower category climbed to the second position, showing an increase in sales to 22,594 units, up from its fourth position in February 2026. Tropic Thunder (7g) also in the Flower category improved its ranking significantly, moving to third place from being unranked in February. Shred'ems - CBD/THC 2:1 Sour Blue Razzberry Gummies 4-Pack (20mg CBD,10mg THC) held the fourth spot, having dropped from second place in the previous month. Shred'ems Pop! - CBD/THC 1:1 Root Beer Blast Gummies 4-Pack (10mg CBD, 10mg THC) rounded out the top five, maintaining a stable presence despite a slight drop in sales figures.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.