Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

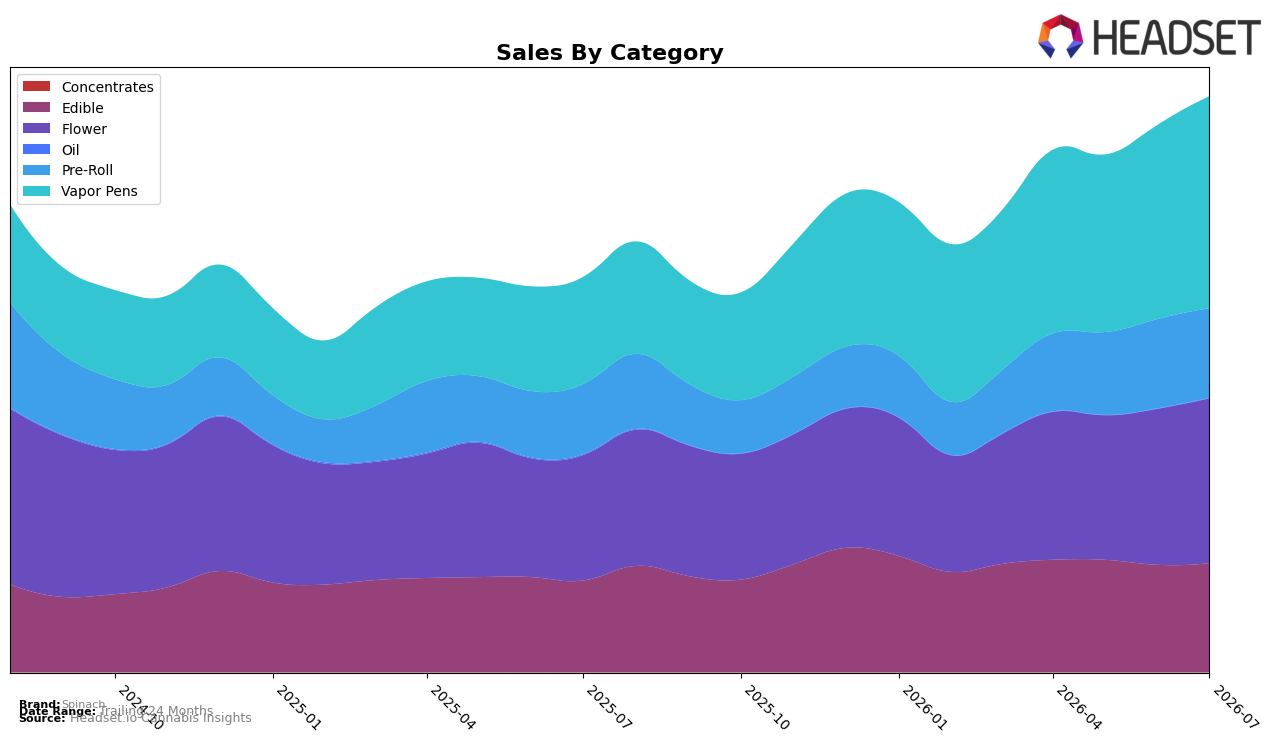

In July 2026, Spinach leaned into a two-tier mix: Vapor Pens rose to 36.85% share with 98.30% year-over-year growth and 9.19% month-over-month, while Flower held 28.61% share with 31.43% YoY and 5.57% MoM. Edible contributed 18.96% share with 18.84% YoY and 1.57% MoM, and Pre-Roll added 15.53% share with 27.79% YoY and 0.17% MoM; Oil slipped to 0.05% share despite a 34.13% MoM uptick and a -67.24% YoY decline. With overall brand sales up 45.77% YoY and the average price up 46.25% YoY, the pattern implies Spinach is scaling volume in higher-priced segments (Vapor Pens and Flower) while allowing low-share Oil to recede, concentrating growth where price realization and repeat velocity can compound.

Positioning-wise, a Vapor Pens lead at 36.85% share alongside a Flower rank of 2 in Alberta signals a dual-pillar strategy: premium inhalables anchoring penetration and baskets, with Edible and Pre-Roll providing breadth at 18.96% and 15.53% share respectively. July 2026 momentum skewed toward Vape and Flower (9.19% and 5.57% MoM) versus Edible and Pre-Roll (1.57% and 0.17% MoM), implying merchandising and supply are aligned to defend top-2 Flower rank while compounding Vape gains; the -67.24% YoY in Oil paired with a 34.13% MoM bump suggests controlled pruning rather than a turnaround priority, keeping the brand positioned as an inhalables-first operator with selective depth in value-access categories.

Competitive Landscape

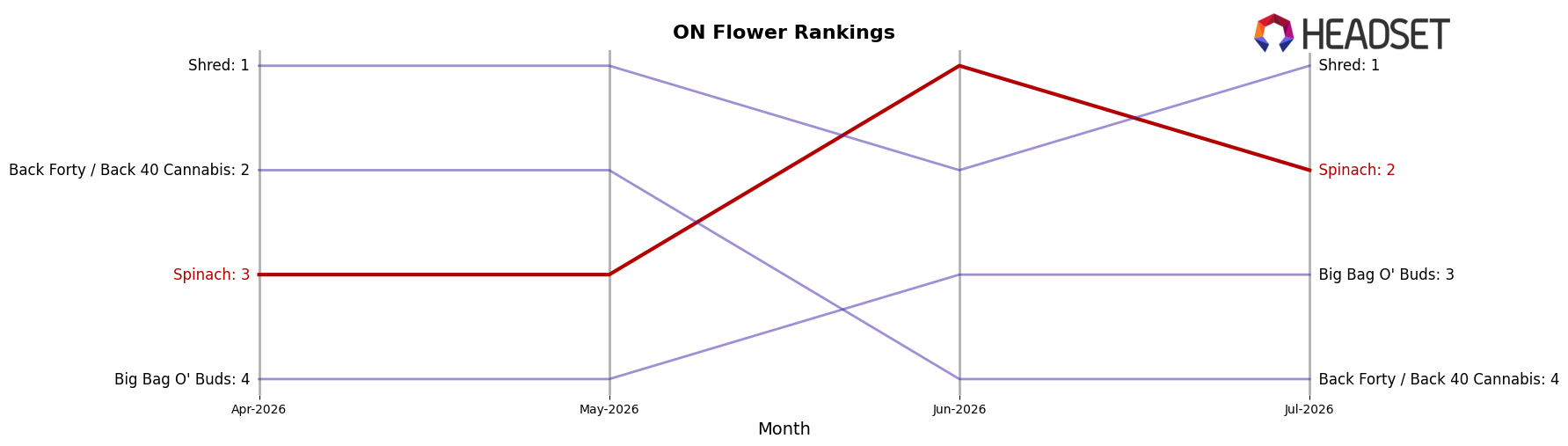

Spinach is ranked #2 in ON Flower in July 2026, improving 2 positions from #4 year over year and edging up 1 spot from #3 in April 2026; however, it slipped 1 place from its peak at #1 in June 2026, which puts the brand in a narrow band of movement near the top. Shred holds #1 after rising from #2 year over year while posting a 17.2% sales increase, and Back Forty / Back 40 Cannabis fell from #1 to #4 with a -5.4% sales change, indicating Spinach’s ascent is occurring amid a leadership transition where the path back to #1 depends on outperforming an incumbent with positive momentum rather than waiting for competitor decline.

Notable Products

Sourz - Blue Raspberry Watermelon Gummies 5-Pack (10mg) posted the largest movement in July 2026 with a month-over-month gain of 782.5% while rising to rank 2, implying a sharp shift toward entry-size gummy formats. In contrast, the larger Sourz - Fully Blasted Blue Raspberry Watermelon Gummies 10-Pack (100mg) slipped 3.8% MoM at rank 6 as the 1-pack variant at rank 1 grew 32.1%, and four of the top ten are Edible SKUs concentrated in the Sourz gummy family. Pre-Rolls held ground with Sour Chem Pre-Roll 2-Pack (2g) up 6.1% at rank 5 while GMO Cookies Pre-Roll (1g) increased 5.4% at rank 8, but the CBD/THC 1:1 gummy 10-Pack declined 4.3% at rank 9 despite $523,469 in sales. The pattern indicates a mix shift toward smaller-dose, flavor-led gummies and steady Pre-Roll support, pointing Spinach toward variety-pack and trial-friendly formats over bulk edible packs.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.