Where to Buy

Sublime is stocked at 226 licensed dispensaries across New Mexico, Arizona, and 4 other states, 105 of them in New Mexico, with the deepest coverage in Albuquerque, Hobbs, Las Cruces, Sunland Park, and Alamogordo. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

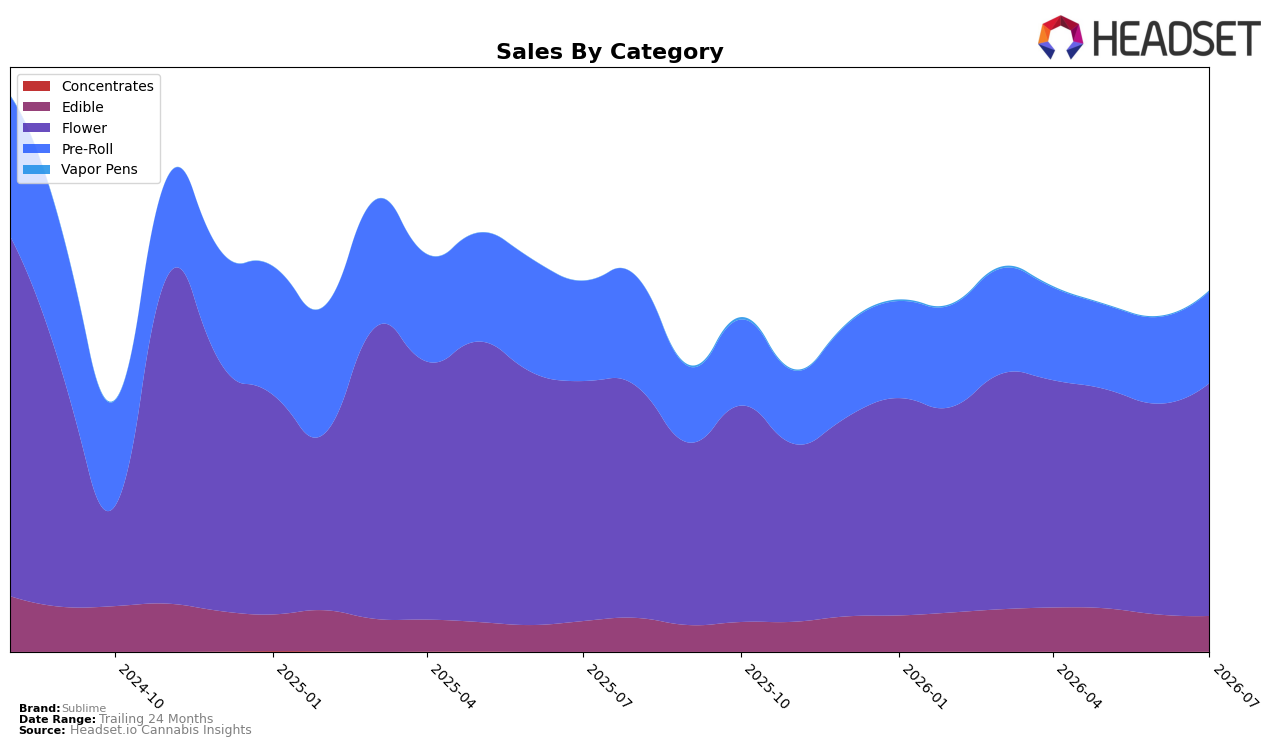

Market Insights Snapshot

In July 2026, Sublime concentrated 64.47% of sales in Flower with a month-over-month gain of 10.41% but a year-over-year decline of 3.04%, while Pre-Roll held 25.40% share with a 6.05% MoM lift and an 8.40% YoY drop. Edible accounted for 9.84% share with a 16.31% YoY increase but a 4.31% MoM contraction, and Vapor Pens, though just 0.25% share, jumped 25.76% MoM; Concentrates remained a negligible 0.04% with no clear trend. The mix indicates a pivot toward near-term volume recovery in Flower and Pre-Roll despite YoY drag, while Edible provides the only YoY growth engine, implying that short-term promotions or pricing in July 2026 outweighed longer-cycle demand softness.

Positioning-wise, the 6.79% YoY average price increase alongside a 2.61% YoY sales decline suggests elasticity pressure in core Flower and Pre-Roll, whereas Edible’s 16.31% YoY growth at 9.84% share signals headroom for differentiated value tiers. The 25.76% MoM surge in Vapor Pens at 0.25% share points to a low-base test that could diversify the portfolio without cannibalizing Flower’s 64.47% weight, and the 27 rank in Flower in Missouri frames the brand as mid-pack where incremental share gains likely come from stabilizing YoY declines while leaning into Edible momentum. Net, the pattern implies prioritizing price-pack architecture in Flower to ease elasticity while scaling Edible activation to convert its YoY strength into sustained share gains.

Competitive Landscape

Sublime sits at rank #27 in Missouri Flower for July 2026, improving 2 positions year over year from #29 but slipping 2 spots from April 2026’s #25, while its historical peak was #20 in August 2024; by contrast, Flora Farms held steady at #1 with a 1.25% year-over-year sales decline and Sinse Cannabis climbed from #4 to #2 with a 8.99% sales increase, indicating Sublime’s modest YoY rank gain is being outpaced by upward mobility among leaders and recent quarter slippage, implying a trajectory of incremental improvement that risks further crowd-out without a catalyst to reverse the 2-rank quarter-over-quarter dip.

Notable Products

Moonbow 112 IX Pre-Roll (1g) posted the steepest movement in July 2026 with a -57.2% month-over-month drop and slid to rank 4, while Hot Rod - GDP Infused Pre-Roll (0.5g) fell -22.4% and sits at rank 7. In contrast, Hot Rod - Purple Urkle Infused Pre-Roll (0.5g) rose 11.6% to rank 5, and Hot Rod - Cherry Dream 91 Infused Pre-Roll (0.5g) in rank 10 edged down -2.5% despite category stability.

Pre-Rolls account for all top-10 SKUs, with Hot Rod infusions occupying ranks 3, 5, 6, 7, 8, and 10, indicating a concentration in infused formats even as non-infused leaders hold ranks 1 and 2. The top two SKUs each generated more than $30,000, with Roseanna Pre-Roll (1g) at $30,728 and Hawaiian Fonta Pre-Roll (1g) close behind, implying a barbell mix where flagship non-infused volume coexists with mid-pack volatility among infused variants.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.