Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Treeworks is stocked at 243 licensed dispensaries across Massachusetts, New Jersey, and Connecticut, 193 of them in Massachusetts, with the deepest coverage in Boston, Northampton, Pittsfield, Worcester, and Fall River. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

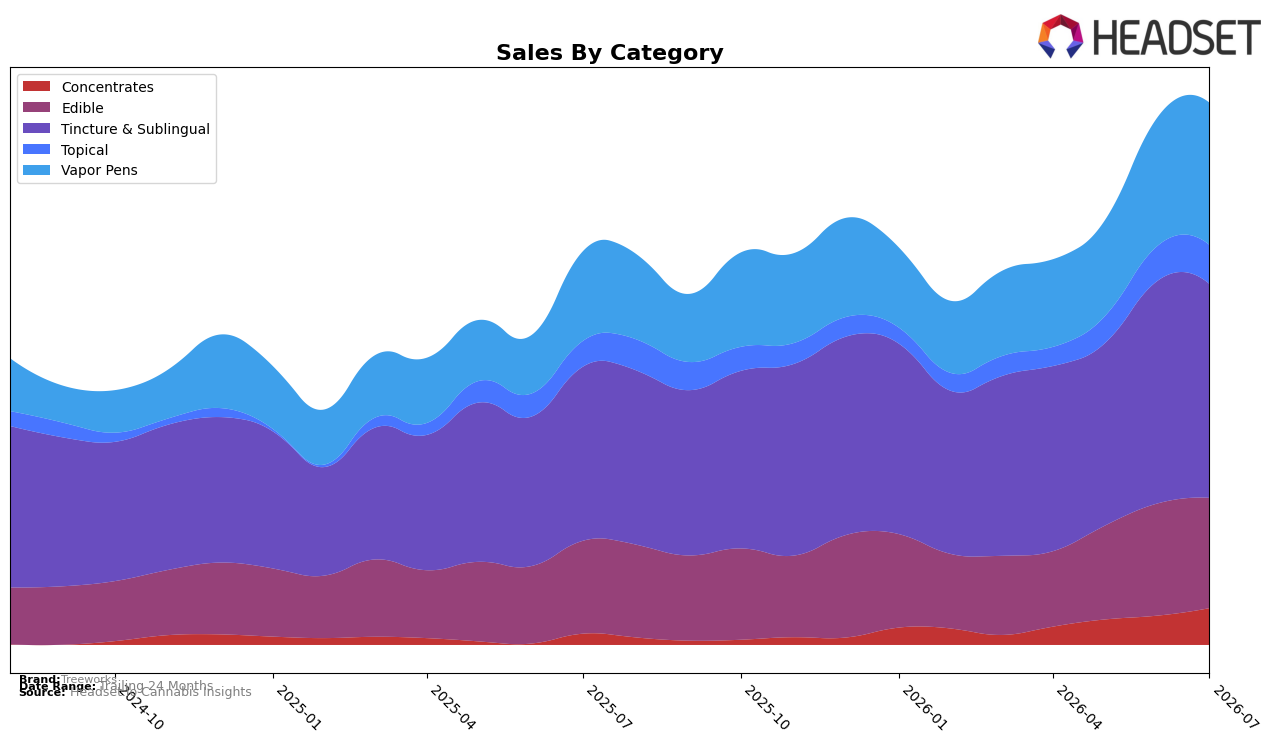

Treeworks concentrated 37.45% of July 2026 sales in Tincture & Sublingual, where year-over-year growth was 21.29% but month-over-month slipped 3.81%, while Vapor Pens expanded to 25.59% share with 51.33% YoY and 9.47% MoM gains. Edible held 20.31% share with 16.51% YoY but a 1.55% MoM dip, and smaller buckets moved up: Concentrates climbed 107.94% YoY and 17.76% MoM to 8.13% share, and Topical rose 34.90% YoY and 8.60% MoM to 8.51% share. With brand-level sales up 32.55% YoY and the average price up 1.22%, the pattern implies Treeworks is shifting from a single-category anchor toward a more balanced mix, with faster-growing inhalables and Concentrates offsetting recent softness in Tincture & Sublingual and Edible.

That mix shift translates to a positioning pivot: maintaining a leading presence in Tincture & Sublingual (37.45% share) while leaning into velocity categories where MoM is positive, notably Vapor Pens at 9.47% and Concentrates at 17.76%. The 21.29% YoY in Tincture & Sublingual combined with a 3.81% MoM dip suggests a mature core that continues to add annual dollars but cedes incremental monthly momentum to faster-turn formats, and the 51.33% YoY in Vapor Pens alongside 34.90% YoY in Topical indicates broadened consumer adoption beyond ingestibles. The implication is that Treeworks can defend its core while using inhalable-led gains to lift overall growth above the 32.55% YoY brand pace, narrowing dependency on any single format and creating headroom for price at a $41.46 average without eroding mix.

Competitive Landscape

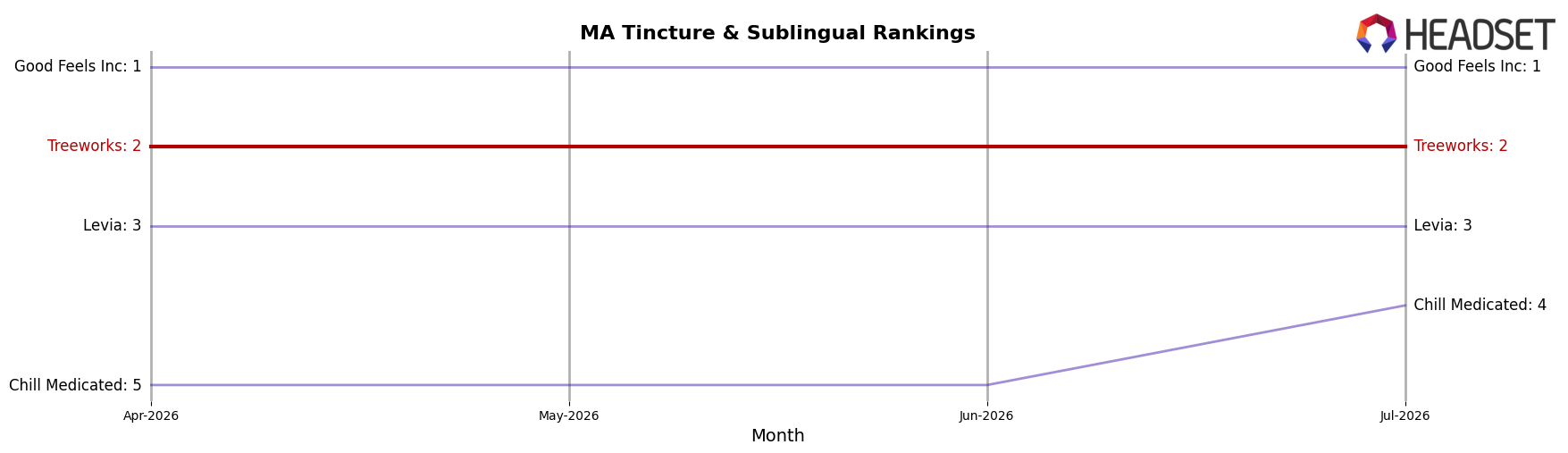

Treeworks sits at rank #2 in MA Tincture & Sublingual in July 2026, unchanged from #2 a year earlier, and it also held #2 three months ago, implying flat rank momentum even as competitors reshuffle; Good Feels Inc remains #1 with a -5.1% year-over-year sales change while Treeworks stays put at #2, and Levia holds #3 with +130.6% year-over-year growth, indicating pressure from below, whereas Howl's slipped from #4 to #5 alongside an -11.7% decline and Chill Medicated climbed from #8 to #4 on +368.3% growth, so a stable #2 rank paired with faster-moving challengers implies Treeworks must defend share to avoid being overtaken despite hitting its peak rank of #2 in July 2026.

Notable Products

Dream Drops - THC/CBN 1:1 Indica Bedtime Bliss Tincture (300mg THC, 300mg CBN, 60ml, 2oz) delivered the sharpest move in July 2026 with +17.7% MoM to rank 5, while the Happy - CBD/CBG/THC 3:3:1 Tropical Passionfruit Hibiscus Hash Rosin Gummies 20-Pack (300mg CBD, 300mg CBG, 100mg THC) rose +12.5% MoM and held rank 1, implying depth rather than a single-SKU spike. Two Topical SKUs sat in the top 10 with CBD/THC 1:1 Full Spectrum RSO Canna Cream (150mg CBD, 150mg THC, 2oz) up +12.6% at rank 7 and CBD/THC 1:1 Extra Strength Canna Cream (500mg CBD, 500mg THC, 2oz) up +6.3% at rank 2, pointing to steady analgesic demand alongside edibles leadership. Three Tincture & Sublingual entries occupied ranks 5, 9, and 10 with MoM changes of +17.7%, +1.9%, and n/a respectively, while Vapor Pens clustered at ranks 4, 6, and 8 with +19.0% MoM on Honeydew #2 Live Hash Rosin Wand Disposable (0.5g), indicating broader basket reach beyond a single format. The pattern implies Treeworks is leaning into multi-cannabinoid wellness SKUs across tinctures and topicals while keeping an anchor edible at rank 1, a mix that balances routine-use categories with a high-velocity gummy to drive traffic and trade-up.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.