Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Agro Couture is stocked at 162 licensed dispensaries across Washington and Oklahoma, 155 of them in Washington, with the deepest coverage in Seattle, Tacoma, Spokane, Everett, and Vancouver. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

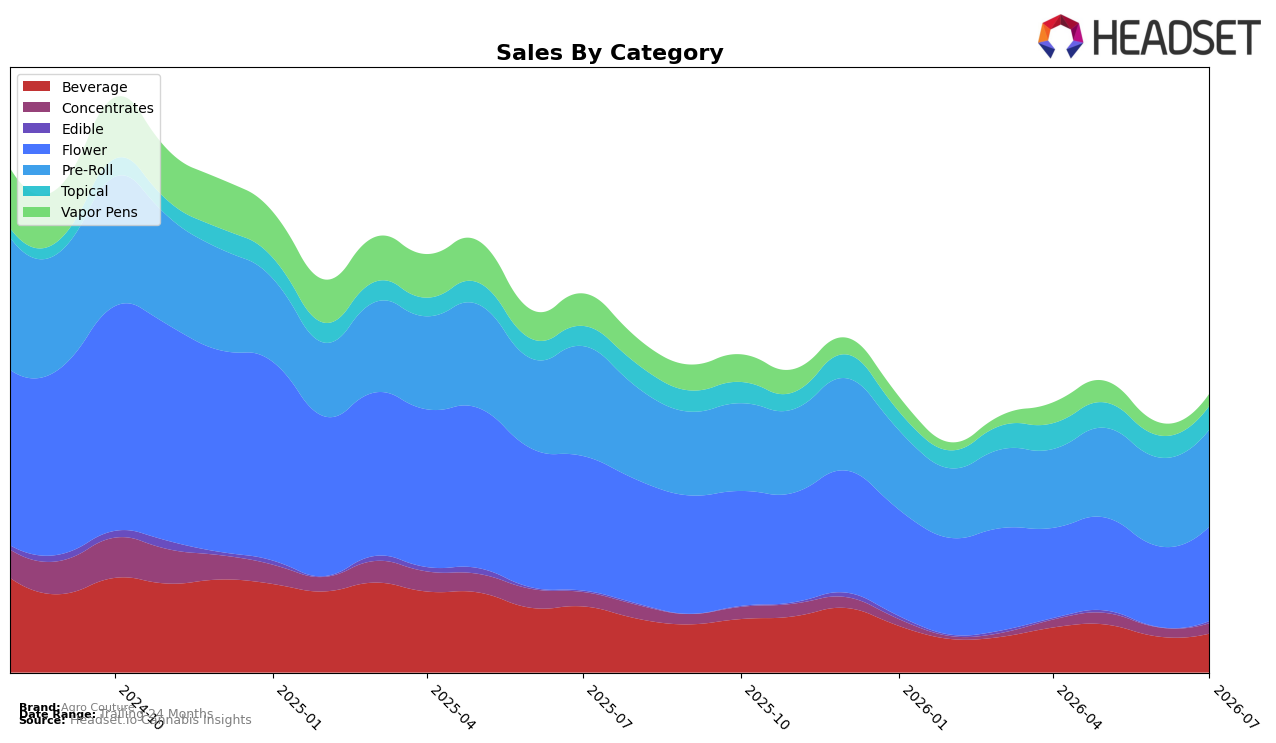

In July 2026, Agro Couture’s mix concentrated in Pre-Roll at 29.37% share and Flower at 28.70% share, with Pre-Roll up 8.07% month over month but down 10.34% year over year, while Flower climbed 14.39% MoM yet fell 26.90% YoY. Beverage held 14.06% share with a 5.79% MoM lift but a 33.75% YoY decline, as Topical accounted for 10.02% share with a 4.47% MoM gain and a 10.23% YoY increase. Vapor Pens at 7.00% share slid 3.35% MoM and 43.36% YoY, and Concentrates at 6.52% share rose 5.00% MoM but dropped 13.95% YoY, while Edible at 4.34% share advanced 11.62% MoM and 4.79% YoY. This pattern implies the month’s growth leaned on tactical rebounds in Flower and Pre-Roll and steadying smaller formats (Topical, Edible), partially offsetting structural YoY erosion concentrated in Vapor Pens and Beverage.

With brand sales down 20.88% year over year and average price down 9.16%, the expansion of lower-priced Pre-Roll (average price $6.07) and Edible (up 11.62% MoM, up 4.79% YoY) points to a value-oriented repositioning that trades margin for volume, while the continued 43.36% YoY contraction in Vapor Pens and 33.75% YoY decline in Beverage limit premium mix recovery. Pre-Roll’s rank position in Washington at 18, combined with Flower’s 14.39% MoM surge, suggests near-term share defense in core inhalables, but the durable YoY growth in Topical at 10.23% and the modest YoY gain in Edible indicate diversification is cushioning volatility in larger categories. The implication is that sustaining momentum will require keeping MoM gains in Flower and Pre-Roll while reallocating away from underperforming Vapor Pens and Beverage to stabilize the overall mix despite a 39.16% two-year sales decline.

Competitive Landscape

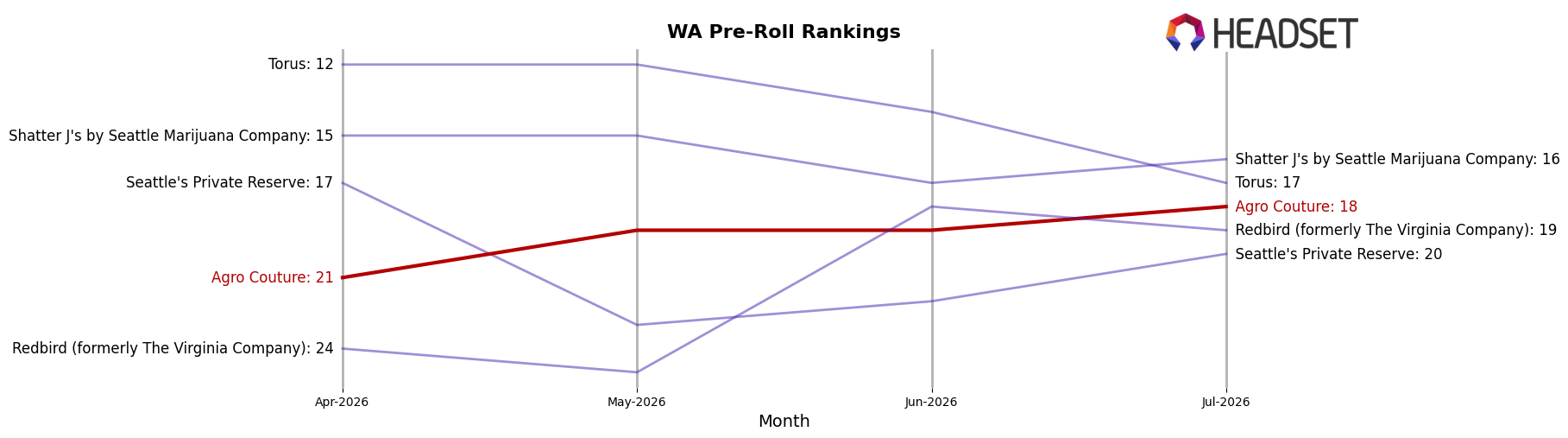

Agro Couture sits at rank #18 in WA Pre-Roll for July 2026, down 1 position year over year from #17 and up 3 spots versus April 2026’s #21, while still trailing its peak of #14 from December 2024; by comparison, Ooowee climbed from #2 to #1 and Phat Panda slipped from #1 to #2 as of July 2026, indicating top-tier volatility that Agro Couture has not mirrored. With leaders posting year-over-year sales growth of 59.5% at Ooowee and 1.2% at Phat Panda, Agro Couture’s rank holding pattern between #14 and #21 suggests mid-pack stability but limited share capture, implying that without a catalyst to reverse the 1-rank YoY erosion and convert the 3-rank spring-to-summer gain into sustained momentum, the brand risks being boxed out by faster-moving rivals.

Notable Products

Tropicana Cookies Pre-Roll (1g) delivered the standout move in July 2026 with a 59.5% month-over-month gain to rank 3, while Wedding Cake Pre-Roll 2-Pack (1g) rose 36.6% to hold rank 1, indicating velocity is concentrated at the top of the chart. Alaskan Thunder Fuck Pre-Roll (1g) climbed 27.6% at rank 2 as four of the top ten are Pre-Roll SKUs, suggesting the brand’s throughput is increasingly tied to combustion formats rather than beverages, where CBD/THC 1:1 Blue Raspberry Infused Lemonade (100mg CBD, 100mg THC, 1.7oz) advanced only 4.8% at rank 4. The concentration of gains above 25% across ranks 1–3, alongside a modest 1.3% uptick for Ice Cream Cake Pre-Roll (1g) at rank 8 and a $24,781 Topical at rank 9 with no MoM marker, implies Agro Couture is leaning into fast-turn Pre-Rolls as the commercial core while non-Pre-Roll formats contribute stability rather than growth.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.